Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Active Fixed Income outlook: An unexpected rotation

2025 began with the US unexpectedly yielding leadership to Europe and China; how else could markets defy expectations?

This article is an extract from our Q2 2025 Active Fixed Income outlook.

In the final weeks of 2024, if you said that by the end of February US markets would not only underperform the rest of the world, but that the market’s least loved countries (China, the UK and Europe) would be leading returns for the year to date, nobody would have believed you.

This rotation has been around a rising trend – albeit with the leadership stocks and sectors losing momentum and starting to underperform. Markets have been relatively insulated to headline risk as positive investor sentiment continued to protect markets from the noise. Despite the blizzard of policy announcements from the new administration in the US, there has been little concrete evidence of any lasting economic damage at this stage. We believe it has been hard to find any data trends that capture the impact of policy announcements, partly because there have been more announcements than actual implementation. This is now changing. The threat of a US growth inflection point may be approaching and there has been little allowance for policy risk in valuations.

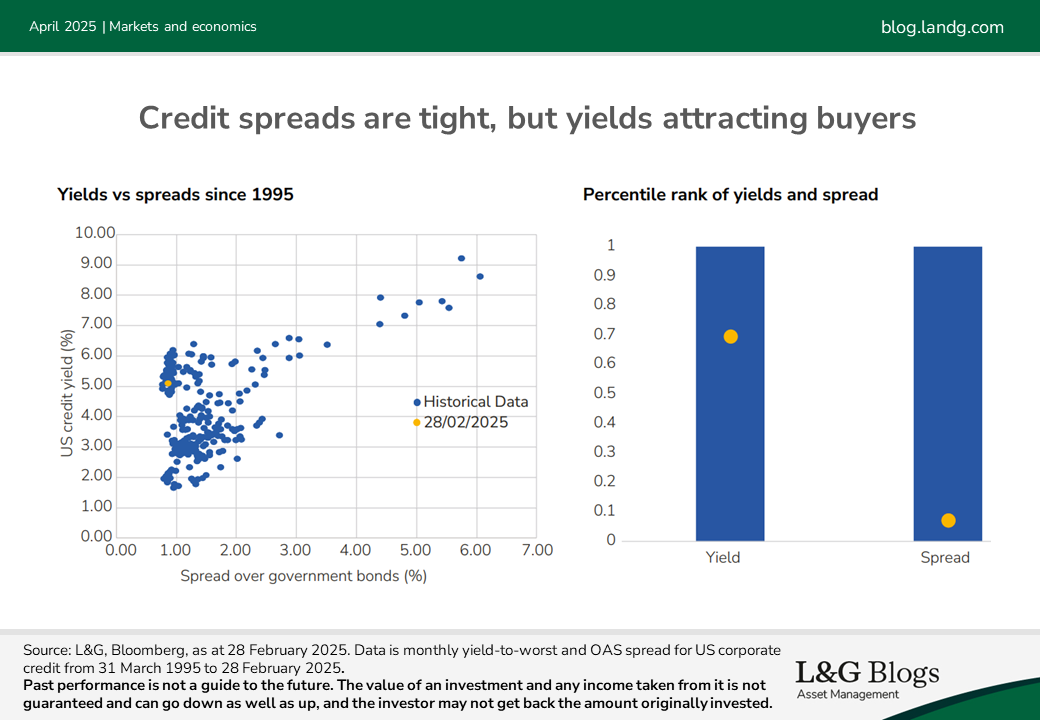

In fixed income markets, investors are still having to deal with the uncomfortable combination of tight credit spreads and total yields that continue to attract significant inflows to the asset class.

Playing chicken?

For pure credit spread investors, this feels like a game of brinkmanship.

Valuations are rich but the underlying fundamentals are not suggesting portfolios should be moved to outright bearish positions. Whether you believe the change in the US administration has signalled the beginning of a new cycle or not, you cannot ignore the unattractiveness of credit spreads in isolation. However, we have to play the market as it is, and not how we would like it to be.

We feel a derisking strategy is prudent, recycling risk into higher-quality exposures where reasonable credit spread is still on offer. We like exposures to emerging market debt as the fiscal sustainability debate will remain a live issue in developed economies. In looking for red flags, we struggle to see many. Leveraged loan default rates are running at three time the high yield market and worthy of monitoring, but we think investment grade credit should remain lower beta than other risk asset classes.

You could argue that general investor bullishness is more about equity prospects than actual GDP growth. That said, the impact of a heightened sense of chaos and uncertainty from the new US administration is neither good for investment nor broader animal spirits. We think investors should expect the unexpected in 2025 as confusion around the Trump administration’s actions will continue to have an influence over market outcomes.

This article is an extract from our Q2 2025 Active Fixed Income outlook.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.