Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Crowding out?

With massive issuance from governments and companies – most notably hyperscalers, is there a crowding out theme emerging in bond markets?

This article is an extract from our Q1 2026 Active Fixed Income Outlook.

We have firmly entered a new year and the key question on investors’ minds is: what does 2026 have in store? As I started to put some initial thoughts down on paper, what surprised me the most is how little I mention growth, inflation, monetary policy or any other classic market drivers. Instead, it’s clear that this year will be shaped by the continued rise of artificial intelligence (AI) and sovereign debt dynamics.

As I touched on in our last outlook, we’re seeing AI capital expenditure (capex) at extraordinary levels, and this has a significant macroeconomic impact – both for the US and globally. So, I find it hard to get too bearish on US growth expectations when most of the positive impact from this AI spending is still ahead of us – we believe we should start to feel some of this when the big tech companies continue to raise debt and redeploy it back into the economy, supporting activity and growth.

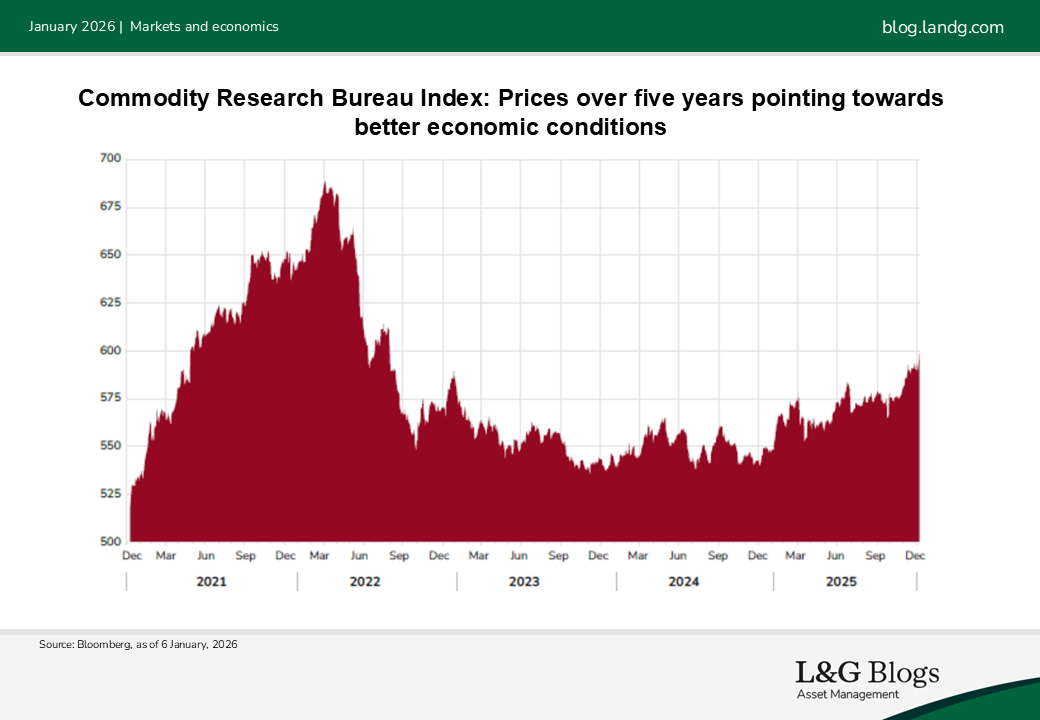

There is also one small glimmer of hope in economic fundamentals: a sign that growth expectations outside of the US might be quietly improving. The Commodity Research Bureau’s Spot Raw Industrials Index, a leading indicator of economic activity, tracks basic materials used directly in manufacturing and industrial processes. The underlying prices come from actual traded spot transactions, giving a better picture of real-world supply/demand pressures for these materials. We believe this points to an improving environment globally as we enter 2026.

Another noteworthy development is the onset of US bank deregulation nearly 20 years after the global financial crisis. Any student of economic cycles with their booms and busts will tell you that while they all differ, there is one common theme: we tend to see a particularly challenging period once every few decades. So this raises an important question: are we late cycle or approaching it? If we are, then we believe we should acknowledge it in our investment decisions and risk taking as the odds for the investor changes significantly depending on where you are in the cycle.

Big tech bonds

There is, however, a circularity to all this. To date, the hyperscalers have financed this investment through their own cashflow, alongside a very willing private credit market. Going forward, the public markets are going to have to step up because the sums involved are so much bigger now and the technology sector needs to broaden out its investor base.

We got a little taste of what this might feel like in October and November 2025, when in relatively short order, we saw around $85 billion of issuance from Oracle*, Amazon*, Meta* and Google*. There was some indigestion, which has now largely passed. Most of the bonds – aside from Oracle – currently trade modestly tighter or around the level where they were issued[1]. Microsoft* is notably the only hyperscaler that has yet to announce a bond issuance to fund its AI spending, but we believe this is only a matter of time.

This circularity matters. If there are any signs that credit markets aren't willing to finance this, or step back because tech companies are not spread sensitive, or if the debt becomes progressively cheaper, then this could seriously undermine the AI capex tailwind for growth.

Perhaps unsurprisingly given how dominant the theme is, we explore AI-related issuance in more detail in the following pages: on page 7 our Global Unconstrained Bond team focuses on positioning implications and on page 23 our Research and Active Engagement team details the Meta* mega data centre deal.

M&A matters

But substantial levels of bond issuance and capital raising extend beyond the AI and technology sector – it’s a trend affecting companies more generally. After hitting its lowest level in more than 30 years in 2023, merger and acquisition (M&A) activity is making a comeback. The third quarter of 2025 saw announced deal volumes surge by 43% year on year and crucially large strategic transactions leading the way – this tells you that corporate confidence has also returned.

This is particularly relevant considering the current stage of the economic cycle. Credit investors tend to sleep easier at night when M&A activity is muted because there is less risk of companies taking on too much debt which could affect their credit ratings.

Paramount’s* high-profile hostile takeover bid to acquire Warner Brothers Discovery* in December 2025 only fuels the comparisons between the current cycle and the late 1990s dot-com bubble. I’m sure many of you will remember AOL’s* disastrous takeover of Time Warner in 2000 – I certainly do. The increase in M&A activity across sectors will be something credit investors need to monitor carefully.

Fiscal is fab?

Our central investment thesis since the COVID-19 pandemic is that there has been a seismic global shift from monetary policy to fiscal policy. Governments that are currently sitting on large deficits will need to focus on growth – austerity is not an option.

We have left 2025 with Germany and Japan joining the ‘Fiscal Is Fab’ club, with the former releasing their debt-brake and the latter electing a pro-fiscal policy prime minister. This on top of the US’s own fiscal expansion with the One Big Beautiful Bill – are we seeing a new paradigm?

Fiscal sustainability is firmly on the market’s radar. The challenge for investors is determining whether we’re seeing a plausible path to a crowding out theme developing in bond markets – where increased borrowing can lead to a surge in the supply of bonds. This in turn can push up interest rates, making it more expensive for other borrowers to raise funds. Issuance will be coming at us from governments, companies across sectors, but most notably hyperscalers. Credit investors will need vigilance and agility to navigate the next chapter unfolding in bond market history.

This article is an extract from our Q1 2026 Active Fixed Income Outlook.

[1] As at 7 Jan 2026

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitutea recommendation to buy or sell any security.

Key risk

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass. The value of an investment and any income taken from it is not guaranteed and can go down as well as up, and the investor may get back less than the original amount invested.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.