Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Is China a currency manipulator?

The new US administration has threatened to label China a "currency manipulator". This label has little direct impact, but could be the trigger for a series of further protectionist steps such as tariffs and quotas. However, on the US government's own criteria, the accusation cannot be justified. If it happens, it would suggest that populist policymaking now rules the roost at the White House.

Donald Trump’s Contract with the American Voter outlined an action plan for his first day (and first 100 days) in office. Among the large number of pledges is one directly targeted at the bugbear of American protectionists: the Chinese renminbi.

The thinking behind the clamour is that by allegedly keeping their currency weak, the Chinese can keep the price of their goods artificially low on international markets, and unfairly undercut US competitors.

President Trump’s first day in office has been and gone, and the “currency manipulator” label has been notable by its absence. The threat was later downgraded further by Steve Mnuchin, Trump’s nominee for Treasury Secretary, when he offered the following masterclass in equivocation:

The direct consequences of the manipulator label are not exactly fearsome. The law simply requires the US Treasury Secretary to “initiate negotiations” with the offending country on “an expedited basis … to eliminate the unfair advantage”. Bill Clinton’s administration slapped the “manipulator” label on China five times between May 1992 and July 1994. There were no obvious consequences beyond a few stern conversations.

However, the political consequences are more unpredictable and potentially much more severe. Over recent years, there have been several Congressional proposals to impose tariffs. This theme was also picked up on the Presidential campaign trail:

Surprisingly, that was not a pledge of Donald John Trump in full protectionist flow, but the words of Hillary Rodham Clinton back in March 2016. If those types of policies were introduced, then it is only reasonable to assume that China would retaliate with tariffs of its own. The world could rapidly move to the type of destructive trade war last seen in the 1930s.

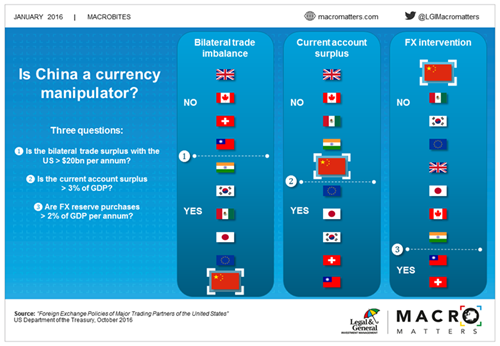

However, before rushing to punitive action, China critics would do well to consider whether any currency manipulation is actually taking place. The Trade Facilitation and Enforcement Act of 2015 outlines three criteria for a country to qualify as a currency manipulator:

- A large bilateral trade surplus with the US

- A sizeable current account surplus as a share of GDP

- Persistent one-sided intervention in the currency markets to keep the exchange rate weak

In recent years, the US Treasury department have clearly defined quantifiable cut-offs for whether countries fall foul of those criteria. The slide below evaluates the top ten trading partners of the US on all three scores. Countries below the cut-offs can coherently be accused of manipulating their currency; countries above the cut-offs cannot.

China’s current account surplus has shrunk considerably and now stands at just 2.4% of GDP. On that metric, China is only a currency manipulator if you are willing to apply the same label to the euro zone, Japan, South Korea, Switzerland and Taiwan.

However, the more important point is that China has definitely not been buying foreign assets to keep its currency weak. That music stopped in mid-2014. Since that time, Chinese has sold an eye-watering $1trillion of its reserves trying to keep its currency strong in the wake of capital outflows. That is the exact opposite of what it stands accused of by US politicians.

We may now live in a post-truth age in which exaggerations and misinformation are increasingly acceptable. Officially labelling China a currency manipulator despite the clear evidence to the contrary, would be the biggest “alternative fact” yet embraced by the new administration.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.