Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

In recent months investors have grown increasingly concerned about the potential for AI to disrupt traditional software business models. New releases in AI models such as Anthropic’s[1] Claude have prompted a reassessment of how resilient software firms are. For credit investors, the issue is particularly relevant: software represents a meaningful share of US collateralised loan obligation (CLO) exposures. Understanding whether the perceived disruption risk is justified is therefore crucial when evaluating potential vulnerabilities and opportunities across CLO portfolios.

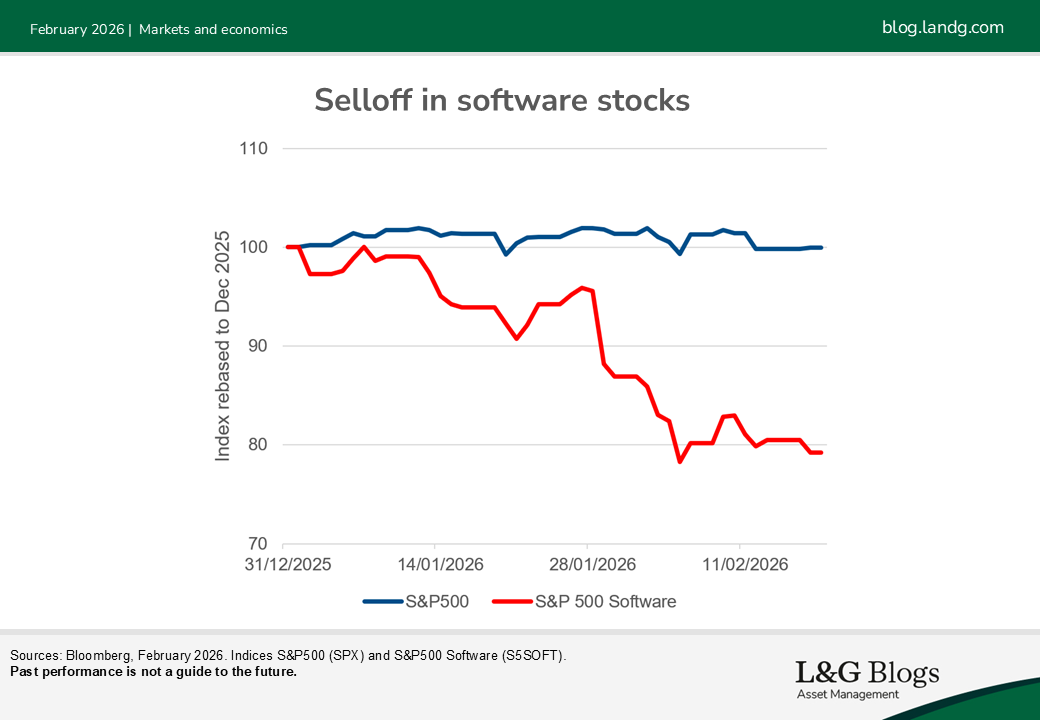

Sell first ask questions later

A wave of indiscriminate selling has recently hit software stocks on fears that generative AI could cannibalise software companies’ business models.

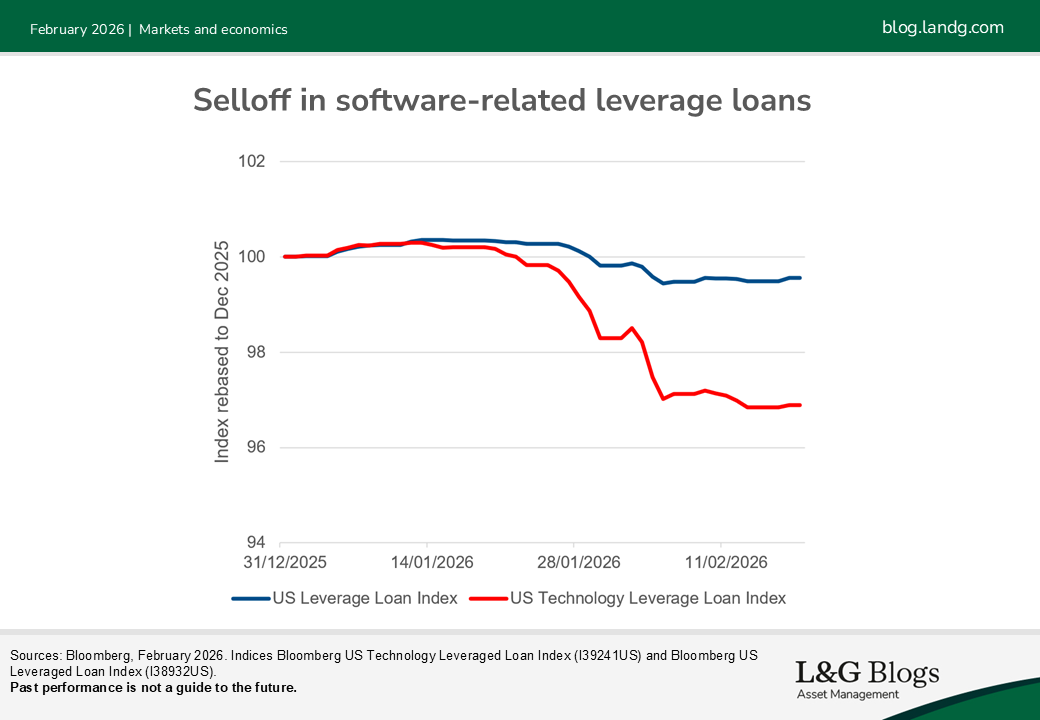

Software and software as-a-service (SaaS) leveraged loans have also fallen this year so far amid selling by CLO managers and loan funds reacting to the tech turmoil. Year-to-date (mid-February), US and European technology loans (which include software) are down roughly 3% versus a flat broader loan index. 11% of technology loans within the Bloomberg US Leveraged Loan Index are now classified as distressed based on trading levels, up from approximately 6% at year end[2].

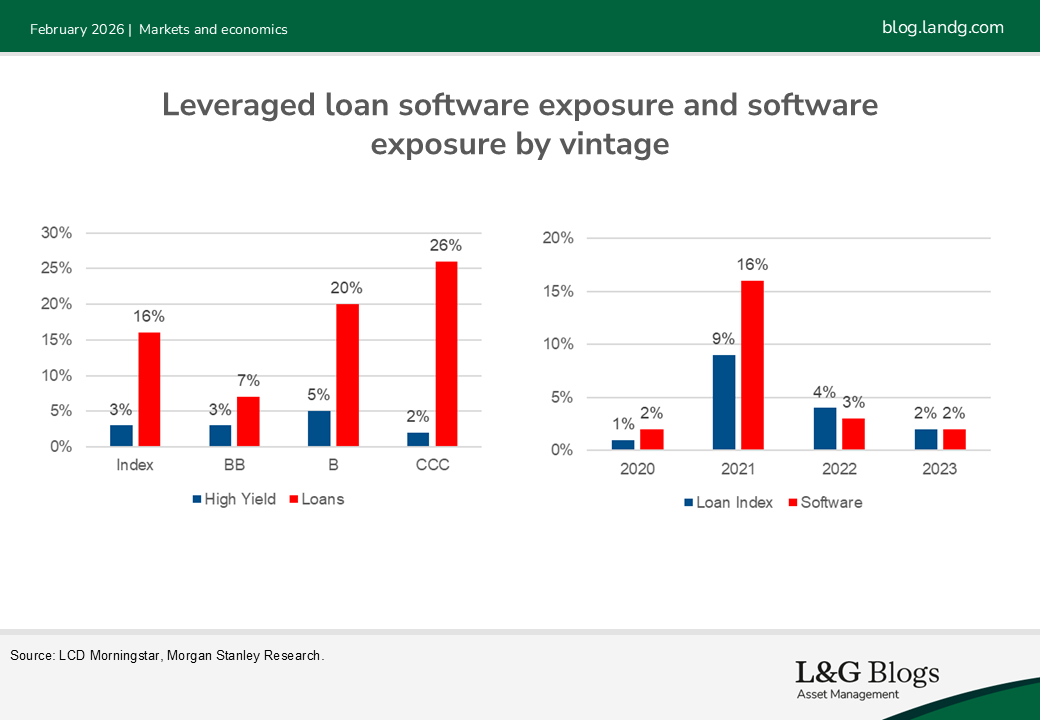

Concerns around software loans are not totally without justification, in our view. Loan market software exposure is skewed towards lower-rated single B and CCC rated loans and is concentrated in the 2021 vintage, with roughly 16% of loans originated in 2021.

There is also considerable dispersion in the performance of software loans. The sector is broad, and some business models are far more exposed to AI‑driven disintermediation than others. Enterprise software providers, with deeply embedded customer relationships and sticky, mission-critical revenue streams, appear relatively insulated. By contrast, certain application‑based software firms may face greater competitive pressure, depending on how close their products sit to the underlying data and how large the total addressable market (TAM) is.

Broadly speaking, the closer a company is to the data and the smaller its TAM, the lower the risk of meaningful AI substitution. And if we also consider software‑adjacent issuers, such as a healthcare services company that supplies software into hospital workflows, the proportion of issuers that face disruption risk increases.

What’s the size of software exposure in CLOs?

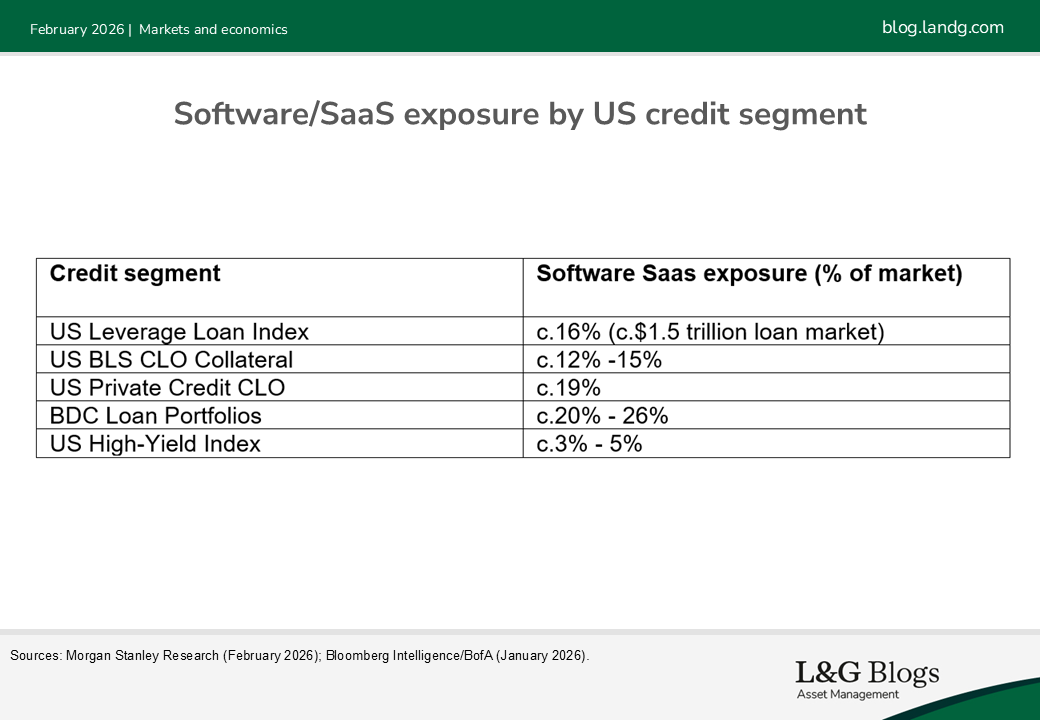

CLOs are major holders of sub-investment grade software loans. In the US loan market, software now accounts for roughly $235 billion of loans (c.16% of the $1.5 trillion leveraged loan index), making it one of the largest single sectors. By contrast, software-related issuers represent only about 3.5% of the U.S. high-yield bond universe. Software companies have tapped the leveraged loan market heavily in recent years, funding a surge of private‑equity buyouts that were underpinned by the appeal of subscription‑based revenues, and potentially attractive margins and steady cash flows.

Resilience of CLOs

Despite negative sentiment in software loans, CLOs have numerous features that seek to protect senior tranches:

- Structural credit enhancements: CLOs are built with substantial loss-absorbing buffers. ‘Subordination’ is a feature whereby equity and lower-rated junior bondholder tranches serve as credit support for the higher-rated senior bonds absorbing all losses from defaults on the underlying loans first. This resilience is bolstered by over-collateralization and interest coverage tests: if too many loans default or migrate to CCC ratings, excess cash is diverted away from equity to pay down the senior notes early, preserving their principal. As a result, senior CLO tranches (AAA through A) have had zero impairments in the modern era – since 2010 (Moody’s Impairment and loss rates of structured finance securities survey).

- Diversification[3] and concentration limits: By design, CLO collateral pools are spread across 100+ issuers and diverse industries, with explicit limits on maximum industry exposure (typically 10–15%). This means no single sector’s woes – even a big sector like software – can overwhelm the portfolio.

- Reinvestment flexibility: CLOs are actively managed and the CLO manager can reinvest principal proceeds into new loans for several years. Hence the CLO manager has the ability to adjust the CLO portfolio to changing conditions or opportunities – reducing exposure to risker areas or taking risk when areas of the market look relatively cheap.

Portfolio implications

Software typically represents 12–15% of CLO portfolios, making the sector’s potential AI‑related disruption an important consideration for investors. Although default rates among software borrowers remain low for now, heightened concerns about AI substitution combined with challenging capital‑market conditions could increase refinancing risk for the many software issuers with debt maturing over the next three to four years.

For CLO investors, any deterioration in credit performance is most likely to be felt lower down the capital stack, where equity and mezzanine tranches are the first to absorb losses. By contrast, senior CLO tranches can potentially benefit from structural protection[4] and active portfolio management, providing cushions that could help them withstand even a moderate rise in software‑related defaults.

[1] For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

[2] Source: Bloomberg intelligence credit strategy dashboard (BI STRTN), Leveraged Loan Data library as at 16 Feb 2026.

[3] It should be noted that diversification is no guarantee against a loss in a declining market.

[4] References to protection and structural protection are general strategic terms. There is no protection guarantee. Past performance is not a guide to the future. The value of an investment and any income taken from it is not guaranteed and can go down as well as up, you may not get back the amount you originally invested.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.