Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Surplus extraction is here: What should DB schemes do now?

The government is making it easier for well-funded DB schemes to release surplus, when ‘safe to do so’, and trustees will need to set out their proposed approach to surplus extraction as part of their statement of strategy. As we weigh up this crucial issue of ‘safety’, let’s look to the insurance market to consider how DB schemes might run on and extract surplus for now, while preparing to pivot to buyout if needed.

What has been announced so far?

The government has set out its intention to amend the rules on surplus extraction, “to allow trustees of well-funded DB schemes to release money back to employers and their scheme members, when ‘safe to do so’, unlocking some of the £160 billion surplus funds to be reinvested across the UK economy and boost business productivity and deliver for members". Following consultation, it will bring forward legislative changes as part of the Pension Schemes Bill 2025, including regulations that will specify the minimum funding level at which surplus can be extracted, currently expected to be full funding on a low-dependency basis.

The Pension Regulator (TPR) has issued guidance on new models and options in DB schemes to help trustees and employers to assess the range of new endgame models and options available across governance, financial and insurance. Once legislation is enacted, TPR will consult and publish further guidance on releasing surplus.

With approximately three in four schemes in surplus on a low-dependency basis, endgame planning and whether to choose buyout, run-on or both will be a key question for DB schemes.

DB schemes: Have a plan for endgame and for surplus

TPR has issued a call to action that ‘Schemes should have documented policies regarding their long-term objectives and endgame options, including surplus’.

A key consideration for trustees considering surplus release will be this question of safety, balancing multiple objectives to:

- Manage scheme assets to pay pensions and remain fully funded on a low-dependency basis

- Improve security for members and prepare for contingent events

- Release surplus under a framework agreement with the sponsor to, for example, enhance member benefits, make payments to a DC scheme or make payments to the employer

When is it ‘safe to do so’? Learn from the insurance industry

The history of pension scheme legislation protecting against releasing surplus will no doubt be on the mind of many trustees. Just like a beekeeper extracting honey from a hive, the concept of safety is therefore hugely important. Insurers paying benefits until all liabilities have been discharged have similar objectives to DB schemes that are running on – what can we learn from the prudent capital framework that underpins the financial security of the insurance regime?

1. Manage scheme assets ‘like an insurer’?

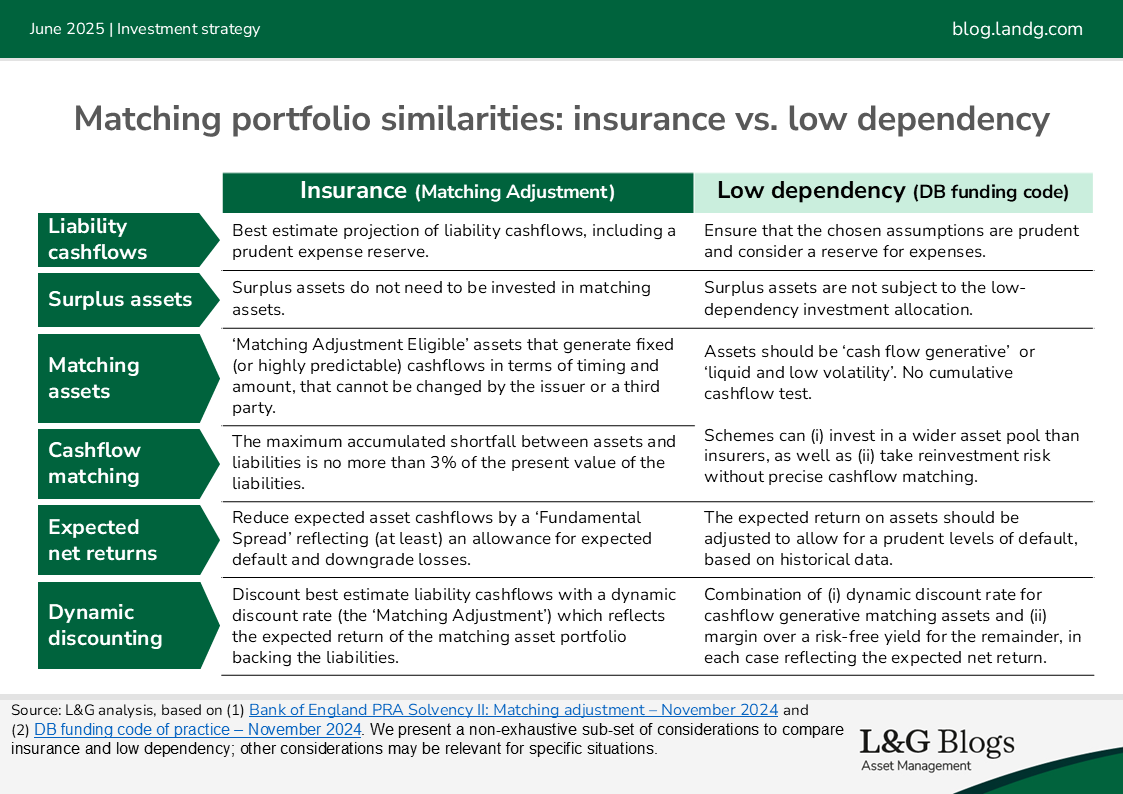

TPR’s DB Funding Code of Practice requires DB schemes to determine a funding and investment strategy to provide benefits over the long term, so that when the scheme is fully funded on a low-dependency basis and invested in the low-dependency investment allocation, no further employer contributions would be expected to be required.

This framework has many similarities with the ‘Matching Adjustment (MA)’ framework for insurers, set out in the table below, suggesting that well-funded DB schemes in run on may consider ‘investing like an insurer’, but with more flexibility:

Potential actions include:

- Update liability basis: refresh assumptions for a low-dependency basis, including an expense reserve, reviewing prudence and deploying a dynamic discount rate that is sensitive to credit spreads

- Create a low-dependency matching portfolio: invest cashflow-generative or liquid and low-volatility assets to pay pensions, manage risks, and generate surplus against the low-dependency basis:

- Consider a cashflow-aware approach that includes cashflow matching as well as investing in short-dated credit with reinvestment risk (see Endgame portfolios: making the most of CDI and Playing the 'weighting game')

- Consider public and private-credit-based assets and their potential transferability to an insurer (or if they are not transferable, understanding their investment horizon and liquidity terms – see Illiquidity innovation)

2. Improve security for members by planning for contingencies?

Both pension and insurance frameworks include provisions to address contingent events, such as short-term adverse changes in market conditions or longevity (beyond the assumptions made in the low-dependency framework) or a deterioration in the employer covenant, potentially requiring a new course of action.

Potential actions include:

- Stress test assets: adapt investment guidelines to constrain the low-dependency investment strategy within an acceptable level of risk, for example a 1-year, 1-in-6 Var measure

- Create a surplus / growth buffer portfolio: surplus assets in excess of the low-dependency funding level do not have to be invested in accordance with the low-dependency investment allocation:

- Consider a three pot approach so that some of the surplus could be a risk buffer against adverse experience of the matching portfolio versus liabilities, with the rest invested in short- or long-term growth (see Running on into retirement?)

- Put a plan in place to move surplus assets between the matching and surplus portfolios to maintain the low-dependency funding level

3. Release surplus by agreeing an extraction policy?

In our earlier blog we considered the key question of how to set the extraction level, considering intergenerational fairness, the variability of buyout pricing versus a low-dependency basis, and the rise of contingent assets.

So what’s new? TPR’s guidance states ‘If you decide that you wish to extract surplus, the level at which you consider that surplus can be extracted is a matter for you as a trustee to decide. Current legislation only allows surplus release in relation to buyout funding levels. Any changes to this basis will be set out in future legislation.

Subject to this, in situations in which the scheme is likely to remain fully funded on a low-dependency basis and there is no realistic risk of employer insolvency, it is unlikely that TPR would have reservations about the release, subject to you having considered any other relevant matter related to the circumstances of the scheme and the sponsoring employer.’

By contrast, in the insurance regime, the minimum funding level for extracting profit is the total of their technical provisions, the risk margin and the solvency capital charge. However, many insurers will also hold excess ‘own funds’ above this amount and maintain a higher solvency capital coverage ratio than 100% before releasing profit. For example, Legal & General Group’s Solvency II coverage ratio on a regulatory basis was 232% as at 31 December 2024.

A potential action:

- Scenario analysis: Before setting an extraction policy (and subject to future legislation), trustees may wish to carry out scenario analysis and/or stress testing to better understand the range of possible future outcomes following surplus release, taking account funding level projections as well as future covenant strength projections. Trustees will need to balance a trade-off between surplus extraction (the opportunity to share surplus with current members) versus benefit security (safeguarding benefits for future pensioners), see our blog: Unlocking surplus in the endgame.

Prepare for surplus now, put a plan in place for the future

While we await further legislation to clarify opportunities around surplus extraction, in particular around ensuring that it is ‘safe to do so’, trustees can start to plan now, and prepare to ‘invest like an insurer’ to preserve their low-dependency funding level and seek to grow a surplus, while retaining flexibility to pivot to insurance if you want to or need to in the future.

If you’ve enjoyed this content, we’d like to highlight that you can find all our latest content for DB schemes in one place at our designated DB blog page.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.