Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Fiscal fault lines: how debt sustainability fears may shape 2026

After years of fiscal largesse, the ‘debasement trade’ has gained significant momentum, just as AI fuels an extraordinary wave of capital investment.

The following is an excerpt from our 2026 global outlook

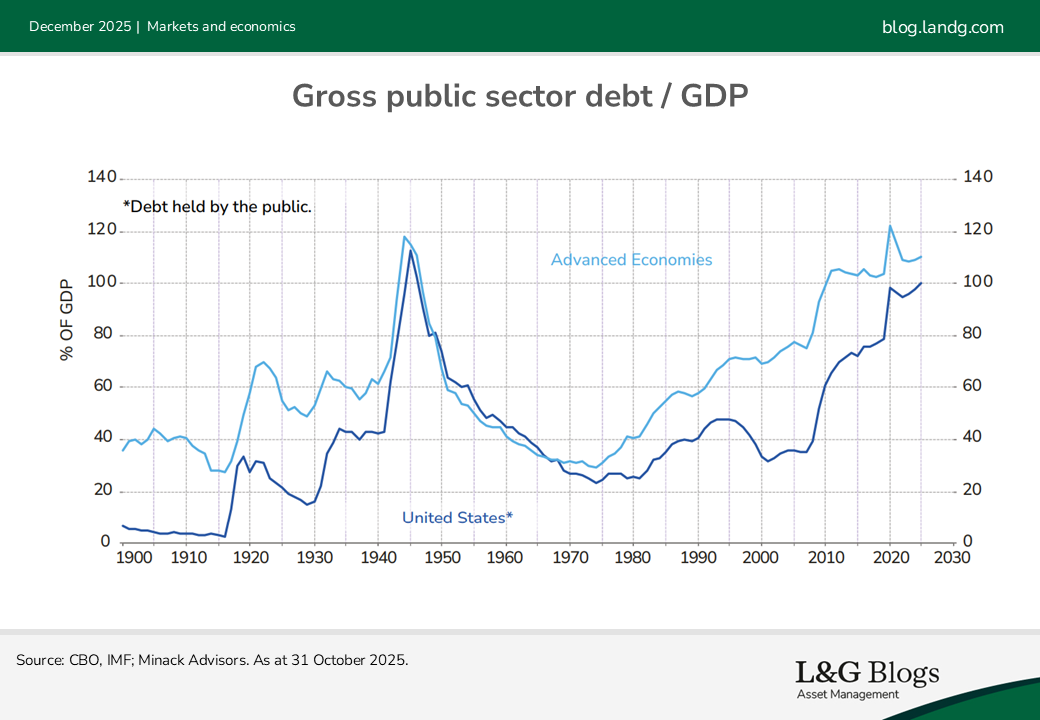

A surge in government debt during the pandemic enabled developed economies to survive the crippling impact of lockdowns on economies. But it also reminded politicians that giving money to the electorate sometimes translates into votes.

Perhaps unsurprisingly, therefore, debt has reached levels not seen since the Second World War.

In the US, despite persistent calls for fiscal consolidation by Democrats and Republicans, there appears to be little appetite to curb spending, and the fiscal deficit remains elevated.

Enter the bond vigilantes

The post-pandemic boom coincided with an energy price spike following Russia’s invasion of Ukraine, leading to inflation and rising rates. The ‘bond vigilantes’ returned amid concerns about inflation and debt sustainability, resulting in a sharp increase in longer-term funding costs.

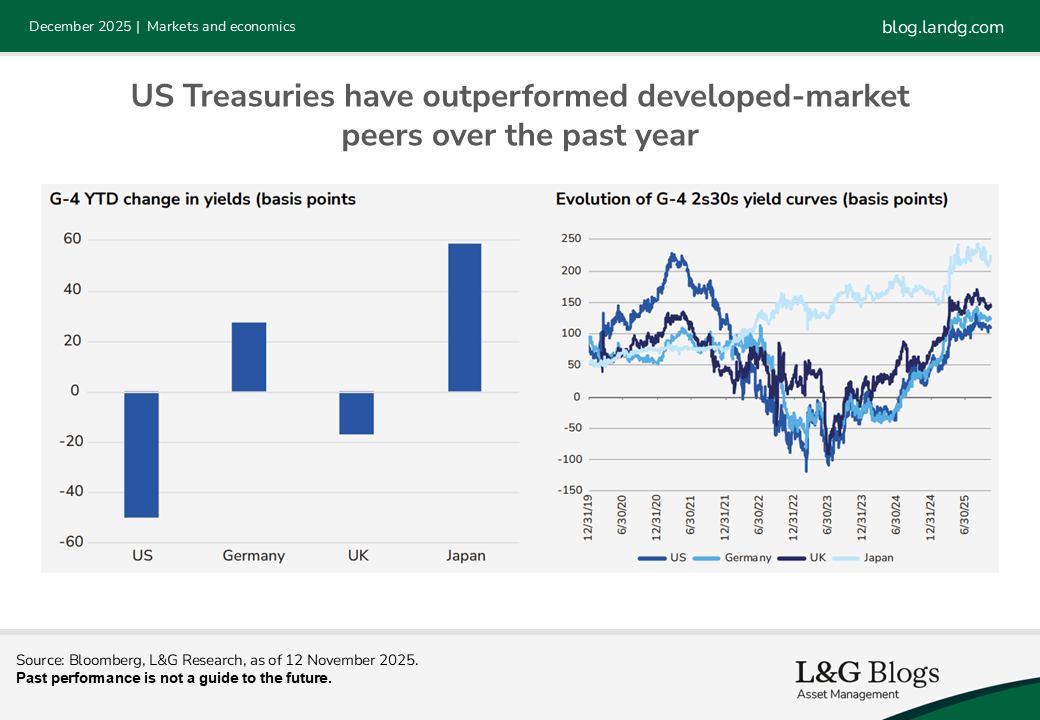

In the US, worries around a looming debt crisis spiked shortly after the tariffs-related ‘Liberation Day’. However, although US largesse has dominated headlines, investors have become increasingly wary of the deteriorating fiscal position of other G10 markets.

The material repricing in the term structure of rates is not just a US phenomenon – term premiums have risen even more abroad.

For some time, we have believed that governments are not incentivised to issue the most expensive debt. And this is what has happened over the past few years – the proportion of shorter-dated debt has increased.[1]

Keeping the peace with bondholders

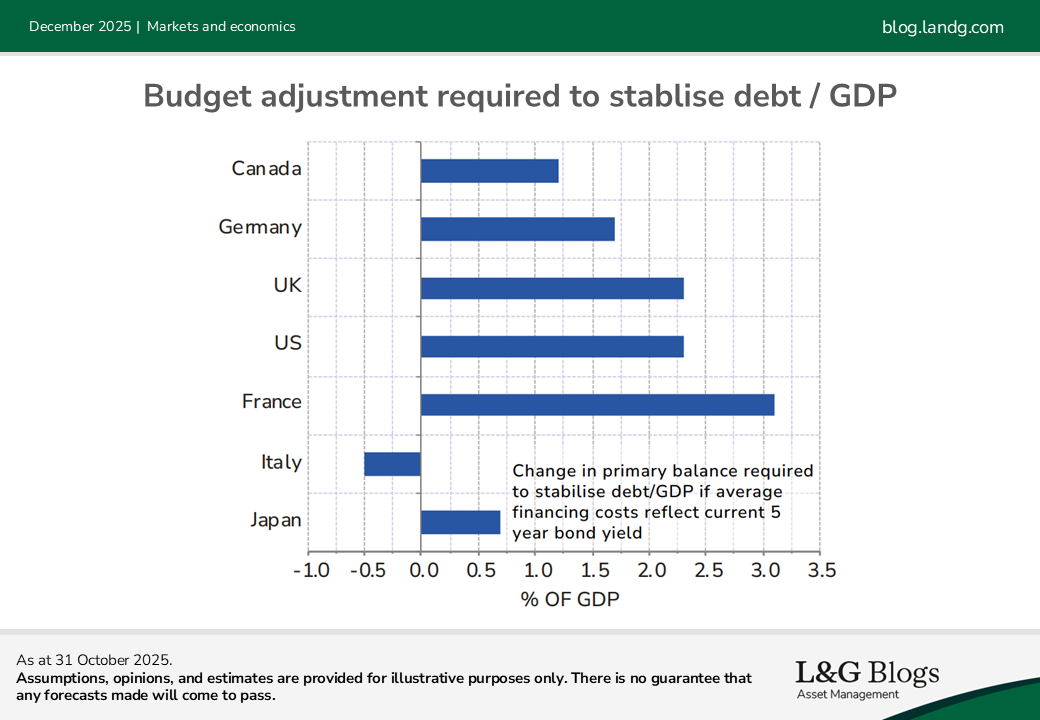

Although fiscal austerity is not politically fashionable, the stirring of the bond vigilantes is nudging some governments to respond.

The UK is aiming to maintain a fiscally neutral budget by the end of parliament, while the new Japanese premier is also trying to contain expectations over huge fiscal spending.

Apart from France, the budget adjustments required by governments are not massive by historical standards, but we are not yet seeing many signs that increasingly populist governments will accept the pain.

In the US, the One Big Beautiful Bill Act is projected to increase the deficit by $3.4 trillion over 10 years, according to the Congressional Budget Office, largely owing to reduced federal tax revenues. Consequently, the technical backdrop will remain a headwind for Treasuries.

While the end of quantitative tightening should provide some modest relief, price-sensitive buyers will likely continue to demand additional compensation to take down long-term debt amid elevated policy uncertainty and two-way inflation risks.

What happens next?

The rollover of debt mountains could become an issue for countries whose average debt maturity is short. Most developed markets are not yet near this position, but that could change over the next few years.

Apart from an unexpected outbreak of fiscal austerity, investors should also watch out for indications of financial repression or engineering to finance deficits.

We note that the US promotion of stablecoins (often backed by short-term government debt) and the easing of US bank capital regulation (enabling banks to hold more treasuries) should help the government fund its fiscal deficit.

Finally, a return of quantitative easing could also assist in financing deficits, but this would most likely require some form of market or economic shock. Governments (and investors) should be careful about what they wish for!

The role of Treasuries in 2026

The ‘debasement trade’ has become increasingly topical amid the surge in gold and crypto prices. While fears over government debt and expansionary monetary policies eroding the purchasing power of fiat currency are not without merit, we still see a place for US Treasuries.

With yields well above post-global financial crisis averages, and the US policy rate generally viewed as modestly restrictive, we believe short-dated Treasuries can serve as an effective hedge should risk assets come under duress and / or the economy tip into recession.

Moreover, if this year is any indication of the market’s assessment of fiscal risk, investors can take comfort in the notion that the US is still seen as the ‘cleanest dirty shirt’.

AI spending in focus

In tandem with the sovereign debt dynamics discussed above, AI is fuelling an extraordinary wave of capital investment.

The AI capex boom is well underway, and even with tech companies funding a healthy portion from their free cash flows, the revolution will be heavily funded by debt. This deluge of supply is not only likely to exert widening pressure on spreads, but may also put upward pressure on risk-free rates.

According to Morgan Stanley,[2] global data centre expenditure is projected to reach about $3 trillion by 2028, which translates to ~$1 trillion in annual investment demand by 2028. For context, the total capital expenditure of all S&P 500 companies in 2024 was only about $950 billion. Most importantly, Morgan Stanley expects $800 billion of supply to flow through private credit markets by 2028.

At the same time, the recent bankruptcies of First Brands and Tricolor have created a lot of anxiety over the health of the private credit market. In fact, both were deep sub-investment grade (“IG”) borrowers – so their bankruptcy had little impact on IG private credit. They also sought most of their financing from banks and working capital funds; sub-IG private credit exposure was very limited.

Idiosyncratic cases like First Brands point to emerging cracks, but there’s no clear evidence at the moment pointing to broader stress in sub-IG private credit, in our view. Default rates in direct lending remain low and falling interest rates should support debt servicing. Nevertheless, recent events have been a useful wakeup call and once again emphasise the importance of robust underwriting and portfolio diversification. We think investor caution should drive better underwriting standards, which could lead to improved credit performance for future vintages.

2025 is the year when the AI revolution truly reached private credit. Several multi-billion deals were announced, including Meta’s $29bn AI data centre financing and Microsoft’s $30bn partnership with BlackRock.[3] This is not a fleeting trend: we expect further growth in private credit financing of digital infrastructure in 2026. The surge in debt supply could shift negotiating power in favour of lenders, which would be welcome news for investors after several years of spread compression and covenant erosion.

However, there are plenty of risks associated with the sector – cost volatility, obsolescence risk and overcapacity, to name a few. For investors, we believe the opportunity lies in targeting private credit strategies that capture the structural tailwinds of AI-driven infrastructure, while maintaining disciplined risk management in a rapidly evolving market.

Read our 2026 global outlook

[1] Refer to chart C on page 28 of the 2025 OECD Global Debt report.

[2] As at July 2025

[3] For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.