Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Assessing the appeal of agency MBS floating-rate bonds

We believe agency mortgage-backed security (MBS) floating-rate bonds can offer attractive value, flexibility and price stability – though they come with increased structural complexity.

Agency floating-rate bond issuance has surged in recent years fueled by demand from a variety of investor types. These bonds offer many benefits including short durations and the absence of credit risk – principal and interest are guaranteed by Fannie Mae, Freddie Mac or Ginnie Mae. To be sure, agency floaters tend to be more structurally complex than competing floating rate alternatives. But we believe they offer attractive value for investors willing to assume the unique risks inherent to this asset class.

Why floating-rate assets?

Floating-rate bonds, or “floaters,” bear a coupon that is set to a benchmark rate (typically SOFR) plus a “reset margin.” Floaters tend to have very limited interest rate sensitivity and are therefore easier and cheaper to hedge than their fixed-rate counterparts. Floaters tend to outperform in a rising rate environment because their prices remain relatively stable while fixed-rate bond prices are falling. Floaters can also perform well vis-à-vis fixed-rate bonds when the yield curve is flat or inverted.

Demand for floating rate assets began increasing in 2022 as investors sought out price stability amid rate hikes. But momentum has remained strong since the Federal Reserve started cutting rates in September 2024, supported by an inverted yield curve, persistent macro uncertainty and sticky inflation, which may constrain further easing.

Agency floaters trade credit risk for analytical complexity

Agency MBS floaters are a part of the broader agency collateralized mortgage obligation (CMO) market, which includes a wide variety of structures and bond types. Most mortgage loans in the US are fixed rate, so most mortgage pools bear a fixed coupon. Mortgage structuring desks can split the cash flows from a fixed-rate mortgage bond to create a floating-rate bond (whose coupon is set to the benchmark rate plus a reset margin) along with an “inverse” bond (whose coupon moves in the opposite direction to the benchmark rate). The face amounts, coupon formulas and principal allocation rules on the floater and the companion inverse bond are set such that the sum of their cash flows equals the cash flows on the underlying fixed-rate bond.

As mentioned above, agency floaters do not have credit risk. But they tend to be structurally and analytically more complex than other floating-rate alternatives such as collateralized loan obligations (CLOs), non-agency residential mortgage-backed security (RMBS) floaters and asset-backed security (ABS) floaters. A key distinguishing feature is that agency floaters are capped, while CLOs and most ABS floaters are not. For example, a bond might pay “SOFR + 1.5% with a cap of 6%.” If SOFR rises to 4%, the bond pays 5.5% (4%+1.5%). But if SOFR goes to 4.5%, the coupon gets capped out at 6%. Furthermore, agency floaters carry prepayment risk. Therefore, investors need to consider the structure of the underlying fixed-rate bond as well as the collateral characteristics.

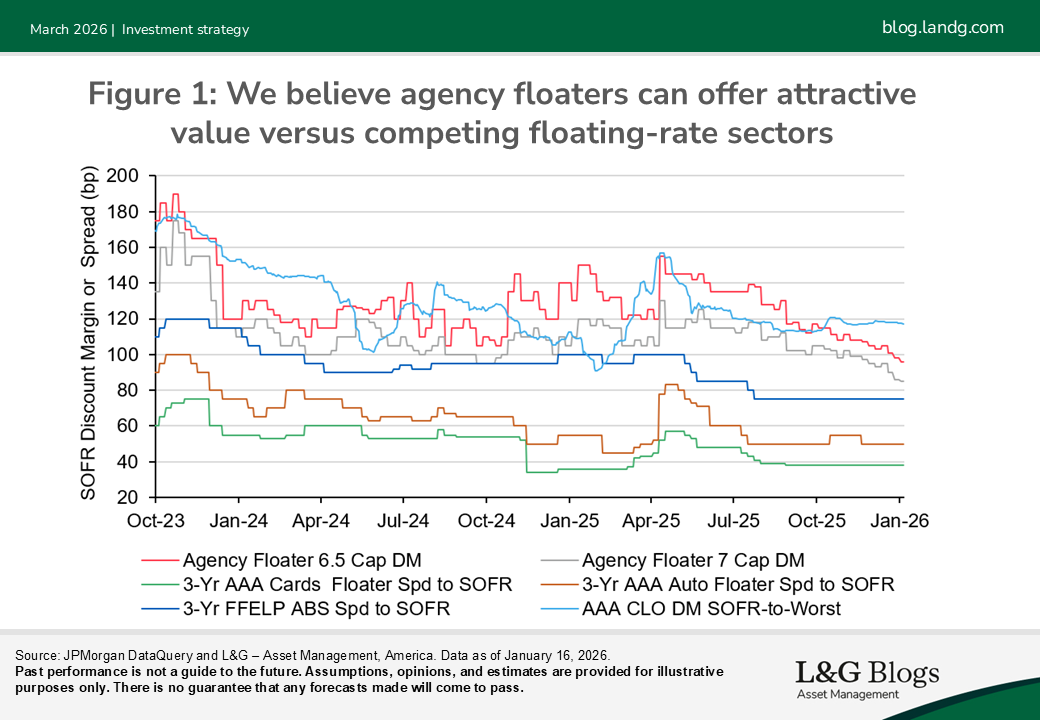

Figure 1 shows agency floater discount margins along with spreads on a variety of competing sectors. With the caveat that spreads across sectors are not directly comparable because of structural differences, the chart illustrates that agency floater spreads have generally been compelling versus competing sectors over the past couple of years.

Issuance has reached record levels

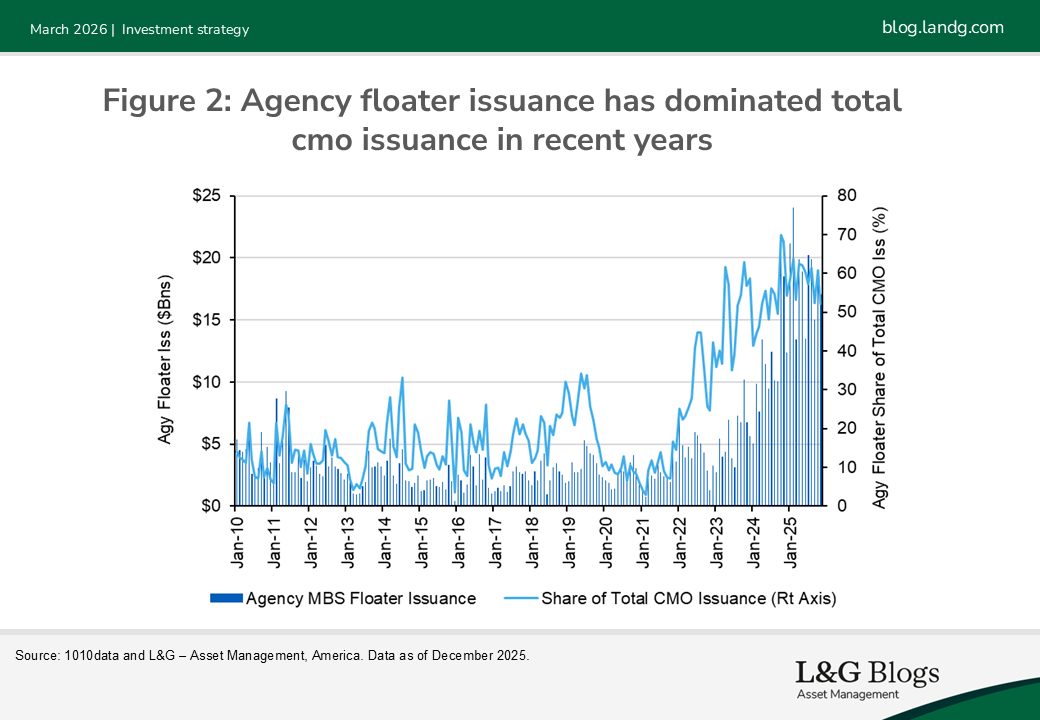

Issuance has surged since mid-2022, in absolute terms as well as in terms of the share of total CMO issuance (see Figure 2). The same factors that have driven broad demand for floating-rate assets have also supported demand for agency floaters. Banks have been particularly active buyers, drawn by minimal duration and favorable regulatory capital treatment, especially in the aftermath of the 2023 regional banking crisis.

Key considerations when investing in agency floaters

The structural complexity of agency floaters gives rise to unique risk factors and opportunities. Some important points to keep in mind when evaluating agency MBS floaters:

Spread must be balanced with cap risk. Floater reset margins are set to compensate investors for the level of cap risk on the bond. A lower cap or a longer weighted average life increase cap risk, all else equal. Investors who believe that 1-mo SOFR is biased lower can opt for a lower cap in exchange for a wider reset margin.

The bonds inherit the prepayment risk of the underlying. Faster-than-expected prepayment speeds when rates rally hurt floater returns because prepaid principal needs to be deployed into a lower-margin floater (for the same cap). Conversely, slower-than-expected prepayments into a rates selloff extend the bond, increase cap risk and erode returns. Prepayment risk can be alleviated by selecting collateral with a better convexity profile or by choosing a floater backed by a bond with relatively stable cash flows (such as a planned amortization class).

The market is diverse with a wide variety of bond types to choose from. The structural complexity of agency floaters creates flexibility. Investors can choose the cap, reset margin, underlying bond structure and underlying collateral to express customized views on rates and prepayment speeds and to achieve the desired risk-profile.

Closing thoughts

Agency MBS floaters have become a mainstream investment holding for many institutions. These bonds allow investors to add agency mortgage market exposure with minimal duration. They are potentially an attractive diversifying asset for investors willing to trade credit risk for increased structural complexity. Their characteristics create analytical nuances and introduce new risks. In exchange, we believe these bonds can offer attractive value, flexibility and price stability.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.