Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Emerging markets: Upside risk after a resilient 2025

We identify reasons for cautious optimism and discuss how we think innovative exposure can be achieved.

The following is an excerpt from our 2026 global outlook

Half a year after the US raised tariffs to levels not seen in a century, we are still to see a significant effect on emerging markets.

As at November, exports are growing above 10-year averages for each of the four regional groupings and China, according to Bloomberg data. In our view, front-loading and re-routing probably delayed Liberation Day’s impact.

On the other hand, trade uncertainty should be significantly lower in the lead-up to the US mid-term elections and several large emerging markets (EMs) are still to negotiate tariffs down. We should also note that free-trade negotiations are mushrooming in the rest of the world – a pattern already observed during President Trump’s first term.

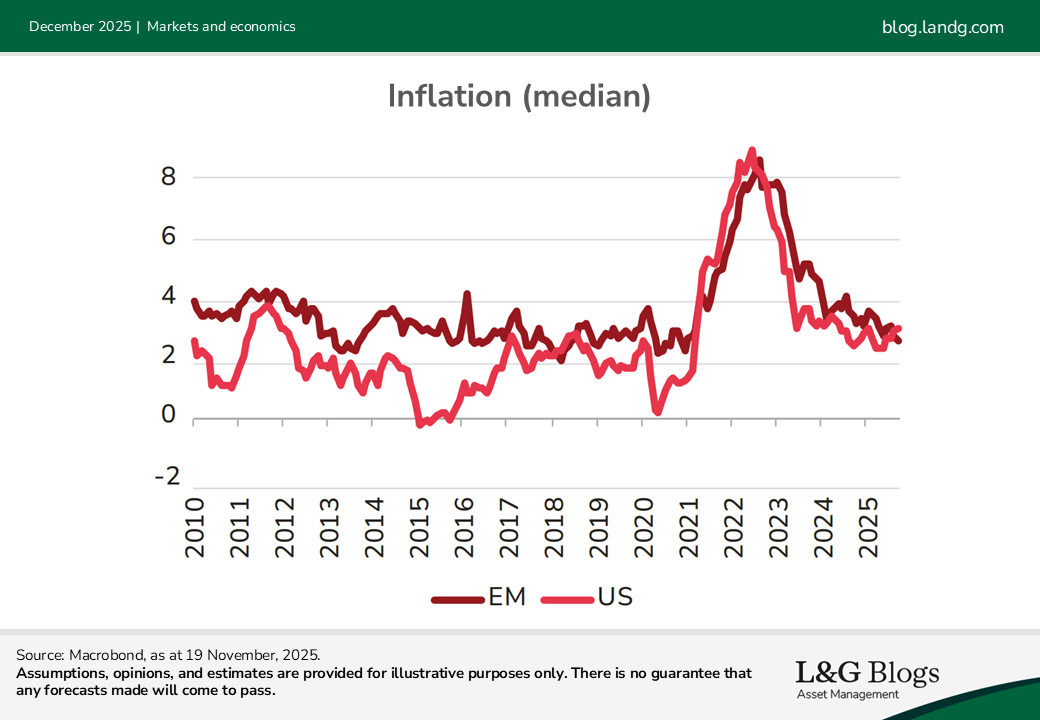

Rate of change

Importantly, with inflation falling and now at par with G7 levels (see chart), we believe emerging markets will continue to cut interest rates. Some 40% of the top 20 cut over since the summer, as at November, with the rest staying on hold. This still needs to feed through to the real economy. On top of that, market consensus is that the US Federal Reserve is expected to ease by 100 basis points over the next 12 months.

Fiscal policy will likely be less accommodative, as the majority of emerging economies still need to return their fiscal balances to pre-COVID levels. Particularly worrisome, in our view, have been the fiscal dynamics in Poland, Colombia and to a lesser extent Indonesia. But there have also been success stories – notably Chile, South Africa and India. Government debt remains much lower in emerging economies than in their advanced peers, including when measured against taxing power.

Next year will see a number of elections that could mark crucial turning points. We believe a market-friendly pivot is most likely in Colombia. Brazil’s election remains a toss-up at this stage, while Peru is likely to remain politically divided irrespective of the outcome. In Israel and Hungary, two leaders who have dominated politics for decades are fighting for survival.

As of October, the International Monetary Fund expects growth of emerging and developing countries to accelerate in 2026. We are sympathetic to this view, as risks look skewed to the upside. Capital flows to emerging markets have been lacklustre over the past decade. Hence, we believe the risk of a sudden reversal in capital flows – perhaps the quintessential crisis for such economies – is low. China has experienced a multi-year property and earnings recession, again suggesting that risks are asymmetric. Finally, we believe the US dollar is more likely to fall than rise given excessive valuations, which tends to boost EM growth.

The debt view

With resilient growth across emerging markets, upward revisions to forecasts, declining inflation, and a robust external sector, we maintain a constructive stance on emerging market debt (EMD) and anticipate continuing to buy on pullbacks as we head into year-end and 2026.

Our confidence is underpinned by structural improvements now being reflected in credit rating trends. Upgrades have outpaced downgrades in 2025, signalling positive momentum. There have been zero sovereign defaults in the last two years, and we expect aggregate default probability to be very low next year, whereas EM corporate default is forecasted at about 3% in 2026, according to J.P. Morgan as at November.

We have also observed investor sentiment towards EMD improving. Global liquidity conditions have strengthened, and after years of significant outflows, EMD funds are now seeing renewed inflows, EPFR data indicate as at November. Notably, crossover investor allocations to EMD have risen from 8% to 15% over the past three years, Bank of America, also as at November.

Given this backdrop, we see limited risk of a sharp widening in EM spreads. Despite record issuance this year, spreads have compressed, indicating strong demand for the asset class. Even CCC rated issuers such as Suriname, Laos, and the Republic of the Congo have successfully accessed markets, underscoring investor appetite for EM paper.

Relative value

From a valuation standpoint, while spreads remain tight, we find all-in yields compelling and see them as a more reliable indicator of potential forward returns, in our view. We also expect solid EM fundamentals to help contain any spread widening.

With subdued growth, a softening labour market, and weak oil prices in the US, we, like other market participants, also anticipate continued rate cuts by the Fed. This should help keep rates from rising meaningfully, supporting our expectation of mid-to-high single-digit total returns in EMD for 2026.

Looking ahead, key risks for EM in 2026 are likely, in our view, to stem from US markets and macroeconomic developments – particularly a possible resurgence in inflation and elevated AI-driven equity valuations.

Recent volatility in US equities has already had spillover effects on EMD and broader risk assets in Q4 2025, and we remain cautious of similar episodes next year. Consequently, our positioning is more selective than in previous cycles, with a focus on idiosyncratic opportunities (for example, oil importers and precious metal exporters) rather than broad beta exposure.

Taking things private

An increasing trend we’ve noticed in 2025, and one we believe will persist in 2026, is the prominence of private debt investing when allocating to EMs.

So far, larger markets like China, India, Brazil and South Africa have been the focus of managers looking towards this type of exposure. Investment-grade countries in Latin America and Southeast Asia have also been on investors’ radar. Anecdotally, we haven’t seen much investment into lower-income countries where it is generally more challenging to find opportunities.

Innovation, innovation, innovation

One reason we believe private debt is a viable strategy for EM exposure is the capacity it offers for product innovation. By opting for private transactions, investors may be able to gain exposure to debt structures that offer the potential for attractive and uncorrelated returns, while supporting initiatives that have a real-world impact.

One such example is use-of-proceeds lending, which involves providing loans where the proceeds will be used in a defined way – for example, on an infrastructure or housing project. We have also observed the emergence of debt conversions as a way of allowing EMs to refinance their debt while supporting sustainability efforts.

These transactions – which are also referred to as ‘debt conversions for nature’ are investment grade and allow EM sovereigns to refinance their debt at improved financial terms. The caveat is that the borrower commits to utilising the proceeds from these savings in conservation efforts.

We believe other public goods can be used in debt conversions – notably, health, education, food among others.

We are also interested in the “A/B” loan programmes carried out by multilateral development banks (MDBs). Effectively these involve MDB’s lending money via their commercial arms to corporates / financial institutions / infrastructure projects in emerging markets while selling the risk to investors. This provides investors with exposure to EM and the underlying transaction while seeking to benefit from the MDB’s preferred creditor status.

A last structure we believe worth keeping an eye on in 2026 is outcome bonds. As the name suggests, returns from these instruments is linked directly to the success of specific development projects. We think there could be a strong pipeline for this kind of model developing in emerging markets, with potential returns linked to things like conservation efforts.

Read our 2026 global outlook

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.