Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Emerging market debt: Time to shine?

Given a resilient macroeconomic picture and supportive technicals, we believe the outlook for emerging market debt (EMD) is positive.

The following is an extract from our latest CIO outlook.

It has been a challenging two years in emerging market (EM) credit, during which sharp increases in developed market yields have led to outflows from EM bond funds – and nearly three years of negative or low returns.

Falling bond prices, though, have meant the higher EM yields on offer have found few precedents in recent history. The hard-currency, sovereign benchmark index[1] yields 8.5%, implying 70 basis points (bps) of monthly carry, while outflows have also meant investor positioning is cleaner.

Higher borrowing costs have resulted in many emerging markets shifting their focus to multilateral agencies, meaning new issuance from sovereigns over 2021, 2022 and 2023 year-to-date has remained lower – even compared to 2020 levels. Looking ahead, 2024 cashflows returned to investors, in the form of amortisation and coupon payments, are forecast to see a 30% plus increase.[2]

Support from yields, technicals and macro

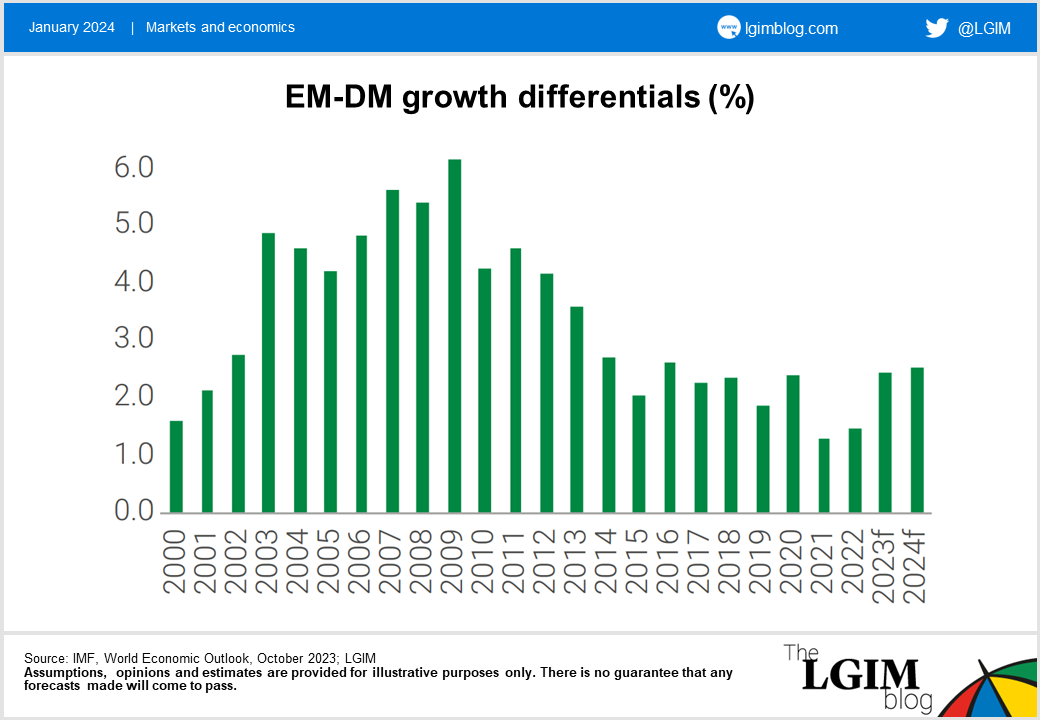

According to the International Monetary Fund (IMF), and despite sharp monetary tightening over the last two years, headline EM real GDP growth is forecast to come in at 4% this year and expected to stay at this level for 2024. This implies that growth differentials, relative to their developed market peers, will rise to 2.5% – increasing for the third consecutive year to the highest level since 2016.

Meanwhile, government debt in EM is forecast rise to 69% of GDP – about 2% higher than last year – but significantly lower than the 113% of GDP pencilled in for advanced economies.[3] This increase is, in fact, driven by just a few large economies, making the country-bycountry picture considerably better than suggested by headline data.

The strength of emerging markets is also apparent in external sector dynamics. Trade surpluses are running at about $550 billion, some $100 billion lower than the peak, but still close to their highest levels. This, coupled with the rebound in tourism, implies that EM current account surpluses will persist this year and next at about 0.5% of GDP, according to the IMF. That’s better than pre-COVID levels, which typically saw modest deficits.

In addition, emerging markets have enjoyed strong support from multilateral institutions, such as the IMF and the World Bank. This not only provides cheap financing, making up for closed capital markets, but also acts as an anchor for policy reforms.

Importantly, these dynamics have also meant that EM FX reserves remain healthy at $10.3 trillion, almost $500 billion higher than pre Covid (end 2019) levels, and equal to nearly 3x the level of external debt amortization due in 2024.[4]

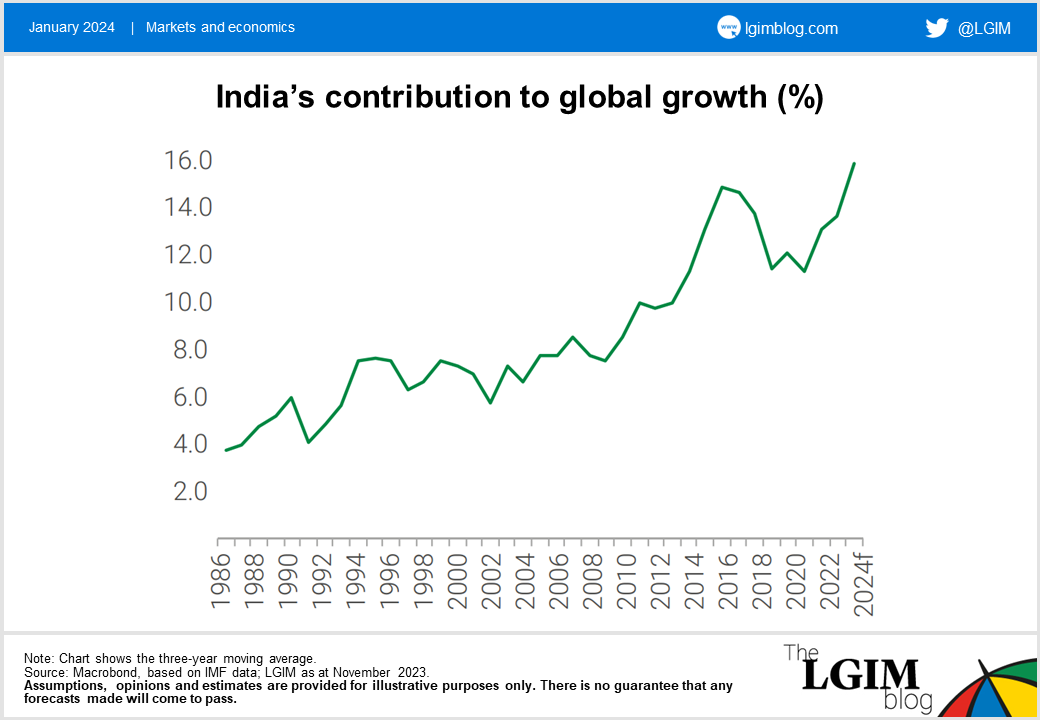

India – a key driver of emerging market growth

A key driver of the growth resilience in emerging markets has been India, where real GDP has expanded in recent years at the fastest pace among large economies. These growth dynamics are underpinned by a vibrant economy, driven by a resilient private sector and a government focused on reforms and addressing the infrastructure deficit.

India heads to elections next year, where the incumbent Bharatiya Janata Party is likely to secure another term. The question is the extent of the majority the party will likely win in parliament – as that will determine the pace and scale of reforms.

The government’s track record on the latter has not only aided growth but has also led to India’s forthcoming inclusion in the JPM GBI-EM Global Diversified Index, and potentially other indices. When this happens, we expect capital inflows to rise, helping to lower domestic borrowing costs for the government and private sector, further boosting growth dynamics.

The above is an extract from our latest CIO outlook.

[1] Source: JP Morgan EMBI GD Index, October 2023.

[2] Source: JP Morgan, October 2023.

[3] Source: IMF, World Economic Outlook databases, October 2023

[4] Source: Bloomberg, as at 13 November, 2023

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.