Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Chart of the month: Have reports of the dollar's death been greatly exaggerated?

In May 1897, rumours began to circulate in New York of the death of Mark Twain. The great writer, who was in London at the time, is reported to have sent a trans-Atlantic telegram with the simple message: “Reports of my death have been greatly exaggerated”. Could the same apply to the US dollar?

In 2025, it is not an American humourist but the American currency whose passing is the subject of feverish speculation. We hear about the “end of American exceptionalism”, the “threat of dedollarisation”, and the “demise of the dollar’s reserve currency status”.

President Trump’s tariffs make the United States a less predictable trading partner, Congress is threatening higher taxes on US assets held overseas, there are legitimate questions being raised about the durability of the US security umbrella, and all three major ratings agencies have now stripped the US of its AAA status. Is that enough to put the US dollar reserve currency status at risk and what would losing that status entail?

In the 1960s, Valery Giscard d’Estaing spoke of the “exorbitant privilege” of the US issuing the world’s reserve currency. Losing that privilege could entail higher debt financing costs and a weaker exchange rate. To understand how far that can go, we just need to look at sterling since the early 1900s. Prior to WW1, each pound was worth around $5 and sterling was the default currency of international trade and finance.

However, the upheavals of two world wars, the loss of empire and the growing economic heft of the US saw that status frittered away. Today, each pound is worth around $1.35. That’s a 75% fall in value over the course of just over a century. Could something similar happen to the US dollar?

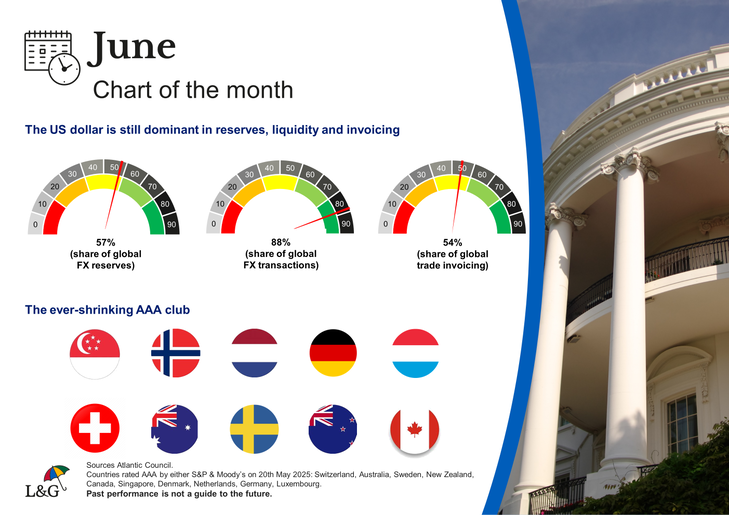

The US dollar remains dominant in global reserves, liquidity and trade invoicing. In the world of realpolitik, it’s also crucial that the US military spending is roughly comparable to the rest of the world combined. The dollar has been under pressure recently, with a 10% fall in the value of the US trade-weighted exchange rate since the start of the year. But that’s different from the end of the US dollar’s reserve currency status. The remaining AAA countries may be more creditworthy than the United States but, with the exception of Germany, they are all small markets. When it comes to picking a global reserve currency, there is little alternative (TINA) to the US dollar.

Putting the recent performance into context is also important. Despite a recent setbacks the US dollar is still 10% above its long-run inflation-adjusted average value against a broad basket of trading partners. This year’s drawdown is a stumble, not a death knell. We believe that reports of the dollar’s death have been greatly exaggerated.

Past performance is not a guide to the future.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.