Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Building resilient portfolios in an uncertain world

Why we seek to shun reckless prudence in favour of clearly reasoned strategic allocations.

The following is an excerpt from our 2026 global outlook

In a twist on the author Leo Tolstoy’s famous adage, we’d argue that “all bullish investors are alike, but all bearish investors are bearish in their own way”. Investment managers can always point out reasons to worry, but the nature of the concern shifts over time.

The regular survey by Bank of America of fund managers is a good reflection of the zeitgeist.

With 2026 nearly upon us, the following are top of the list: AI valuation concerns, nebulous fears about private credit and the perennial angst about the inflation outlook. Geopolitics is also never far from investors’ thoughts, given the simmering tensions.

Known unknowns

A number of these drivers are better characterised as existential uncertainty rather than risk. Risk refers to situations where the probabilities of outcomes are known or can be measured; uncertainty describes scenarios where these probabilities are unknown or difficult to estimate. Uncertainty is fundamentally less quantifiable and more challenging for investors to manage.

The only way to avoid all such worries is to take shelter in cash, but that is not a recipe for either liability- or inflation-beating returns. In fact, it is compensation for taking exposure to these unquantifiable uncertainties that can drive excess returns. The sensible framing of the problem is to think about how they can be mitigated without forgoing the most important opportunities.

In the current environment, we think there are four important risk axes where investors can legitimately debate whether simply avoiding the risk portends supernormal returns or whether its crystallisation could trigger stagnation or, even worse, a genuine market relapse.

Those four are:

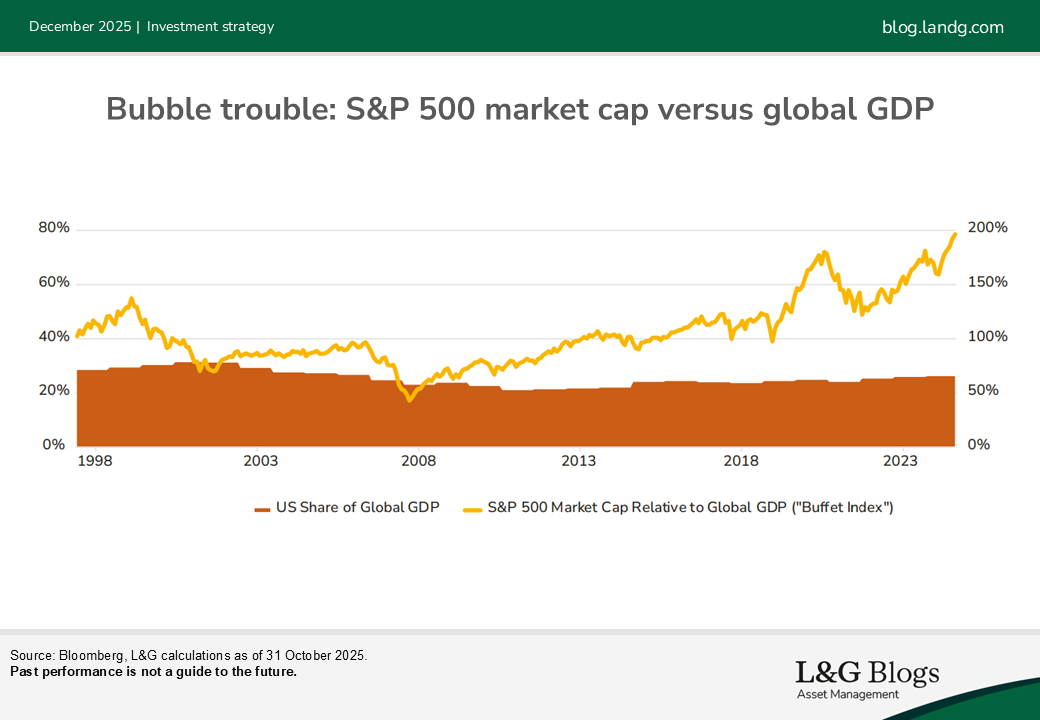

Bubble trouble. At the end of the third quarter in 2025, according to Bloomberg data, the market cap of the so-called ‘Magnificent Seven’ stocks in the US exceeded the market cap of the MSCI EAFE index, representing the 700 largest stocks in Europe, the UK, Japan and the Asia-Pacific. Debate is swirling about the validity of comparisons to the concentration risk of the dotcom boom in the late 1990s.

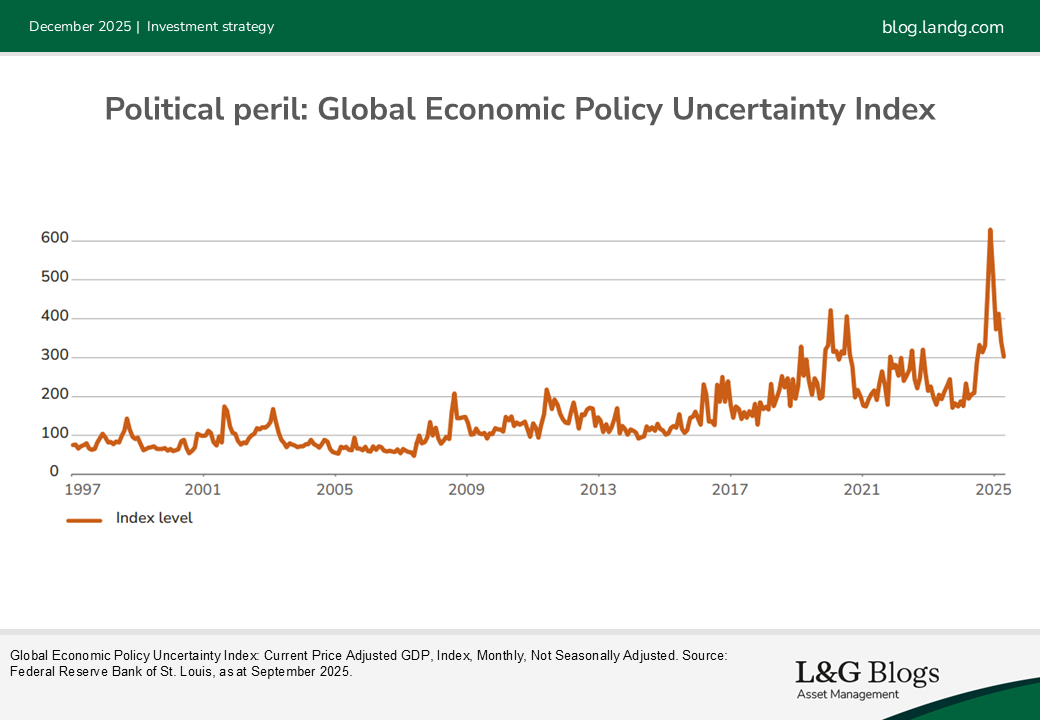

Political peril. The political outlooks for the US, UK, EU and China continue to be endlessly scrutinised, with attention inevitably skewed towards the former. The US heads to mid-term elections in November 2026, and a Republican ‘clean sweep’ victory would offer up the prospect of additional radical reshaping of the US government in the final two years of the Trump administration. We think a Democrat victory in either House of Congress would imply that two years of legislative paralysis beckons.

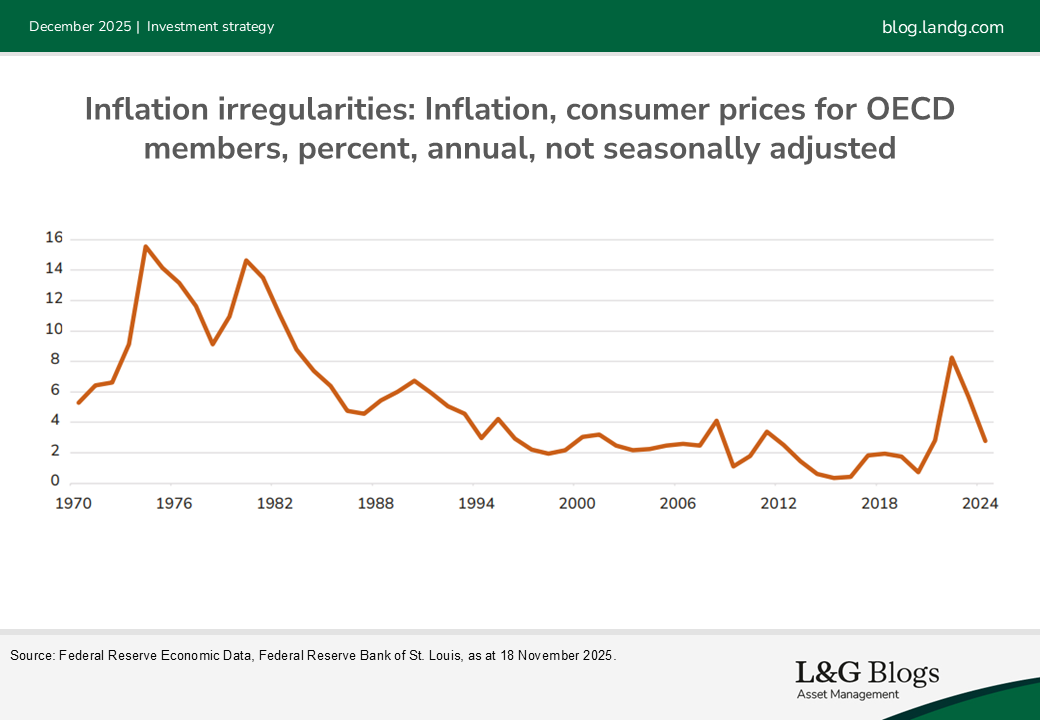

Inflation irregularities. The aftermath of the pandemic, combined with the Russian invasion of Ukraine, drove inflation across the OECD to levels not witnessed since the 1970s. Having been let out of the box so recently, it may be hard for investors to completely move on from inflation concerns.

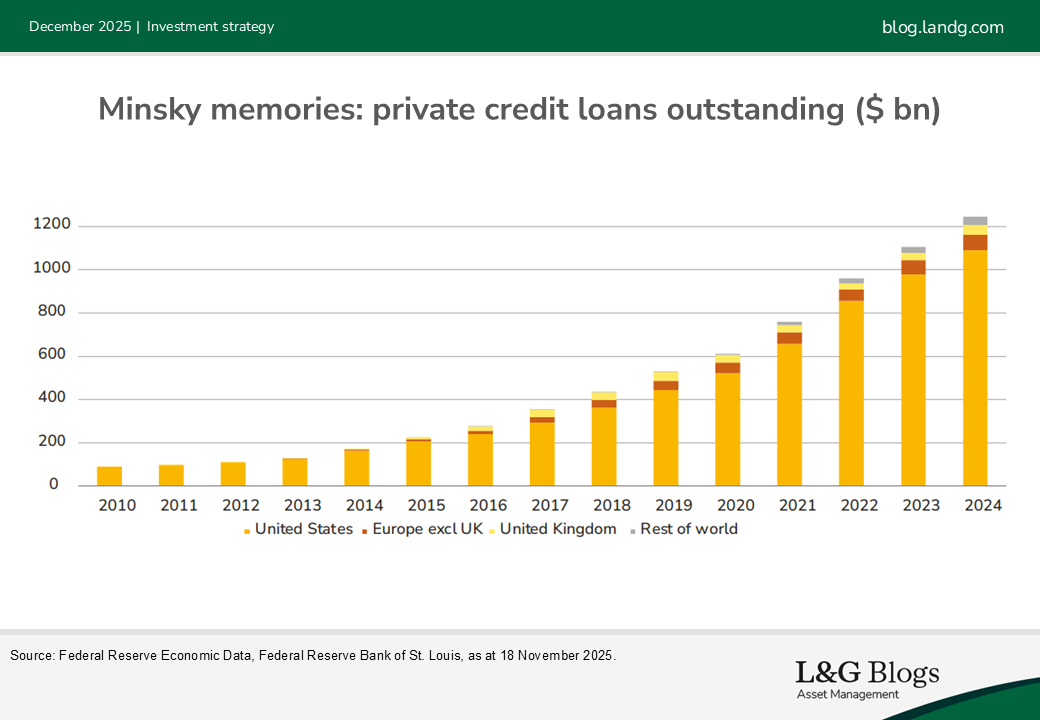

Minsky memories. The growth of private financing is a double-edged sword. Wider participation in private credit and equity increases the opportunity set for a broad range of investors, but fosters concerns about the rapid growth of financing outside of the most regulated channels. That inevitably draws comparison with previous episodes of rapid credit growth and the risk of overextension among both borrowers and lenders.

What do we do about these concerns?

There is extensive evidence that the perception of higher uncertainty leads to heightened risk aversion and amplifies behavioural biases such as familiarity and home bias.[1] It is linked to the idea of ‘reckless prudence’ – insufficient risk-taking to realistically meet long-term objectives. We’d argue that’s almost the opposite of what is needed.

Instead, we aspire to build ‘resilient portfolios’.

What does that mean? We can divide a list of initiatives that we can use to think about this into strategies at the total portfolio level and those which operate at the asset-class level.

At the total portfolio level, steps include:

(1) Adding alternative public assets: broad commodity ETFs can offer liquidity and simplicity, while synthetic commodity exposure can enhance capital efficiency. Investors typically have a small, if any, allocation to commodities, which can diversify traditional exposures to equities and fixed income.

(2) Adding private assets: investors have long looked to private markets with the aim of enhancing portfolio outcomes through a combination of complexity and illiquidity premia, in addition to diversification. Certain market segments offer access to industry sectors and business types that are hard to access via public markets, such as social and affordable housing. We think affordable housing can be attractive to clients who take a very long-term view in portfolio construction and value the prospect of stable, inflation-linked returns over liquidity needs.

(3) Adding alternative risk premia may be increasingly attractive for targeting returns as the risk / reward outlook for equities becomes ever more challenging. Investors seeking to clear a return hurdle may be compelled to move beyond traditional asset classes in search of consistent, repeatable outcomes.

(4) Risk-conscious hedging of unacceptably poor outcomes may seem uncompelling given the historically poor carry – the return or cost of holding the position. However, we see equity hedges as priced fairly (relative to their own history) going into 2026. Prospectively, though, the four risk axes outlined above seem poised to pull portfolios strongly away from central expectations in any one of those directions. Direct hedging ensures resilience in the face of those risks.

Within established asset classes:

(5) Sector and geographical diversification[2] can be achieved through active risk taking or strategic benchmark design and selection. In recent years, sectors and markets with less challenging valuations generated strong absolute returns while being largely overshadowed by US large cap tech. Active asset allocation can help identify ample opportunities outside the mainstream. In private markets, asset owners are increasingly considering complementing US exposures with allocations to Europe and, selectively, APAC.

(6) Decorrelated niches: as an example, within private credit, there is a spectrum of risk-return profiles. Many investors now have substantial allocations to sub-investment grade lending. Although returns have been healthy, this does come with associated credit risk. The investment grade space in private credit, which has long been used by insurers to match liabilities, has a track record of credit quality being substantially insulated from the economic cycle.

We will conclude with another, unaltered quote from a Tolstoy novel: “All the variety, all the charm, all the beauty of life is made up of light and shadow”. By accepting the shadow of uncertainty, and harnessing the light of strategic allocations, we seek to construct truly resilient portfolios for our clients.

Read our 2026 global outlook

[1] See Prospect Theory: An Analysis of Decision under Risk, by Daniel Kahneman and Amos Tversky (1979)

[2] . It should be noted that diversification is no guarantee against a loss in a declining market.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.