Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Am I on your Christmas card list?

Consumer preferences on sending cards are shifting – we discuss the effect this is having on card retailers.

We’re speedily ushering in Christmas. In the vocals of Andy Williams, "It's the most wonderful time of the year – there'll be parties for hosting, marshmallows for toasting, and carolling out in the snow."

Yet as many of you will attest, one of the less exciting Christmas activities is sitting down to write lots of Christmas cards. Not only is it time consuming, but if you need to post them it’s expensive too.

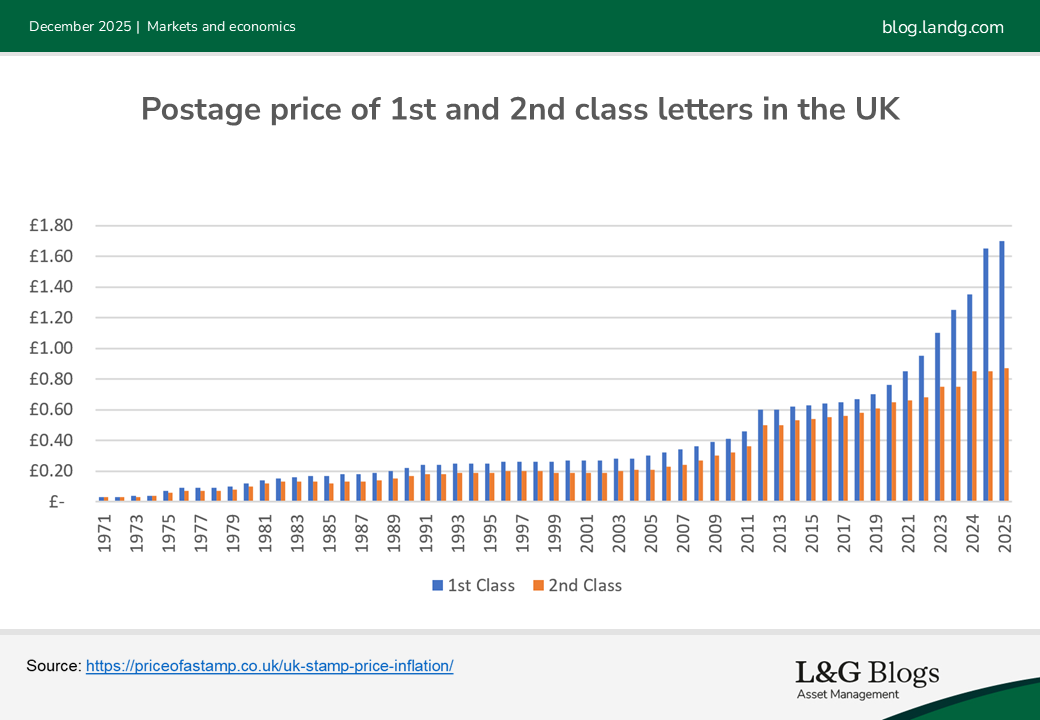

The chart above depicts the dramatic increase in the price of stamps in the UK over the past five decades. From the turn of the millennium until now, the cost of a second-class stamp has risen 358%, while the cost of a first-class stamp is 530% higher.

Over this time, UK inflation as measured by Consumer Price Index (CPI) is only up 92%[1]. Since postage cost increases have far outpaced general inflation, it seems plausible that consumers might be rationalising their Christmas card lists.

The alternatives of sending emails or text messages have the potential benefits of being quicker to write, instantaneous to receive and free to send. As a result, the volumes of greeting card sales in the UK market are declining[2]. This begs a key question…

Does this mean the demise of greeting card companies?

We firmly argue not. Even though the landscape is highly competitive and has changed considerably, there is no shortage of current growth opportunities for card companies.

As with any changing industry, the nimble companies that adapt are the ones that can win market share. This view was corroborated by our recent engagements with the management teams of UK-listed card companies, which highlighted three reasons to be cheerful about the future of the industry.

An untapped market

The card market in the UK is ripe for transition to online – only 6% of cards are sent online[3].

Online offers greater convenience as well as the chance to personalise (alongside various delivery options to suit even last-minute customers), which can lead to a feeling of getting more value for money for the same postal cost.

Moonpig*, which holds a 70% market share among UK online card specialists[4], has a strong technology platform, which is critical for winning in this space. 88% of card purchases are tied to annual events[5] such as birthdays, anniversaries and national celebrations. Therefore, successfully harnessing customer data can result in a defensible moat via reminders and engagement at peak purchase intent moments, driving strong customer retention.

Add-on sales

Secondly, the strategy of these businesses seeks to offset the slow decline in card volumes by tapping into gifts and other celebratory items, including wrapping paper, balloons, tableware and gift bags. Card Factory* has been allocating more store space to non-card items (now more than half of their sales[6]), while Moonpig* has linked up with external brands to offer a selection of presents.

Regardless of offline versus online, attached gifts are a key growth driver for all these businesses, and yielding greater like-for-like growth and improved average basket values. The focus of these businesses is how to correctly maximise this adjacent vertical, given the magnitude of the gifting market opportunity. One route has been acquiring gifting and experience brands, such as Moonpig’s* current ownership of Buyagift* and Red Letter Days*, and Card Factory’s* recent purchase of Funky Pigeon*.

Partnership and overseas opportunities

Card companies can also sell their products beyond just their own stores and websites, via partnerships. Whether it is Card Factory’s* supply of cards to Aldi*, or Moonpig’s* new corporate card-giving proposition for businesses, these are incremental profit pools which are being accessed.

Finally, international expansion is another important growth driver. Moonpig* own the Greetz brand in the Netherlands, and sells into Ireland, the US and Australia too. Card Factory* has made targeted acquisitions to increase its international presence as well.

Too easily dismissed

Active equity selection involves trying to uncover fundamental opportunities which have been overlooked. The card market is at risk of being one of these overlooked areas due to the headline reduction in greeting card volumes. Yet this ignores that the cards market is growing due to average selling price, and capturing market share of the adjacent gifting vertical is the big prize.

Our thesis embraces the potential for scale players to win through a combination of international expansion, partnerships and focused strategy. As a result, we continue to admire the fundamentals of these types of businesses, most notably their potential to continue to earn high returns on capital.

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

[1] Bank of England Inflation Calculator: https://www.bankofengland.co.uk/monetary-policy/inflation/inflation-calculator. Data to October 2025.

[2] Moonpig: https://www.moonpig.group/about-us/our-markets/

[3] Ibid. This 6% relates to volumes. 15% of UK card market value is transacted online.

[4] OC&C Strategy Consultants, 15 October 2024: https://www.moonpig.group/media/3jdotsjv/moonpig-cmd-support_151024_vfinal.pdf

[5] Moonpig, Annual Report & Accounts 2025: https://www.moonpig.group/media/xfpd5o4c/moonpig-group-plc-annual-report-2025-full-version.pdf

[6] Card Factory, 7 May 2025: Gift and celebration essentials now represent 50.2% of total sales, with approximately one in every two baskets now containing a gift or celebration essentials product. https://www.cardfactoryinvestors.com/media/mkbkl4jj/cardfactoryfy25prelimsrnsfinal.pdf

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.