Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Demystifying private credit ratings

Private credit’s been in the headlines of late. In this blog, we address some of the misconceptions about how the asset class is rated.

The bankruptcy of First Brands*, a little-known Ohio-based auto parts retailer, recently propelled private credit into the spotlight despite the asset class having a modest exposure to the company. It has also drawn attention to the unglamorous (but important) subject of credit ratings.

In recent weeks much has been written about the validity of private credit ratings with musings on the capability of the credit rating agencies, particularly those outside the “Big Three” (that’s S&P, Moody’s and Fitch*).

We therefore thought it was timely to provide some insight into how we navigate the complexities of private credit ratings.

Not all private credit is the same

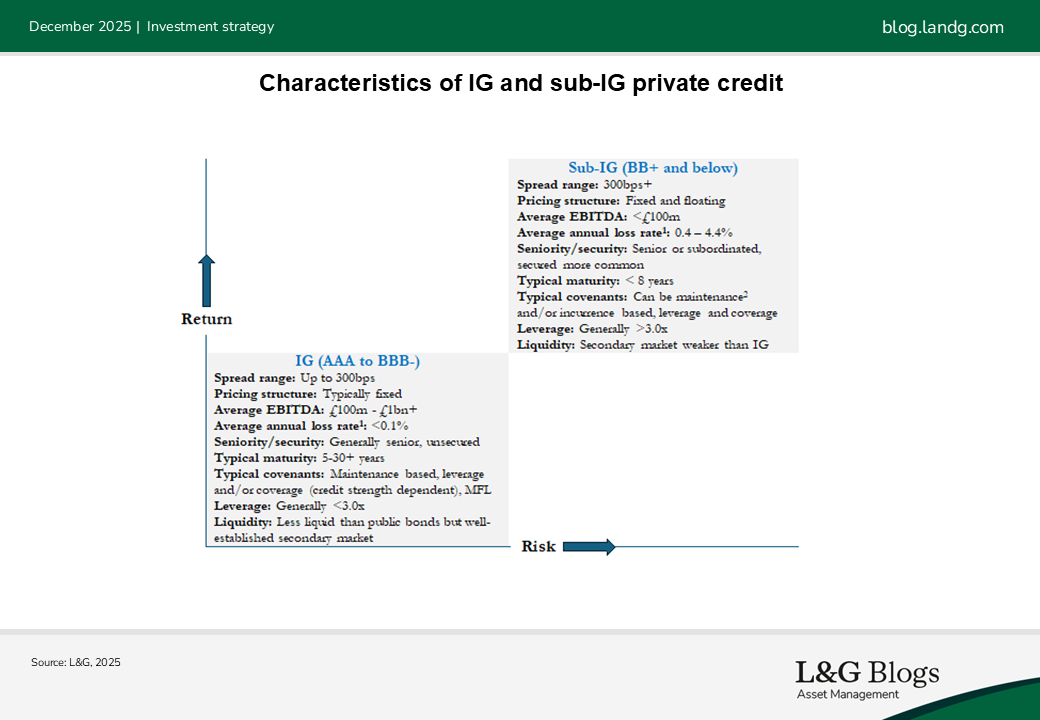

When people use the term ‘private credit’, they often mean the sub-investment grade (sub-IG) part of the market, which is dominated by direct lending. This segment grew rapidly in the aftermath of the global financial crisis. Investment-grade (IG) private credit, in comparison, is less spoken about. We have previously written extensively about this asset class which has a track record over several decades. In terms of market size IG and sub-IG private credit are roughly the same at around $1.5tn-$2tn each based on our estimates.

Below we have used characteristics of corporate private credit to highlight the typical differences between IG and sub-IG. However, it should be noted that a large part of the IG private debt market is also asset-backed, including, for example, Real Estate Debt, Infrastructure Debt and other structured or alternative finance.

It is key to point out there is a significant variety of risk profiles available in sub-IG credit, with big differences between BB vs. single B and below.

BB borrowers sit at the upper end of the sub-IG spectrum and exhibit stronger fundamentals, typically with lower leverage, more predictable cashflows and greater scale. Despite this, lenders still typically benefit from robust covenant packages and other protections. Many investors focus on either firmly IG or single B credit profiles. As such, despite its attractive risk-return profile, BB credit is often under-served by institutional capital – we refer to it as the “forgotten middle”. While this market has historically been well served by bank lenders, capital and returns considerations for banks often mean issuers in this segment have a desire to diversify their funding sources.

Private credit ratings are not new

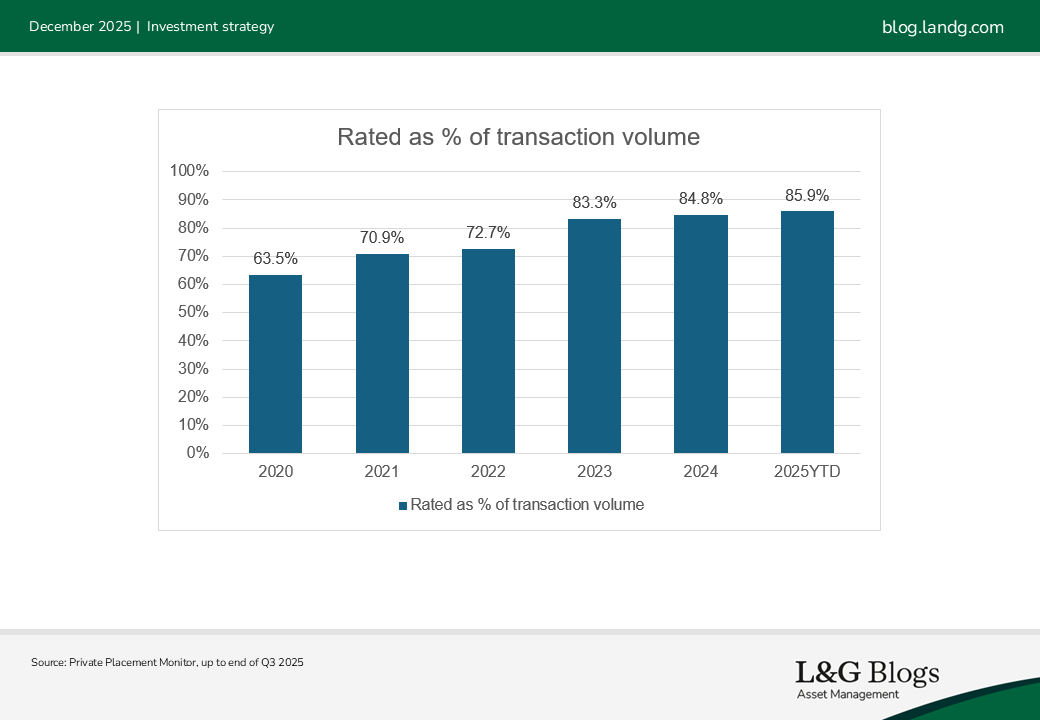

Insurers are a big investor in IG private credit due to the high credit quality and liability-matching characteristics. They also commonly require formal credit ratings for capital requirement purposes. This can be sourced from an external credit rating agency (referred to as an ECAI[1] in Europe and NRSRO in the US) or from an internal ratings team. In 2024, c.85% of US private placements volume, which is a large part of the IG private credit market, had at least one external credit rating. Where the borrower has also issued debt in the public market, which is more common for IG than sub-IG, there will typically be a public credit rating available for the borrowing entity.

Sub-IG private credit assets tend to be more bespoke, bilateral arrangements issued by smaller companies. It is less likely these companies would also issue in the public market and have a publicly available external rating. Some issuers will obtain a private rating from an ECAI, but these are also less common in the sub-IG space, so lenders will often rely on their own internal rating assessments.

Sub-IG private credit is less popular with insurers, given the penal capital charges associated with assets with lower credit ratings. Institutional investors such as pension schemes and endowments are the major allocators. Unlike insurers, they are not subject to regulatory requirements, although they are increasingly asking managers to provide credit rating data for portfolio monitoring and risk management purposes.

How credit ratings are assigned: Public vs. private

The methodologies and processes followed by ECAIs to assign credit ratings remain the same whether the rating is public or private, the only difference lies in how the rating is disseminated:

· Publicly available credit ratings are freely accessible to all and published on the agencies’ websites without paywalls

· Private credit ratings, on the other hand, are shared exclusively with a pre-selected group of investors, as permitted by the issuing entity and the relevant rating agency

Unrated or non-recognised ratings

When a debt investment is either unrated or only rated by an external agency not recognised under the clients’ investment management agreements, in most cases L&G’s independent credit ratings team steps in to provide one. For internal ratings, the team uses proprietary rating methodologies and procedures designed to align broadly with ECAIs, to ensure consistency and avoid systemic bias. Most of the team have previously held roles at one of the major rating agencies.

Transparency is key

As we established earlier in this blog, there are two distinct parts of the private credit market, IG and sub-IG, which have very different characteristics. Private credit ratings are not new for either part of the market. Publicly available ratings are more prevalent in IG, but less seen in sub-IG, where internal credit assessments and private ratings from ECAIs are more common. Private credit ratings thus play a vital role in supporting investor confidence and risk management. We believe transparency is fundamental to the credibility and effectiveness of the ratings. As private credit continues to grow and becomes more complex, robust and transparent rating practices remain essential for making informed investment decisions.

*For illustrative purposes only. The above information does not constitute a recommendation to buy or sell any security.

[1] ECAI stands for External Credit Assessment Institution. NRSRO stands for Nationally Recognised Statistical Rating Organisation. They refer to an organization that provides credit ratings for entities such as corporations, governments, or financial instruments. The most well-known agencies are S&P, Fitch and Moody’s.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.