Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

What can investors learn from the Section 899 drama?

In the third instalment of our series on overcoming equity market concentration risk, we consider how investors can respond to shifting policy risk in US infrastructure and real estate assets.

One of the biggest risks facing investors today is the growing dominance of a small handful of names in public markets. We’ve seen it before: when leadership gets too narrow, the pain of a pullback becomes more acute. This time, it’s the so-called ‘Magnificent Seven’ carrying much of the load, and when one or two stumble, the whole market feels it.

That's where diversification* may help.

In our first blog, we covered regional diversification. In our second blog, we looked at the role of infrastructure and real estate. To recap briefly, we explained that returns from these assets aren’t tied to tech earnings or sentiment. Their cash flows aren’t driven by app downloads or advertising cycles. Instead, they are linked to real-world usage, often supported by long-term contracts, rent agreements, or regulated pricing mechanisms. In short, they move to a different rhythm.

In this blog, we consider an important consideration for investors in infrastructure and real estate: policy risk.

Section 899: a (brief) policy scare?

At the start of the year, the US administration unveiled ‘One Big Beautiful Bill’. Buried within this was Section 899, which caused a stir. The legislation has since been dropped, but we believe it’s still instructive for investors to consider the implications of this episode.

The proposed legislation singled out foreign owners of US assets in retaliation to tax policies some US policymakers feel are unfair.

For investors in infrastructure and real estate, the key concern was an increase in withholding tax on dividends. For example, the bill could have increased the amount of tax paid on US dividends to foreign owners by up to 20%[1], threatening to erode returns substantially.

But as of early July, that risk appears to be retreating. Section 899 has been dropped from the legislation, amid pushbacks from international partners and concerns over capital flight. It is a reminder that bold policy moves with geopolitical overtone can unravel quietly in the legislative weeds.

Yet investors shouldn’t be too quick to relax.

Think global

Even with Section 899 now shelved, the signal it sent remains important: US policymakers are becoming more assertive in using tax policy as a tool of strategic leverage. Therefore, foreign investors in US real assets will need to remain alert to similar risks that may emerge in future.

For investors, this underlines the benefits of regional diversification, as my colleagues Andrzej and Aude highlighted in the first part of this series. Non-US, domestic-focused assets such as infrastructure and real estate may benefit if investors move money away from the US to seek attractive opportunities.

At the same time, the US is not standing by. US infrastructure projects linked to national priorities and real estate tied to AI infrastructure are currently gaining attention. Albeit, not all assets are treated equally as foreign capital may find itself more welcome in some sectors than others.

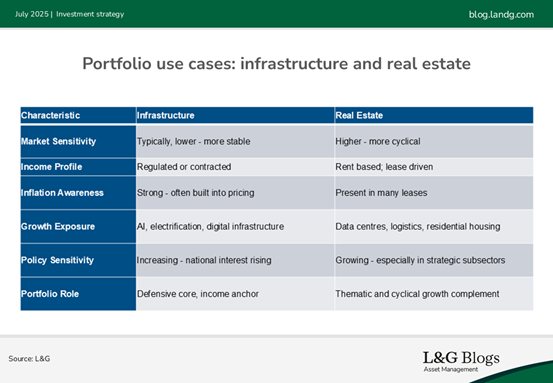

Different roles, shared purpose

It’s tempting to lump infrastructure and real estate together as ‘real assets’. But a more useful approach is to see their differences as complementary. With policy sensitivity in focus, the differing characteristics of these assets become particularly important to recognise.

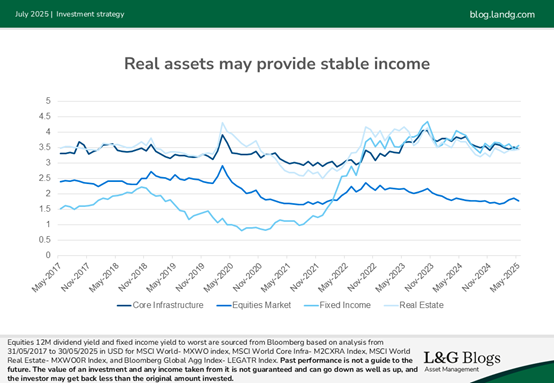

As shown in the chart below, real assets have historically provided a steady source of income, complementing core equity and fixed income positions.

In summary, we continue to see a strong strategic case for infrastructure and real estate, with recent equity market volatility only highlighting the potential benefits.

The brief flare-up around Section 899 may have subsided, but the episode underscores an important broader point: policy can move markets. The challenge for investors is what to do in such a market. We like to follow the mantra ‘prepare, don’t predict’. That means starting from a well-diversified asset allocation and using scenario analysis to assess risks, adjusting wherever those risks appear too large.

It is not about knowing what will happen, but being prepared for whatever does happen. And as this series of blogs illustrates, regionally diversified equities, infrastructure and real estate all have a role to play.

*It should be noted that diversification is no guarantee against a loss in a declining market.

[1] As per the House version of the bill. The Senate has proposed a 15% limit, and changes are ongoing.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.