Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Winner takes all in the UK higher education sector

With a focus on demographics and demand, we look at how trends in international student numbers could affect UK student housing. From our perspective not all universities are created equal.

Concerns over the previous UK government’s immigration policies and their impact on international student recruitment have been a dominant theme in the UK higher education sector and downstream to the student accommodation market.

Newly published UCAS data for the 2024/25 academic year intake showed a 2% decline in international undergraduate acceptances[1]. While this suggests the impact was more muted than some may have feared, there is more nuance behind the headline numbers.

First, the most significant immigration policy changes primarily affect postgraduate students, not undergraduates, which is not captured in the UCAS data. Moreover, the data only captures a portion of international student applications; there are other routes for international students to apply and enrol in UK university programmes, meaning the full picture remains incomplete. The data does, however, provide useful insight into how different universities are navigating a changing landscape.

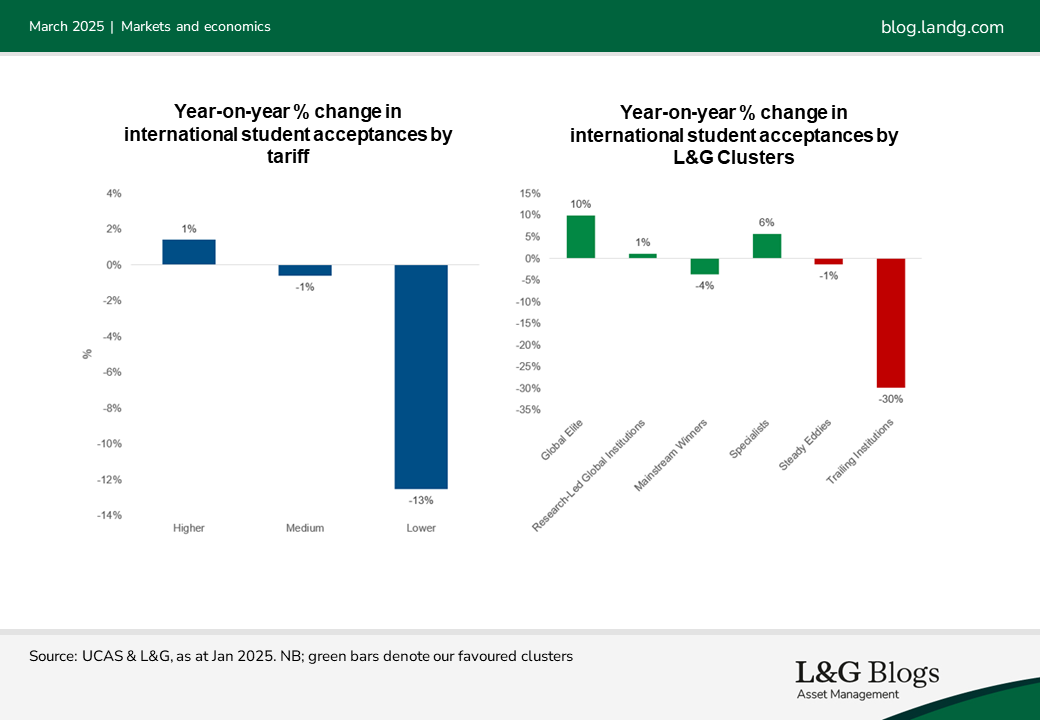

One clear theme from the 2024 recruitment cycle is the increasing divergence in outcomes between, broadly, higher-ranked and lower-quality universities. Universities typically regarded as more prestigious saw a modest 1% increase in international acceptances, while lower-tariff universities experienced a 13% decline. This drop was even more severe than during the suppressed pandemic recruitment cycle. A more granular look at the data highlights clearly that the pain was concentrated to particular institutions.

We have previously described our clustering analysis of universities, which provide a guide to institutions we see as best placed to benefit disproportionately from growing student numbers. Based on that classification, we note that the ‘Global Elite’ cluster – our classification of the cream of the crop – saw international student acceptances grow by 10%. The ‘Trailing Institutions’ cluster (our least-favoured cluster) saw a decline of 30%. This suggests that, much like during the pandemic, stronger universities were able to capture market share from weaker counterparts during a challenging recruitment cycle, reinforcing bifurcation in student demand.

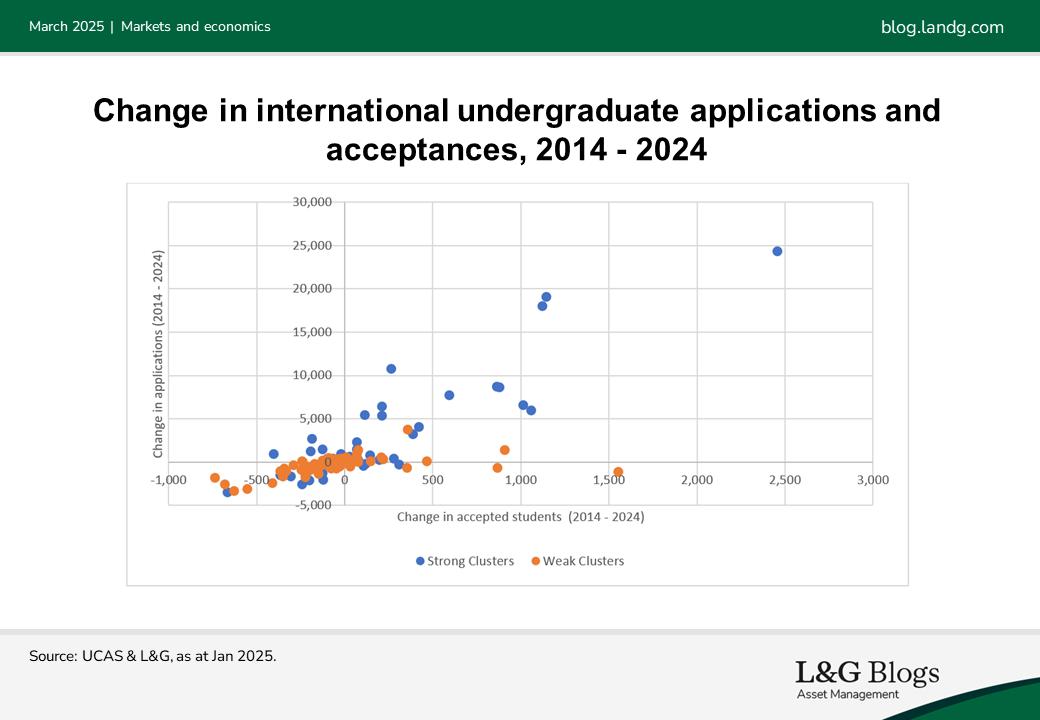

The longer-term view is also clear. International students take the chance to enrol in these better-quality universities when they can. The chart below compares applications and acceptance numbers over the decade, which we regard as an illustration of the underlying attractiveness of universities to prospective students. This shows that the best universities continue to be most favoured.

The financial implications of these shifts are significant. UK universities are increasingly reliant on international student tuition fees, which account for 23% of the sector's total income, ranging to over 50% in some universities[2]. At a time when many institutions are facing financial pressures, losing international students presents a material risk. Domestic students, while important, are not a sufficient financial substitute given the long-standing tuition fees cap in place. While the Labour Government is evaluating further increases in the tuition fee cap, it is unlikely to match international fees, in our view.

The financial implications of these shifts are significant. UK universities are increasingly reliant on international student tuition fees, which account for 23% of the sector's total income, ranging to over 50% in some universities[2]. At a time when many institutions are facing financial pressures, losing international students presents a material risk. Domestic students, while important, are not a sufficient financial substitute given the long-standing tuition fees cap in place. While the Labour Government is evaluating further increases in the tuition fee cap, it is unlikely to match international fees, in our view.

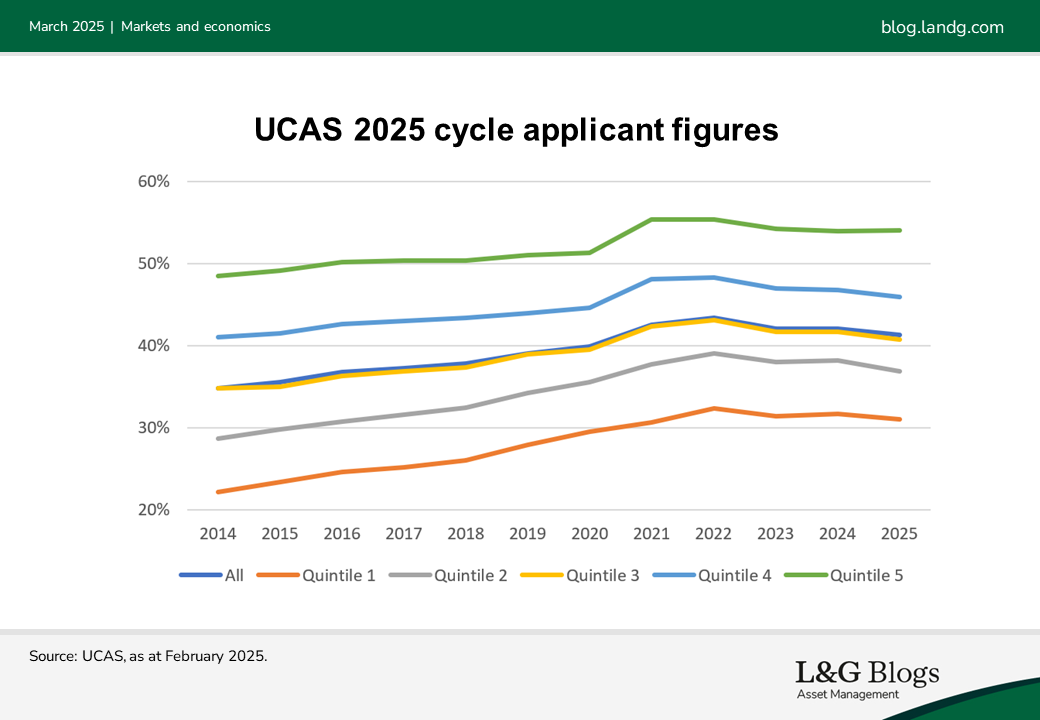

We also have some concerns that higher fees may disincentivise some households from heading to universities. The expected demographic tailwind of more 18-year-olds in the UK may not necessarily materialise into stronger student numbers. Early data from UCAS on the 2025/26 academic year cycle showed that, although 18-year-old application numbers were up in January 2025 compared to 2024, the participation rate (the number of applications divided by the total number of 18-year-olds) was down by a percentage point. Notably, participation rates were down across all but the least deprived areas in the UK[3].

Despite these domestic challenges, there are signs of a potential recovery in international student numbers. UK Home Office study visa data showed a 15% rise in applications in December 2024 and January 2025, compared to the equivalent months in the previous year[4]. This is still below pre-visa changes levels but suggests some recovery. Further, the global landscape for international students is changing, with other key destinations such as the US, Canada, and Australia imposing higher barriers to entry for international students. If the UK remains an attractive and accessible option, we believe it could capture a larger share of a growing global pool of mobile students.

Despite these domestic challenges, there are signs of a potential recovery in international student numbers. UK Home Office study visa data showed a 15% rise in applications in December 2024 and January 2025, compared to the equivalent months in the previous year[4]. This is still below pre-visa changes levels but suggests some recovery. Further, the global landscape for international students is changing, with other key destinations such as the US, Canada, and Australia imposing higher barriers to entry for international students. If the UK remains an attractive and accessible option, we believe it could capture a larger share of a growing global pool of mobile students.

However, the pattern is unlikely to be uniform across the sector, in our view. The trend of ‘winners keep winning’ appears set to persist, with the best universities strengthening their position while weaker universities struggle.

For investors in student accommodation and higher education-linked assets, these trends underscore the importance of selectivity. Our view is that average expected returns for the sector are strong, relative to other sectors[5], but this does not mean widespread performance across locations. Assets in leading university cities remain attractive, while exposure to assets, prime or otherwise, in struggling institutions may present greater risk. The longer-term outlook will hinge not just on policy changes but on how well individual universities in the UK can position themselves in an increasingly competitive market for international students.

[1] UCAS Undergraduate End of Cycle Data 2024, as at Jan 2025

[2] HESA Tuition Fees & Education Contracts by HE provider as at Dec 24

[3] UCAS January deadline applicants and applications 2025 as at Feb 25

[4] UK Home Office, Monthly Entry Clearance Visa Applications as at Feb ‘25

[5] PMA UK National Forecast Winter 2024 as at Dec 2024

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.