Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Private markets are now a core part of strategic conversations in UK defined contribution (DC) investing. Investors increasingly acknowledge the long‑term return potential available in private credit, infrastructure, real estate and other illiquid assets. But one technical feature shapes how these assets behave when introduced into daily‑dealt DC arrangements: the J‑curve.

It’s a familiar concept for private market specialists, yet its implications are less often explored through a DC lens.

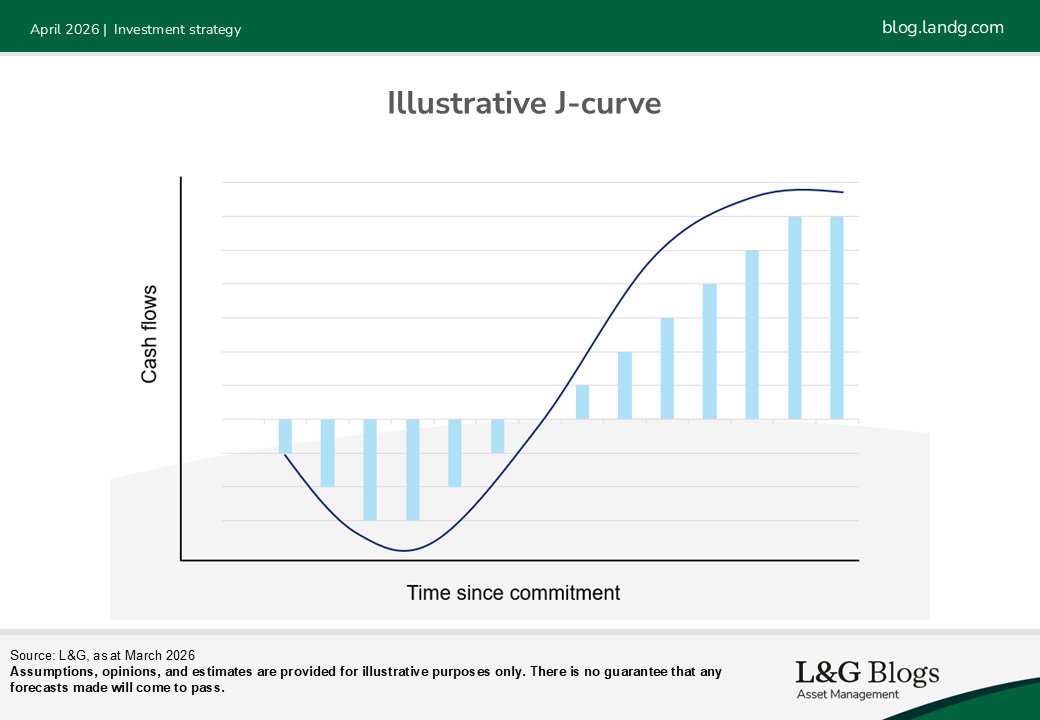

What the J‑curve represents

In private markets, capital is drawn down slowly, some of the fees and expenses are front‑loaded, deals take time to close, and underlying assets may be held at cost before valuations start to move. As a result, capital deployment is often slow and the performance profile typically dips before rising as projects mature and begin to distribute income or generate realised gains.

For a closed‑ended institutional investor – comfortable with multi‑year deployment and infrequent valuations – that pattern is expected. For a daily‑priced DC arrangement, it raises operational, governance and fairness questions.

Daily dealing requires all members to trade in and out at a fair price. But private market assets don’t deploy evenly or revalue instantly. If unmanaged, the natural J‑curve could disadvantage members who happen to be invested during the initial build‑out phase. These members only see a slow build-up of the private market exposure while bearing a disproportionate share of the early negative returns.

Why this matters specifically in DC

Two issues sit at the heart of the problem.

1. Slow deployment and the impact on cohorts

Private market strategies deploy capital gradually, sometimes over several years. In a DC environment, where members join, leave, and derisk continuously, this creates uneven exposure. Early cohorts may sit on largely undeployed capital for long periods, and if they switch strategy or transfer out before the portfolio is fully built, they may never experience the return‑generating phase.

For trustees and employers, this isn’t just an investment point. It is a fairness and communication issue. Advisers often ask: “How do we ensure that no cohort is disadvantaged by the timing of their contributions?” Without a considered approach, timing risk is real.

2. Early performance drag and daily pricing

Setup costs for private market investments, such as legal, structuring and due‑diligence fees are inevitably front‑loaded. In addition, valuation lags mean the early portfolio may not reflect the underlying economic progress of assets still at the development stage.

In a daily‑priced fund, these mechanistic steps of private market investing must not translate into a visible mark‑to‑market loss. A DC default cannot rely on members accepting multi‑year negative performance as ‘part of the journey’. Schemes need mechanisms to avoid penalising early investors.

DC design to reduce the dip

Rather than simply accepting the J‑curve as unavoidable, several design features now help schemes to build private market exposure without creating a fairness problem.

1. Blending vintages to smooth the return profile

Rather than starting exclusively with newly originated assets, DC solutions can combine different stages of the private market lifecycle:

- New early‑stage commitments (at the start of the J‑curve)

- Seasoned, income‑producing assets (beyond the dip)

This blend gives members representative exposure across the full lifecycle of a private market investment and meaningful exposure from day one. It also helps trustees to evidence that value for money has been considered not just at the strategy level but across membership cohorts.

For example, a scheme may hold mature infrastructure equity generating stable cash yields alongside newer commitments development projects in real estate or renewables. The result is a more stable aggregated performance line, even while new assets are being built.

2. Using evergreen structures to solve deployment delays

Evergreen vehicles, or open‑ended private market structures, allow faster capital deployment and avoid the multi‑year build-up associated with closed‑ended strategies. They give DC members immediate access to a diversified pool of underlying assets, helping schemes avoid the stop‑start pattern that can arise when relying exclusively on closed‑ended vintages.

More specialist or opportunistic exposures can then be layered in gradually once the core allocation is established. This sequencing helps avoid situations where early cohorts face large cash balances waiting to be invested.

3. Ensuring operational alignment with daily pricing

The technical work behind daily pricing is often underestimated. To incorporate private markets effectively, schemes need processes that allow:

- Timely flow‑through of underlying valuations

- Clear methodologies for allocating costs – particularly early, one‑off expenses

- A pricing model that can support private asset characteristics without introducing noise or arbitrage risk

4. Scale that can level the curve

Once a DC private market allocation reaches scale, the investment approach can become more granular. Schemes gain the capacity to introduce more specific exposures, such as co‑investments or sector‑focused strategies, without creating distortions in pricing or liquidity.

Mature programmes can also rely more on an ongoing ladder of commitments rather than depending heavily on evergreen structures. This naturally dampens the J‑curve over time and improves diversification* across economic cycles.

The J‑curve isn’t a flaw in private markets – it’s simply how illiquid assets behave. The challenge in DC is ensuring that this behaviour doesn’t unfairly advantage or disadvantage particular cohorts.

While many schemes are still considering how to overcome the J-curve, our early-mover advantage means we are already well into the journey, with capital deployed and exposure being delivered.

The direction of travel is clear: private markets will continue to feature more prominently in DC defaults. How schemes manage the J‑curve will determine whether that exposure delivers what members need – consistently, and fairly. Find out more about the private markets solutions we offer DC clients and their members here.

If you found this article interesting, you can find our latest content on DC pensions and investments on our designated DC blog page.

*It should be noted that diversification is no guarantee against a loss in a declining market.

Key risks

Past performance is not a guide to the future. The value of an investment and any income taken from it is not guaranteed and can go down as well as up, and the investor may get back less than the original amount invested.

Risk management cannot fully eliminate the risk of investment loss.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

The above information does not constitute advice.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.