Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Making the grade: the world of emerging market corporate debt

With the emerging market debt (EMD) universe increasingly considered to be mainstream, we weigh up the pros and cons of investing in hard currency EMD investment-grade corporate debt.

No longer considered a niche asset class, the emerging market debt (EMD) universe is made up of several sub-asset classes – hard currency investment grade and high yield corporates, sovereigns and quasi-sovereign bonds along with local currency sovereign bonds. Here we focus on the pros and cons of hard currency EMD investment-grade corporate debt.

A fast-growing universe

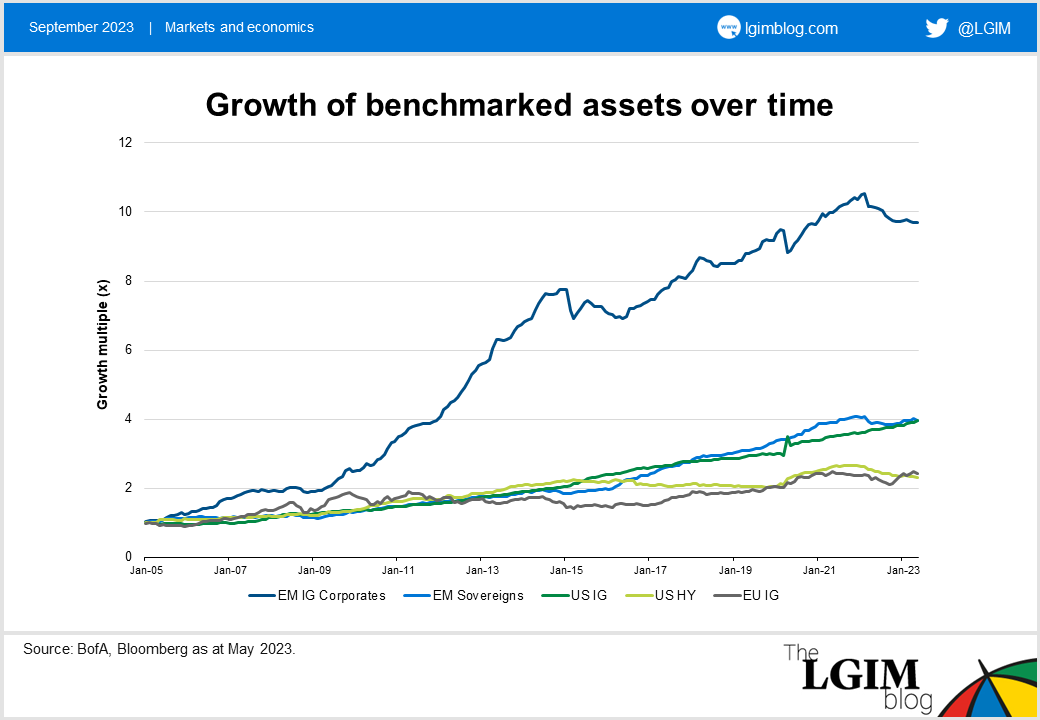

Emerging market corporate debt started gaining in popularity in the late 2000s when J.P. Morgan launched the Corporate Emerging Markets Bond Index suite, consisting of hard currency emerging market (EM) corporate debt. Within the universe, and as can be seen from the chart below, EM investment-grade (IG) corporates have grown significantly over time, standing at over US$1 trillion in size[1].

While it may come as a surprise to some, this makes it almost as large as the US high yield, emerging market sovereign and agency commercial real estate markets. Perhaps as surprising is that the majority (over 60%) of the emerging market corporate debt market is rated investment grade (IG), with an average BBB- rating[2].

Investment grade EM debt: resilient in times of recession?

For many investors the key question is how asset classes could perform at various points of the economic cycle. While this year has seen resilient economic activity (with the exception of China), we continue to believe that a global downturn is on the cards, although the extent of that downturn will be more focused on developed market nations than their emerging market counterparts, in our view.

It’s often assumed that, in the event of a recession, emerging market corporate bonds are more prone to defaults than their developed market counterparts. In our view this isn’t true of investment-grade bonds, which, we believe, have similarly low default rates in both markets. Over time, the average ratings of EM corporates have improved, which is reflected in the average rating of different EM corporate indices[3].

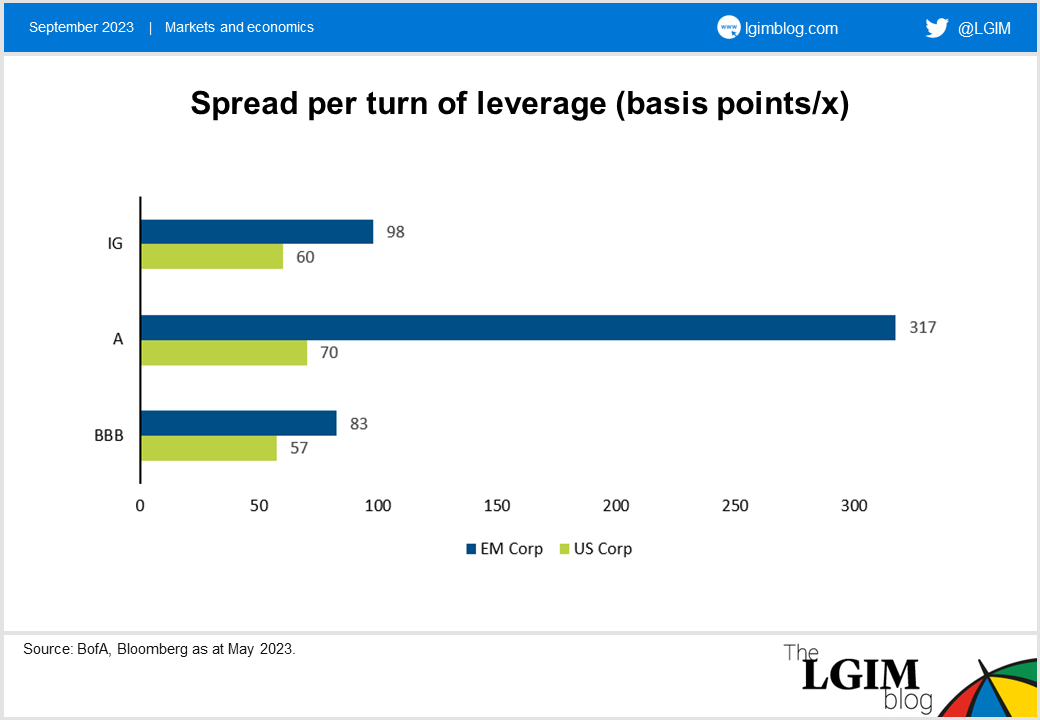

Improving fundamentals for EM IG corporates can also be evidenced by them having better net leverage ratios than US IG corporates. Investors also get a spread pick-up per unit of leverage as seen from the chart below.

Keeping credit quality

We think the yield narrative remains compelling for EM IG corporates despite rates selling off in developed markets. At the time of writing, EM IG corporates[4] provide a yield of just over 6%, c.49 basis points (bps) over US IG and c.185bps over EUR IG corporates. If yields fall going into the end of this year or early next year and we manage to avoid recession, we believe the yield differential could widen to more historic levels. Our view is that this yield pick-up may provide investors with an option to substitute their US IG or EUR IG allocations towards EM IG while maintaining a similar credit quality.

Mind the vol

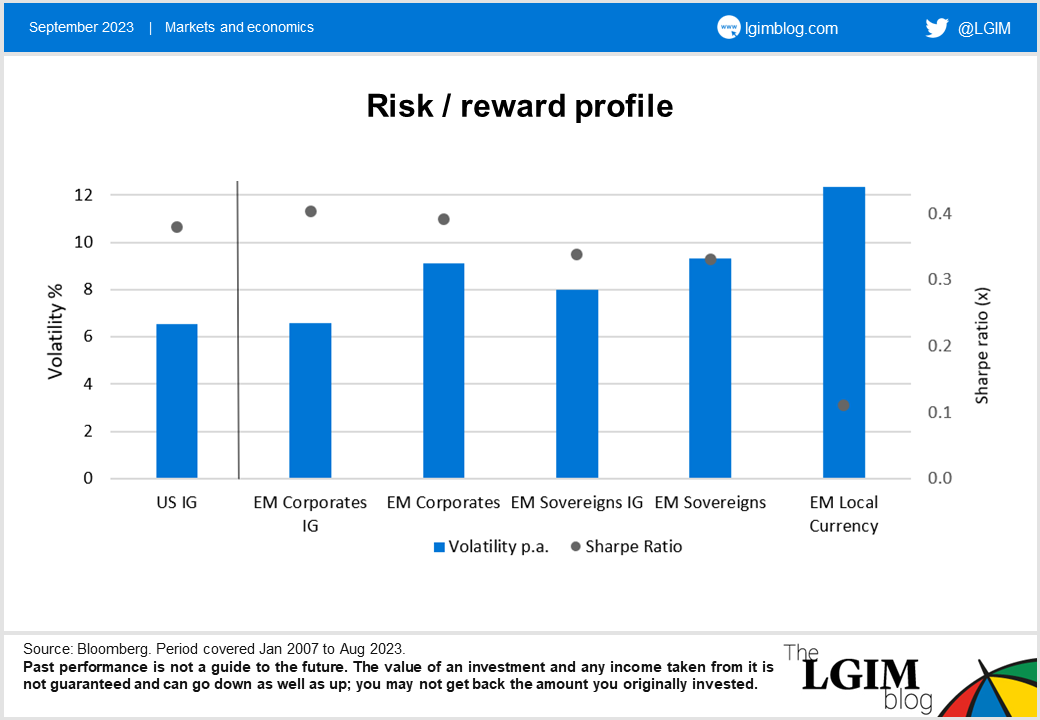

Volatility tends to be higher in emerging market debt than developed markets. That said, we believe investors are compensated for that higher volatility, especially in the emerging market investment-grade corporate space. As seen in the chart below, EM IG corporates have historically had the lowest volatility and highest Sharpe ratios of all other EMD investments – notably sovereigns and EMD local currency.

In our view, since EM IG corporates typically have lower duration, we believe they offer the potential for superior risk-adjusted returns in a rising or a stable interest rate environment. Furthermore, the IG corporate index provides diversification[5] at the country and issuer level, with over 400 issuers from about 30 countries. As a result, there are many under-researched issuers in the index leading to information asymmetry. The depth of the universe and, at times, a lack of information makes the life of the active fund manager an interesting one.

[1] Source: BofA, Bloomberg as at May 2023.

[2] Source: JPM CEMBI BD Index rating as at September 2023.

[3] Source: BofA, Bloomberg as at May 2023.

[4] Source: JPM CEMBI IG+ index as at September 2023.

[5] It should be noted that diversification is no guarantee against a loss in a declining market.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.