Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Chart of the month: Oil prices – putting things in perspective

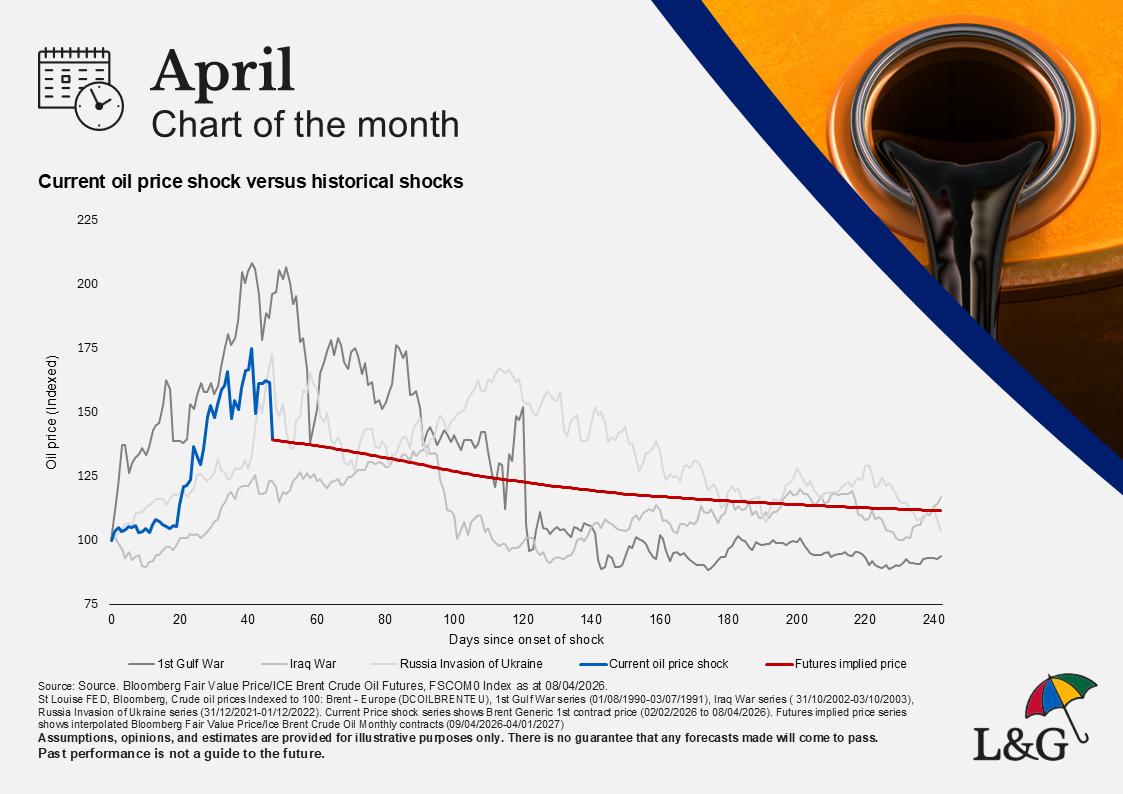

Investor attention remains firmly on the Strait of Hormuz and the timing of its reopening to Gulf energy exports. In April’s chart of the month, we place recent oil price movements in a historical perspective.

The current shock is only slightly less severe than that experienced during the first Gulf War of 1990/1991. Those longer in the tooth may recall that the spike in oil prices during this period contributed to the shallow, yet disruptive, US recession of the early 1990s.

However, today’s world is quite different from that of 35 years ago. Economic growth is now less energy-intensive, and the United States, once a major importer of fossil fuels, is currently the world's largest producer of both oil and natural gas.

Our chart also shows market expectations for oil prices for the rest of the year as implied by futures prices. Markets have been quick to reprice following the announcement of a two-week ceasefire between the US and Iran. Implied pricing now suggests that Brent oil prices will average in the low-to-mid-$80s per barrel range for 2026[1]. Although elevated compared to recent quarters, this is broadly commensurate with the 2023–2024 average.

The market reaction in the opening days of the conflict was fairly muted, with a consensus opinion that the US military operation and any associated disruption to energy supplies would last days or weeks rather than months. However, as the conflict dragged into its second month, some of the signposts to watch for that we had previously laid out came to pass, including damage to energy infrastructure.

These developments helped push market volatility higher and risk asset prices downwards. Against this backdrop and without a strong directional view on the future path of the conflict relative to consensus, we were weary of getting caught up in near-term investor panic. Therefore, we took the decision to upgrade our overall risk outlook towards the end of March, moving from negative to neutral through an increased allocation to equities.

Looking ahead, uncertainty persists, particularly regarding whether the agreed ceasefire will hold, if it will lead to a meaningful resumption of traffic through the Strait, and whether a more lasting settlement can be achieved before the ceasefire period concludes. In this environment, we prefer to maintain a neutral level of overall portfolio risk, keeping the flexibility to capitalise on market dislocations should they arise in the weeks and months to come.

[1] Source. Bloomberg Fair Value Price/ICE Brent Crude Oil Futures, FSCOM0 Index as at 8 April 2026.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.