Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Investing for run-on

Surplus generation and extraction or benefit enhancement provide an additional layer of complexity, but is this really a new concept?

The following article is an extract from our latest DB outlook.

When considering the recent industry discussions around ‘run-on’, many trustees may wonder what all the fuss is about. After all, most pension schemes have ‘run on’ for several decades, often while maintaining a surplus on their technical provisions basis – is there really anything new to consider here?

A sceptic’s view

Of course, the fundamentals of pension scheme investment haven’t really changed – pension schemes are still long-term investors who must meet liabilities. Surplus generation and benefit enhancement or payment to the sponsor can in some sense just be considered a form of future liability accrual, and pension schemes have dealt with this for decades. The exact form of the new liabilities accrued will depend on how trustees and sponsors plan to use the surplus, and these new liabilities would have increasingly shorter duration and be contingent upon favourable investment returns, but the concept remains broadly similar.

So pension schemes will still need to agree their strategy, define their risk tolerance, and then invest in an efficient portfolio which they believe will generate the highest return while staying within that tolerance. They will still need to diversify rewarded risks, seek to protect against unrewarded risks, and carefully manage liquidity.

And as ever, there will be many different views on what the most ‘efficient’ portfolio looks like. While there is general consensus these days that it can make sense to hedge interest rate and inflation risk using bonds, views on the best way to target additional returns can be much more varied. Some will argue that credit has a special place in liability-matching portfolios, while others will make the case for less liquid assets delivering income in a more flexible manner. Alpha generation and absolute return strategies will have their proponents of course, while recent equity market performance may lead others to conclude that traditional growth assets still offer the best long-term value. So who’s right?

Lessons from life insurers

Before getting lost in the detail of these well-tested arguments, sometimes it’s helpful to take a step back and think about the problem from another perspective. Life insurers are the ultimate long-term, low-risk, liability-aware, run-on investors – so what do they do, and why? Sure, they operate under a different regulatory framework, which influences their behaviour to a degree, but that framework is different for a reason. Without recourse to a ‘sponsor’ who can provide deficit payments when needed, and with an ongoing requirement to pay out significant cashflows to meet liabilities each year, they are more vulnerable to short-term changes in their funding position. To seek to avoid the risk of a downwards spiral following a market drawdown, full cashflow matching takes centre stage, alongside an additional capital risk buffer. So could pension schemes follow the same approach? And should they? Or does the pensions regulatory regime provide them with a competitive advantage and greater flexibility?

The ‘best of both worlds’

Full cashflow matching has undoubted appeal where possible, but it may be challenging for some pension schemes to achieve. And with spreads currently very tight, do liquid cashflow-matching assets provide enough return? Life insurers can access higher yields while still achieving a true cashflow match by investing in long-term illiquid assets such as private credit, but this may not work for pension schemes who still have an eye on a longer-term buyout.

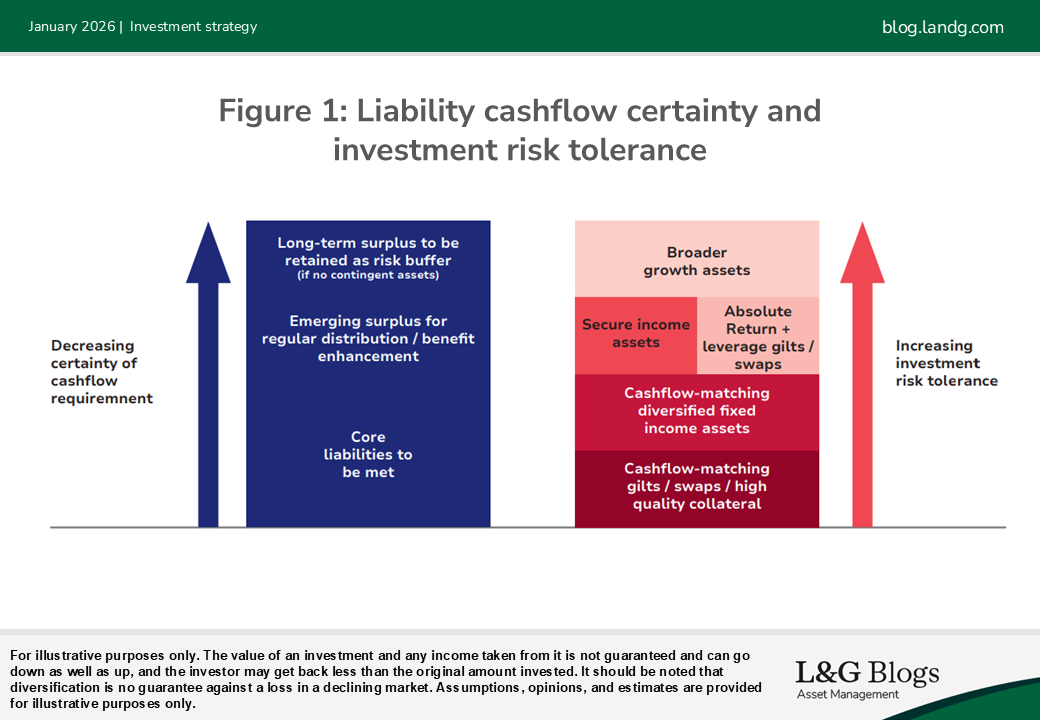

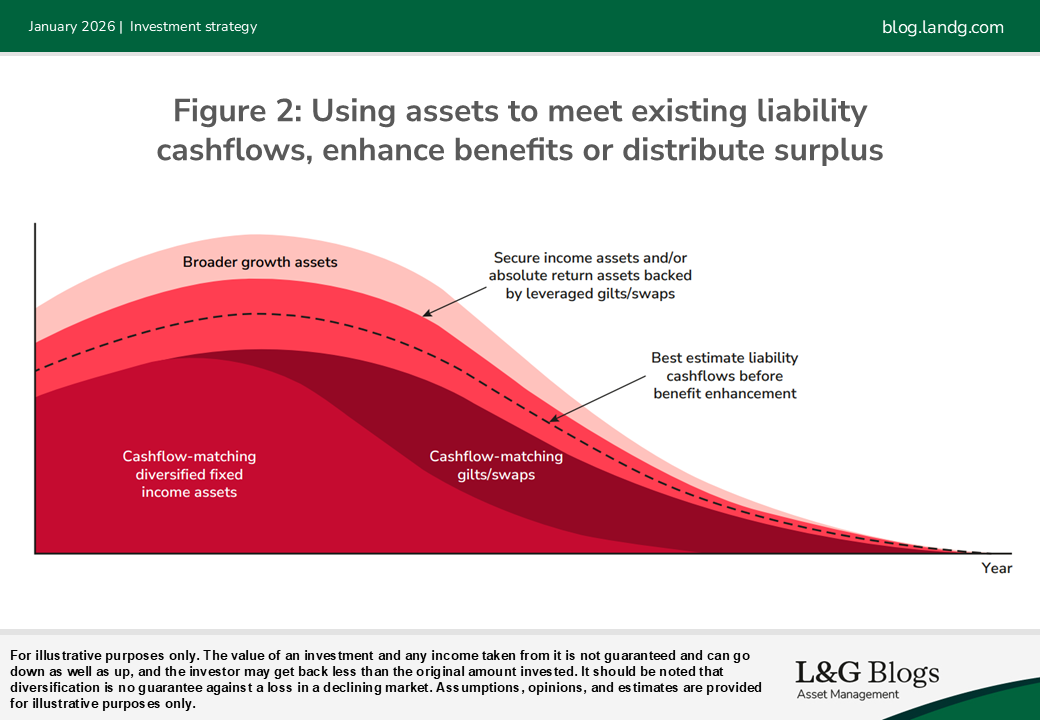

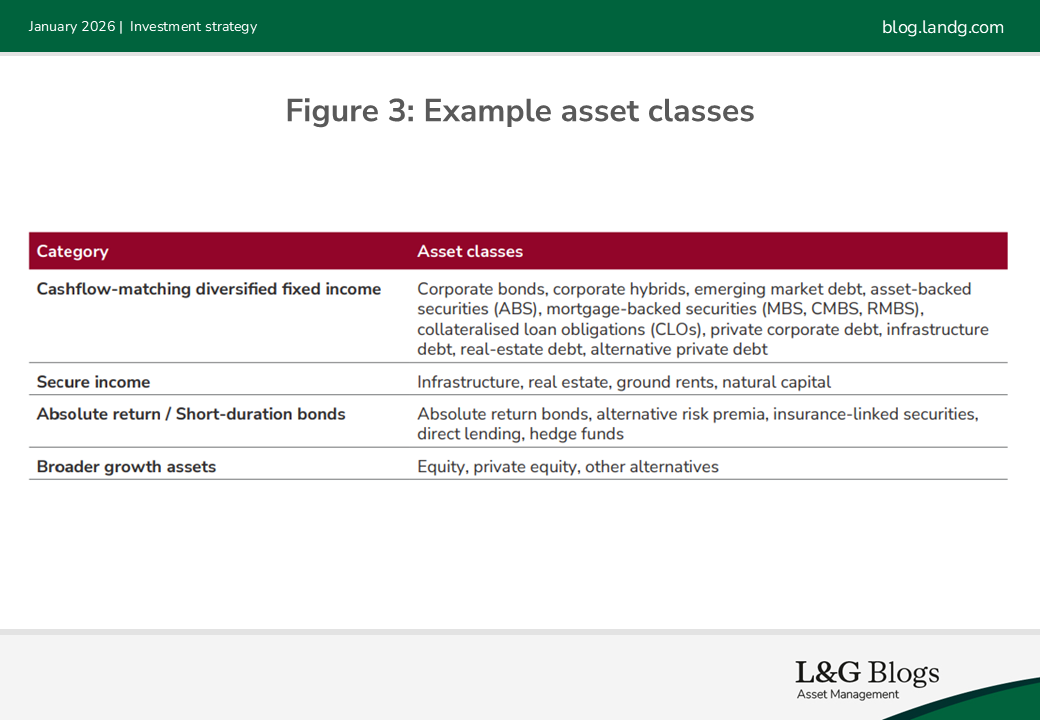

Luckily there are a number of other levers that pension investors can pull to target returns within a cashflow-aware framework. A broad range of alternative credit assets such as emerging market debt and various forms of securitised debt can be incorporated into a cashflow-matching mandate alongside sovereign and corporate bonds. For schemes that can tolerate some illiquidity, this can be supplemented by additional exposure to various forms of cashflow-matching private credit. Further relaxing the requirement for perfect cashflow matching also opens the door to a broader range of ‘secure income’ assets such as infrastructure, real estate and natural capital. And absolute return or short-duration bond assets can also be incorporated in conjunction with swaps or leveraged gilts, effectively generating hybrid matching/growth exposure.

Some schemes and sponsors may use contingent asset vehicles to provide a risk buffer, or else place more implicit reliance on the sponsor covenant over the long term. But where additional surplus is held in the scheme, a larger surplus cushion provides additional risk tolerance, facilitating potential allocations to assets with greater exposure to the market cycle, such as public and private equity, or lower quality credit or alternative assets. So will a long-term run-on portfolio look very different to what pension schemes have seen before? Different tolerances for illiquidity, ability to achieve a true cashflow match, and investment beliefs will mean that there is no ‘one-size-fits-all’ answer. Certainly some of the asset classes will look familiar, but trustees’ investment frameworks will need to be refined, risk models made more robust, and investment considered through the lens of cashflow certainty.

The above article is an extract from our latest DB outlook.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.