Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Domestic demand, demographics and datacentres: a bright outlook for EM equity

Emerging markets (EMs) stand to benefit from stronger growth dynamics than developed market (DM) peers, and a variety of index approaches provide easy access to this vibrant asset class.

Key takeaways

|

After a decade of under-allocation, global investors are showing signs of warming to EMs.

Increasing appetite was reflected in a record-breaking January for EM issuance notes of $150 billion and record monthly inflows into Eastern Europe, Middle East and Africa (EEMEA) equities of around $5bn.[1] However, while tactical allocations have increased, strategic allocations haven’t following a decade-long US dollar bull market.

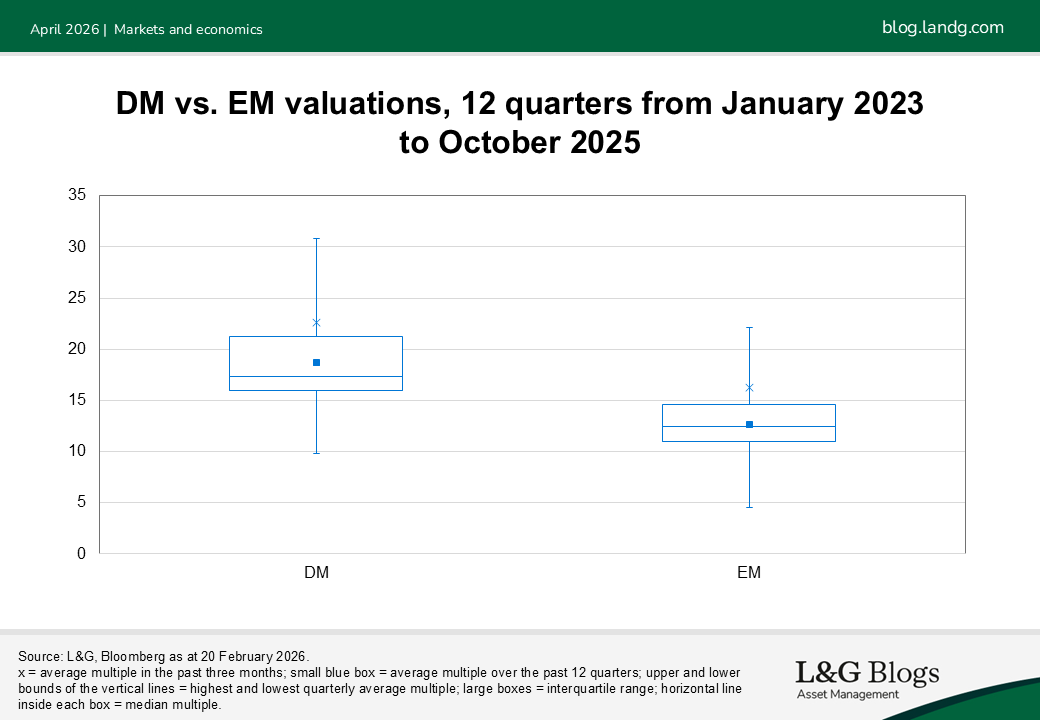

One contributor to recent inflows may be the cheaper valuations of EM equities compared with DMs. Valuations of the latter have expanded as a result of the large weighting towards the US.

EMs in a changing growth environment

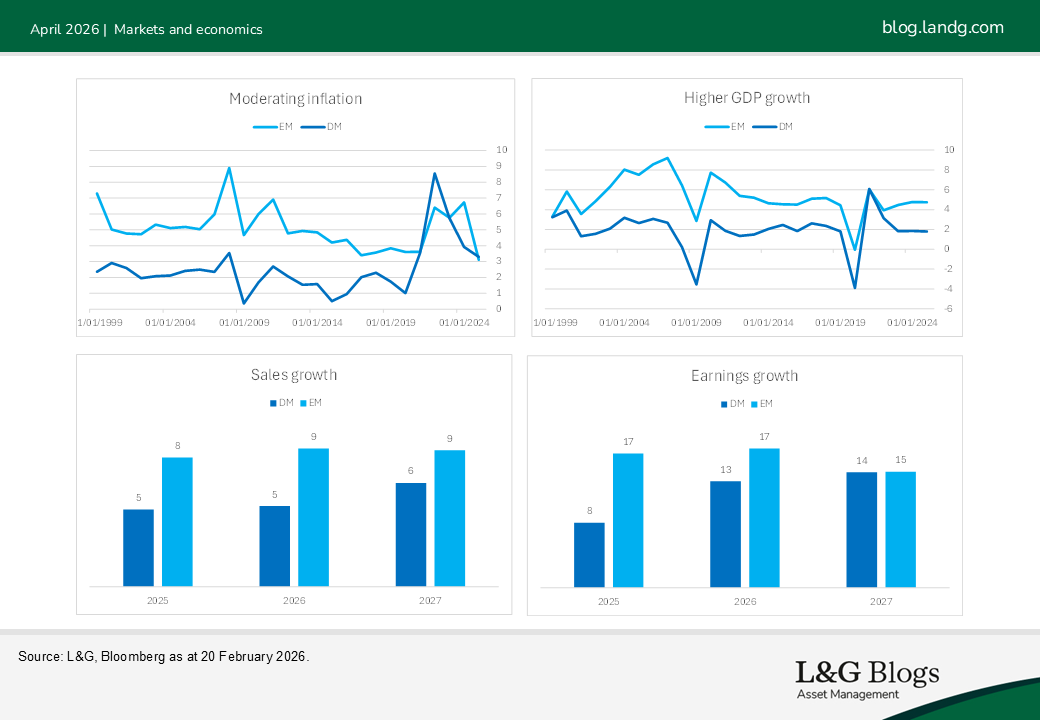

Against a backdrop of moderating inflation and a gradual slowdown in global growth, emerging economies continue to exhibit comparatively stronger growth dynamics than developed market peers.

This relative resilience reflects a combination of domestic demand, structural reform progress and, in some cases, more favourable demographic and productivity trends.

As a result, consensus expectations for sales and earnings growth in emerging markets remain higher than in developed markets going into 2026.

Metals as a driver of growth

AI adoption and the energy transition are now firmly under way and are inherently metal‑intensive. This dynamic directly benefits producing countries, and importantly, it reflects a global and structural trend rather than a short‑term cycle.

Demand is rising across a broad range of industrial and critical metals that underpin electrification, renewable energy infrastructure and datacentre build‑out.

Copper production is concentrated in countries such as Chile, the Democratic Republic of Congo (DRC) and Peru; aluminium in China; nickel in Indonesia and the Philippines; and tin across China, Indonesia, Peru, Brazil and the DRC. Precious and specialty metals also play a role, with silver production led by Mexico, China and Peru, and cobalt overwhelmingly sourced from the DRC.

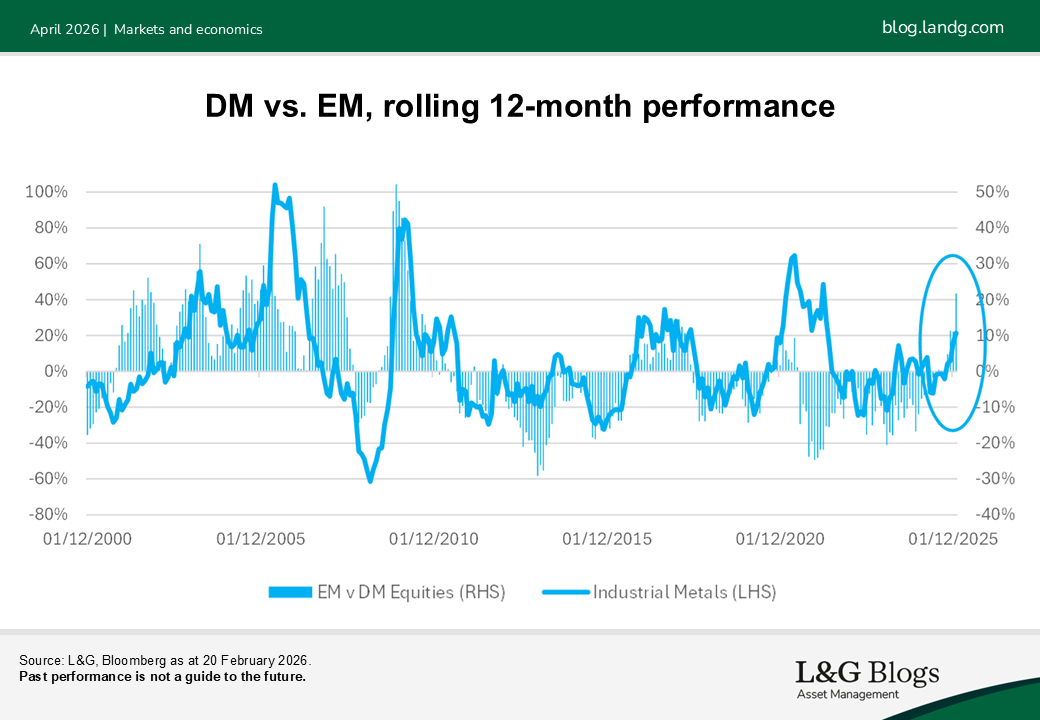

Together, this highlights how metal‑intensive growth themes increasingly channel economic and earnings benefits toward commodity‑producing EMs. The recent rally of EM Equities, which have significantly outperformed their DM counterparts in the last three months, has mirrored strong industrial metals performance.

Core exposure to EM equities

Index‑tracking funds and ETFs represent a simple and efficient building block within a broader asset allocation. By design, these vehicles aim to deliver close alignment with widely recognised EM equity benchmarks, resulting in low tracking error and a transparent return profile.

This makes them particularly suitable for investors who want to express a tactical view on EMs without introducing unnecessary complexity or unintended factor tilts.

In addition, index‑based solutions are typically cost‑effective, allowing investors to capture the long‑term return potential of EM equities while minimising fees, which is especially relevant in markets where volatility can already be higher than in developed regions.

EM equity exposure with an ESG overlay

Incorporating sustainability considerations can serve as a meaningful risk‑management tool. Compared with developed markets, EMs often display greater variability in governance standards, environmental practices and social frameworks, which can translate into higher idiosyncratic risk.

An ESG overlay can help mitigate some of these risks, either through targeted exclusions – such as removing companies with significant fossil fuel revenue exposure – or through ESG‑integrated weighting approaches that tilt portfolios towards more responsible issuers.

Over time, this can aim to improve the overall resilience of an EM equity allocation while still maintaining broad market exposure.

High‑quality dividend exposure within EM equities

Dividends can be viewed as a signal of financial strength and corporate maturity, because dividend‑paying companies are often further along in their life cycle, with stable cash flows that allow them to both reinvest for growth and return capital to shareholders.

In EMs, where dispersion in quality is particularly pronounced, combining a dividend focus with a quality overlay can be especially valuable. Screening out companies with weak profitability or unsustainable leverage helps reduce downside risk and supports a more robust income‑oriented EM equity allocation.

The availability of core EM equity building blocks, strategies that add an ESG overlay, and income-oriented approaches seeking dividend payouts means investors today have a wide variety of options.

[1] Source: Bank of America, January 2026.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.