Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Beyond the barrel

If the conflict in the Middle East persists, inflationary pressures could increase. However, in contrast to 2022, we think a sustained inflation surge appears less likely and the greater concern may be the potential drag on global growth.

Key takeaways:

|

Three weeks into the Middle East conflict and markets are starting to reassess earlier expectations about how quickly conditions may stabilise.

Oil prices have risen further following damage to energy infrastructure but the steep backwardation in energy futures indicates that markets currently anticipate short‑term disruption, with the potential for prices to ease if supply conditions normalise.

What if the shock proves more persistent?

While extremely hard to calibrate given the wide range of possible scenarios, we think there is around a one-in-three chance the world economy is heading for at least mild stagflation later this year.

The near shutdown of the Strait of Hormuz is a textbook negative supply shock. Oil and non‑US natural gas prices have risen in response.

In addition, the blockage of an interlocking web of commodity flows and refined products could disrupt agriculture yields via fertiliser shortages, raise transportation and packaging costs and impact a range of industries such as automotive (reliant on aluminium and rubber) and electronics (uses helium for cooling and sulfuric acid for cleaning). These effects will take time to appear, but will become more apparent if supplies fail to resume in the next few weeks.

Negative supply shocks can create challenges for central banks, as they raise both inflation and growth risks. Responding too forcefully to short‑term price pressures could weigh on employment and activity further ahead.

Templates from the past

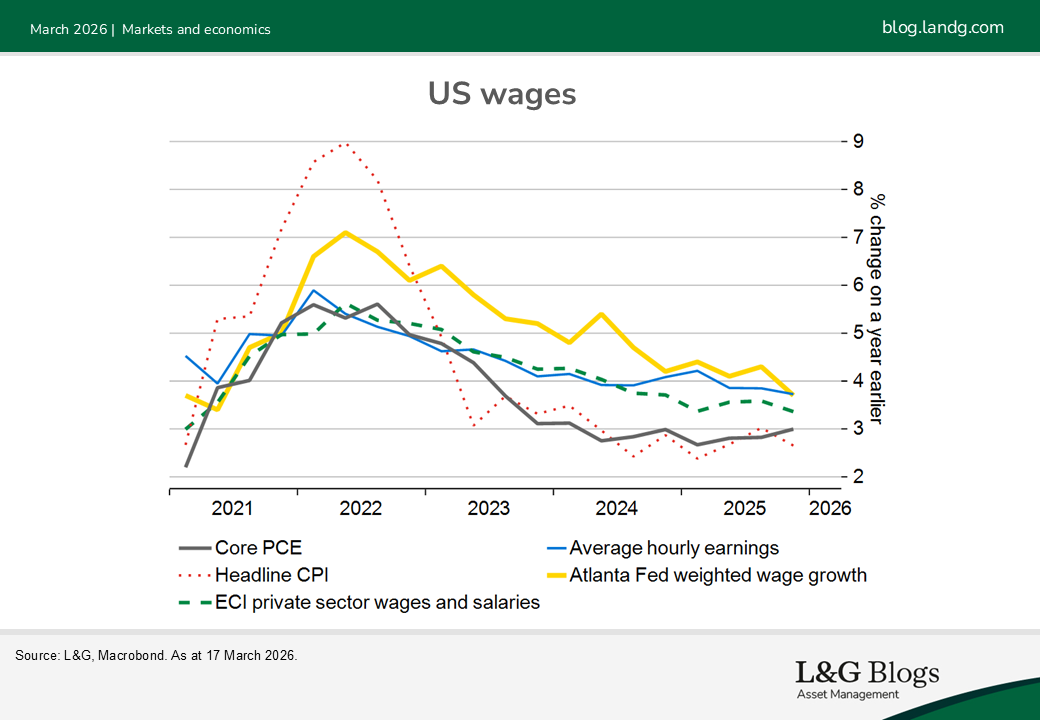

Financial markets tend to suffer from recency bias. The last time we witnessed a negative supply shock was in 2022 and this led to a major inflation outbreak. Wages quickly responded to higher headline inflation and companies then passed these cost increases into prices for broader goods and services. Could history repeat?

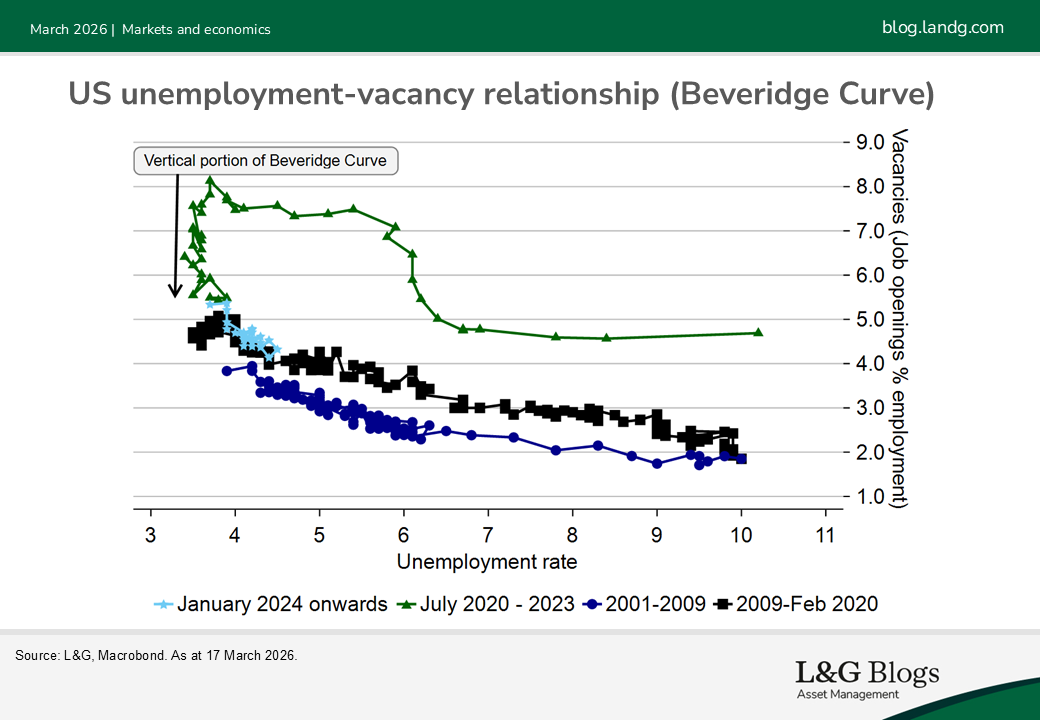

This time, after an initial bout of higher prices, we are less concerned about a more prolonged inflation outbreak. The critical difference in 2022 was surging demand alongside the supply shock. Inflation was already set to rise as pent-up spending from large-scale fiscal support and reopening post Covid combined with a scramble to find workers to meet this demand. This led to extremely tight labour markets. Unemployment had fallen as far as friction allowed. Instead, excess demand led to record job vacancies. Even as monetary policy was belatedly tightened to curb demand, unemployment remained low and wage pressures acute as the economy moved down the vertical portion of the Beveridge Curve.

Today, labour markets are far looser. While unemployment has edged up in the US and UK, this understates the change in conditions. Job openings have fallen back sharply and hiring has nearly stalled, in contrast to the nearly 400,000 a month US job gains seen during 2022. This means workers have far less bargaining power. It seems more likely the supply shock will squeeze real incomes without any corresponding increase in wages. This was the experience in 2011 when oil prices moved up $20-30 in the spring. Furthermore, any shortfall in demand is more likely to be met by rising unemployment rather than another sharp decline in job vacancies as the US is now on the flatter part of the Beveridge Curve.

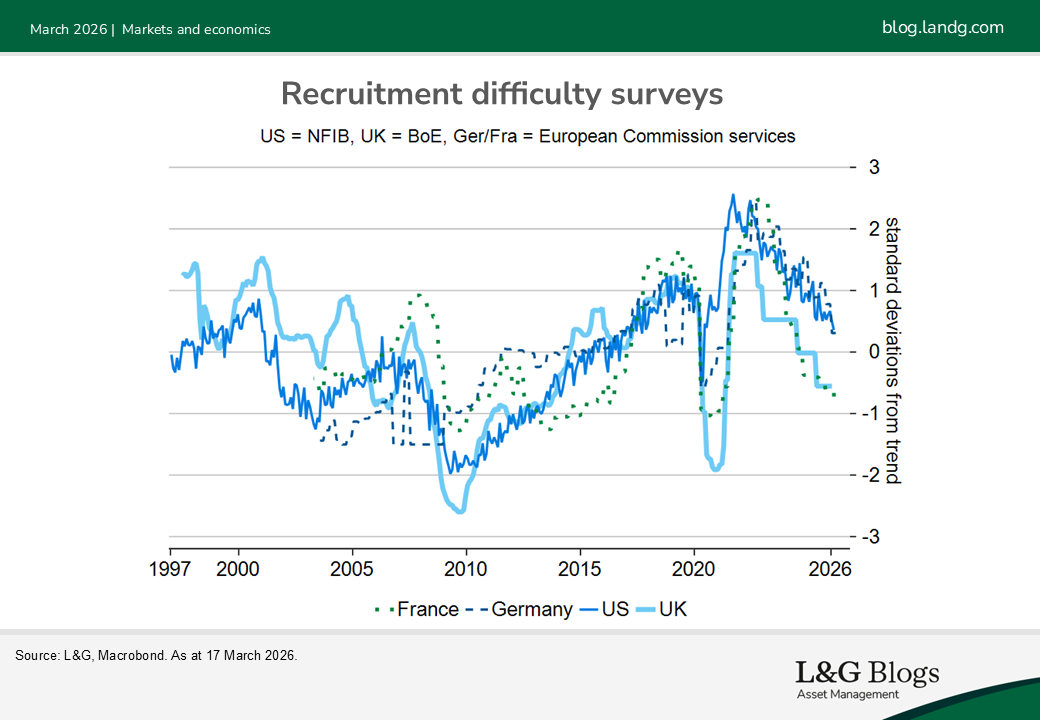

For a cross check for labour market tightness, we can observe surveys of recruitment difficulties. Companies are currently reporting relatively normal conditions across countries, in contrast to the extreme difficulty in finding staff in 2022.

Signposts

We will be watching both the responses of the consumer and the labour market closely. If consumers perceive the shock as temporary, they might be more inclined to run down saving and keep spending. Equally, businesses could also be prepared to hold onto staff if any demand shortfall is seen as short-lived. But the most critical variable is wages. It is not our expectation, but if these pick up in response to higher inflation, while supportive for consumer spending in the short run, these second-round effects would get the attention of central banks and make rate hikes more likely.

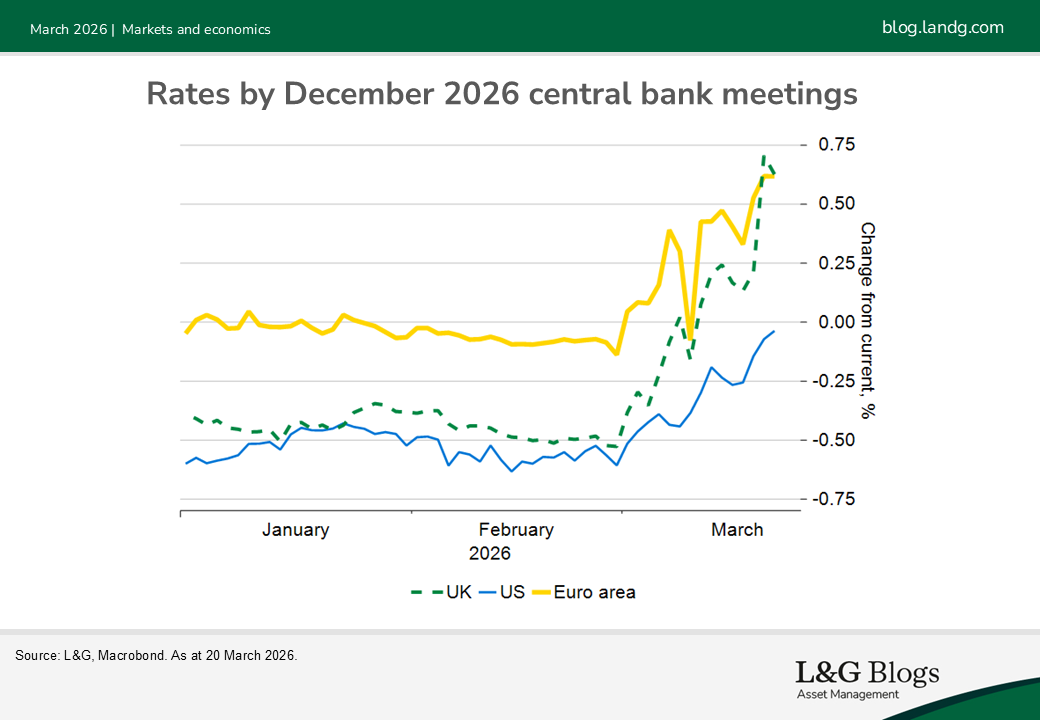

The US is more insulated from the shock given its abundance of natural gas and domestic oil production, but it is far from immune as gasoline, and especially diesel prices, are responding quickly to higher crude oil prices. The US will also suffer from weaker global demand. Given all the uncertainty, it makes sense for most central banks to wait and see. In the absence of evidence of rising wages, we would push back against attempts from markets to price in too many central bank hikes or a more pronounced divergence between European central banks and the Federal Reserve.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.