Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

March of the machines

While some companies will benefit from AI-driven efficiencies, others will find their business models profoundly challenged.

The following is an extract from our latest CIO Outlook.

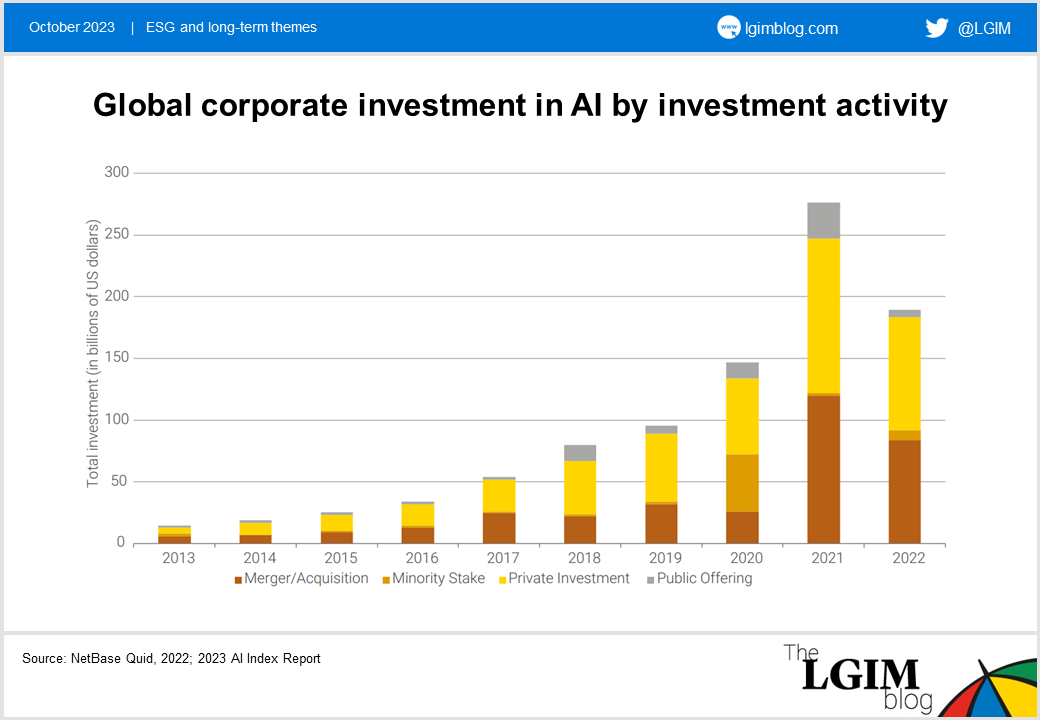

Many companies are making considerable investments in AI – across sectors, spending on the technology increased 35% annually between 2018 and 2021.[1] But will the companies that have invested the most be the greatest beneficiaries of the AI frenzy, or are they in fact those with the most to lose?

Companies across industries are exploring new ways to benefit from the AI revolution, as they seek to optimise their cost bases. In healthcare, AI heralds the prospect of de-risking the notoriously expensive and time-consuming business of drug discovery. The combined pipeline of 20 AI-native drug discovery companies has been found to have reached around 50%[2] of the scale of the equivalent pipeline for 20 of the largest pharmaceutical companies, suggesting some degree of increased efficiency.

Paint shops, plants and M&A

Even in capital-intensive industries, we believe AI has the potential to deliver tangible cost benefits. At its plant in Rastatt, Germany, carmaker Mercedes-Benz* has used an AI system to increase efficiency in its paint shop. Compared with a more conventional control system, the AI-led approach has resulted in energy savings of 20%.[3] Titan Cement* has deployed AI-based, real-time optimisation software in eight of its plants, resulting in up to 10-15% improved throughput and a 5%-10% reduction in energy consumption.[4]

In a post-pandemic world, characterised by labour shortages, AI offers companies the prospect of reduced labour costs and increased efficiency. In May of this year, telecommunications giant BT* announced a plan to cut 55,000 jobs by the end of the decade, with 10,000 being attributed, by the CEO, to roles that could be replaced by new technology including AI[5] (although we are a little sceptical of this claim).

But while AI promises much in the way of cost savings and optimisation, we believe it also poses risks to companies with established business models, where barriers to entry may be lowered by a shift to a more AI-powered ecosystem. In May of this year, shares in education-technology company Chegg Inc*, fell almost 50% after the company warned that ChatGPT threatened the growth of its homework-help services.

Moreover, at this early stage, it’s far from clear which companies will dominate the eventual AI landscape, meaning that some incumbent technology businesses may be left behind. For example, large language models (like ChatGPT) with their ability to generate high-quality text for search queries, web content, or advertisements could eventually disrupt the traditional business model of Alphabet* (Google).

As new challenges surface, and new AI-powered enterprises emerge, we may also see an increase in M&A. In one of several AI-related deals announced this year, last month, tech company Cisco* announced that it would be acquiring software firm Splunk* for US$28bn, in a deal aimed at beefing up its offering in AI cybersecurity.

Potential effects on equities and credit

The implications of this AI revolution may differ between equity and credit markets. Equity markets are more weighted and influenced by large US technology companies, as well as more service-focused businesses, with an asset base comprising a higher proportion of intangible assets. Credit indices, on the other hand, tend to include a greater proportion of companies that are either more established, or more regulated – suggesting a greater degree of risk and also reward in the equity market in the short term, with the impact taking longer to filter through to bondholders.

The above is an extract from our latest CIO Outlook.

*For illustrative purposes only. Reference to this and any other security is on a historical basis and does not mean that the security is currently held or will be held within an LGIM portfolio. Such references do not constitute a recommendation to buy or sell any security.

[1] Standford University’s Institute for Human-Centered AI, 2023

[2] AI in small-molecule drug discovery: a coming wave? Madura K.P. Jayatunga, Wen Xie, Ludwig Ruder, Ulrik Schulze, Christopher Meier.

[3] Mercedes-Benz pioneers ‘Digital First’ production for next-generation MMA platform | Mercedes-Benz Group > Innovation > Digitalisation > Industry 4.0

[4] Titan Cement international presentation as at August 2023.

[5] BT to cut 55,000 jobs with up to a fifth replaced by AI - BBC News

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.