Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

EMs and Hormuz: who is most affected?

The energy shock accompanying the Hormuz closure places many emerging markets (EMs) in the lurch.

The conflict in the Middle East continues to have stark effects in commodity markets. Brent oil prices surged from $60 in early-January to over $100 in late-March, the highest price since the Russian invasion of Ukraine in early-2022.

As sharp as this move has been, it’s more pronounced in refined products like gasoline and jet fuel, as refineries geared to handle the Gulf’s heavy crude start to run dry. Nor does this consider the effects on other energy-dependent materials such as fertilizer and helium, both vital in agriculture and semiconductor fabrication respectively, which have also been put under pressure by the crisis.

If the conflict continues into weeks and months, current price action could potentially lead to more serious breakages in commodity markets and pain for consumers.

Who could be at risk from the rise in oil and gas prices?

While many developed markets have either weathered similar crises before (in Europe) or may even potentially stand to benefit (Australia, the US), the primary losers of the struggle over the Hormuz could be poorer emerging markets (Ems), particularly in Asia.

As principal users of Gulf oil, their energy security is most imperiled by the collapse in supply, creating sharp short-term pain as they rush to find alternate suppliers. Poorer countries also lack the flexibility to finance (even transitory) surges in commodity prices, as borrowing is less forthcoming owing to lesser creditworthiness. As a group, EMs really are at the receiving end of the market implications of the Hormuz crisis.

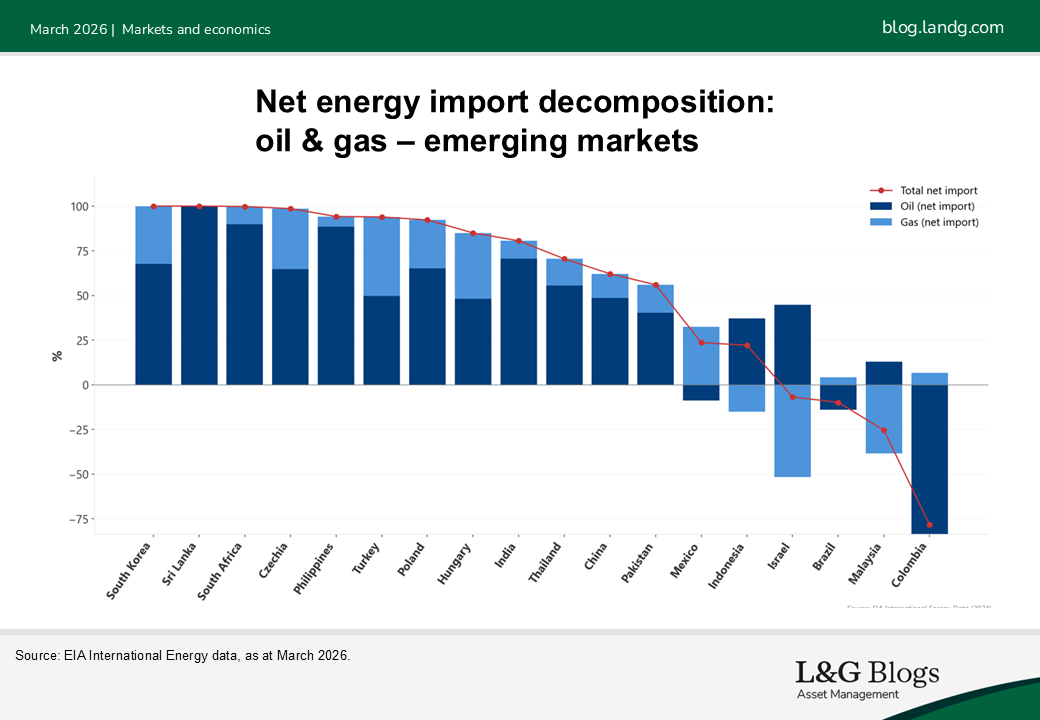

But which ones? In a crisis like this one, exposure comes in various forms. The first is on dependence on imported energy. Many EMs, like South Korea and Taiwan, are stuck as energy importers, whereas others, like Brazil and Malaysia, have oil to export at higher prices than ever before.

The second is stockpiles of crude oil in reserve. The larger the volume of crude held domestically, the more countries are insulated from the near-term effects of the crisis. Lastly, the reliance of the country on external financing. If a country has a substantial buffer of external surpluses, they can weather the shock without relying on external financing.

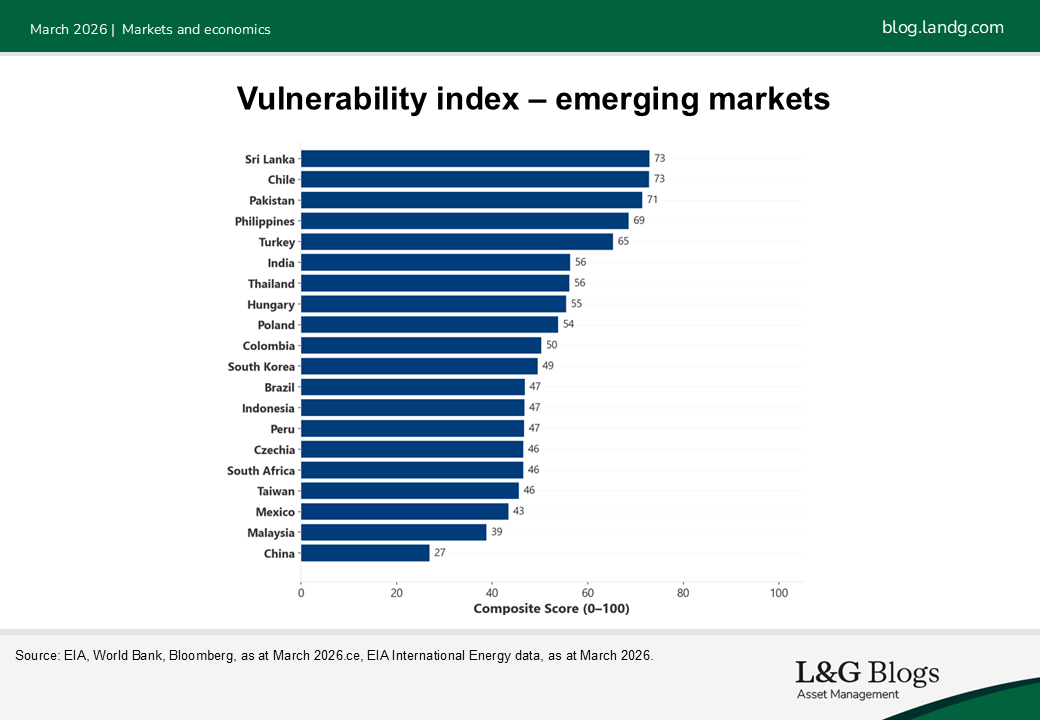

We combine these exposures into a single index. Those EMs which depend on imported energy, with larger external deficits, and smaller stockpiles of oil score higher, and those that are energy and capital exporters, with large oil stockpiles are more secure.

China, with its large current account surplus and relatively large oil stockpile, scores highly, whereas the Philippines and Turkey, with chronic external borrowing needs and dependence on imported energy, are both considered less secure. Meanwhile, Pakistan and Sri Lanka, will likely experience a deeper contraction.

Interruption or stop?

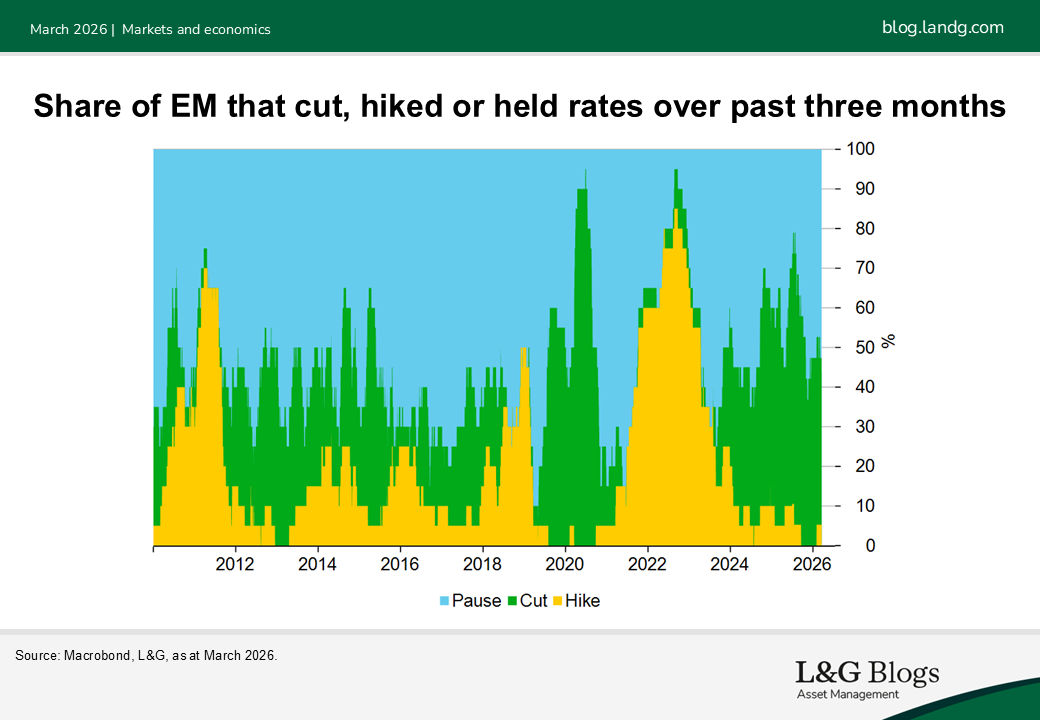

This crisis also interrupts what was a reasonably positive picture for EM in 2026. With domestic inflation falling, the Fed cutting rates and the dollar weakening, EMs were supposed to experience a boom from lower rates and capital inflows. Falling interest rates and easier credit conditions would also have supported still-stretched fiscal deficits across much of EM.

Under the shadow of the Hormuz closure, this scenario now seems remote in our view. In fact, the reverse is happening. The threat of higher inflation will caution central banks (in both DM and EM) to keep rates steady, and even increase in some places. Higher fuel prices will also strain the manifold energy subsidies that are common among emerging markets, worsening fiscal metrics and (if maintained) blunting the demand destruction necessary to weather the shock. Although EMs as a whole are in a good position, with inflation largely within target, withstanding the gyrations in energy markets is going to be a white-knuckle ride.

Weathering the storm

Despite the newsflow surrounding the Hormuz crisis, we remain watchful for opportunities in the EM space where the market might misprice risks as they arise. We believe the market will become more discriminating between countries that are well-positioned in the ongoing energy squeeze and those that are not.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.