Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Words of wisdom? “Picking up pennies in front of a steamroller”

Our Well-known Investment Saying Evaluation (WISE) index provides an assessment of some well-worn financial aphorisms.

The following is an extract from our research report: Do famous investment savings hold water?

“Picking up pennies in front of a steamroller” – WISE score: 10/15

Durability: 2/5

Popularised by Nassim Taleb in his 2007 book ‘The Black Swan: The Impact of the Highly Improbable’, this maxim is relatively new, even if the underling idea itself is not.

Taleb himself spoke about the concept as it relates to carry at the start of the century in another of his books, and the distribution has since been named after him.

Reliability: 4/5

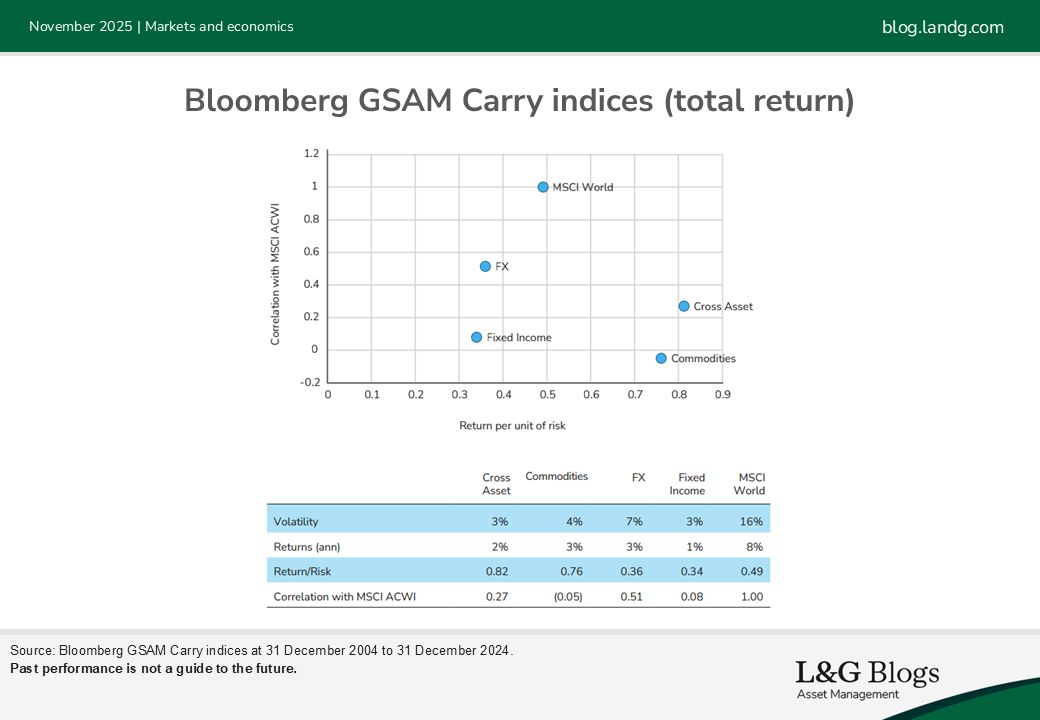

‘Carry’ is a trade that involves borrowing at a low interest rate and investing in an asset that provides a higher rate of return. As a concept, it can be applied in many asset classes,

making generalisation of its performance difficult. In currencies, empirical evidence[1] suggests that carry works (contradicting the theory behind the covered and uncovered interest rate parity concepts), but that it comes with reasonable correlation to risk markets. In other markets it’s less clear.

That said, these comments are made on short back tests of merely 20 years; a warning flag for extrapolation

Insight: 4/5

Making up one of seven of our factors for scoring tactical trades, carry has a relatively prominent role in our process. In systematic risk taking, we tend to pair carry with other

factors: in long-term models where valuations play a key role but can take a long time to play out, pairing with carry ensures our ongoing cost of running the strategy isn’t overly punitive.

It’s what has stopped us buying the yen in recent years, for example. In emerging market FX, where carry can be especially large, we first adjust for inflation differentials then pair it with trend-following and enhanced risk management, designed to cut positions when they start underperforming.

Combined across asset classes, we believe these strategies can provide strong risk-adjusted returns while maintaining relatively low co-behaviour with risk assets.

[1] “Carry” by Ralph S. J. Koijen, Tobias J. Moskowitz, Lasse Heje Pedersen, Evert B. Vrugt.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.