Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

What’s been happening in government bond markets?

Following on from our UK-focused LDI chart update on Friday, we take a broader look at the recent yield rises across government bond markets, including our thoughts on what that implies for equity markets and how events could potentially unfold from here.

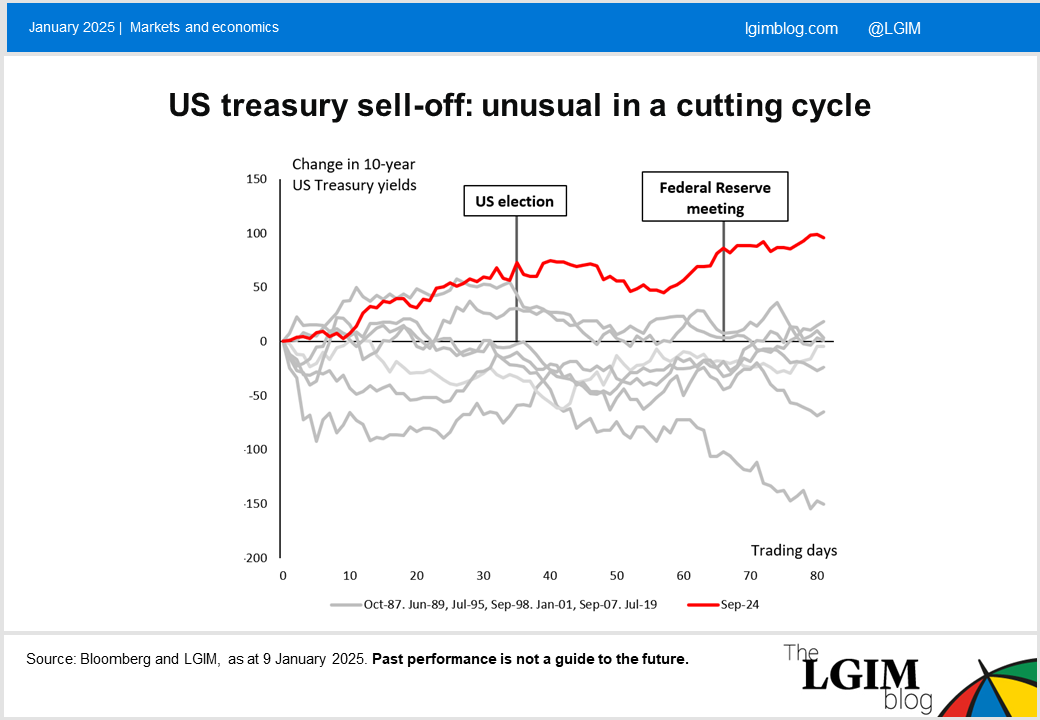

Globally, bond yields have climbed steadily higher towards the end of last year. That move was initially led by US treasuries and, counterintuitively, started when the rate-cutting cycle began in mid-September.

This was exacerbated by two events in Q4:

- The US election in November. Some investors expect Trump’s trade, fiscal, deregulation and immigration policies to be net inflationary, which can lead to higher government bond yields

- The Federal Reserve (Fed) meeting in December, which signalled an end to meeting-by-meeting cuts in policy rates. Economic data suggested that while inflation is moving back towards the Fed’s target, growth has remained resilient, dampening hopes of rapid rate cuts in 2025

As we enter 2025, supply has also moved into focus. January is a seasonally heavy supply month globally and we have already started to see a significant supply of bonds across corporates, sovereigns and supranationals.

In the UK, issuance for this fiscal year was revised higher in October’s Budget, and the Bank of England are frontloading their active quantitative tightening (QT) sales to the first month of each quarter, which has added to the January supply pressures. This has accelerated the trend observed over the final quarter of 2024.

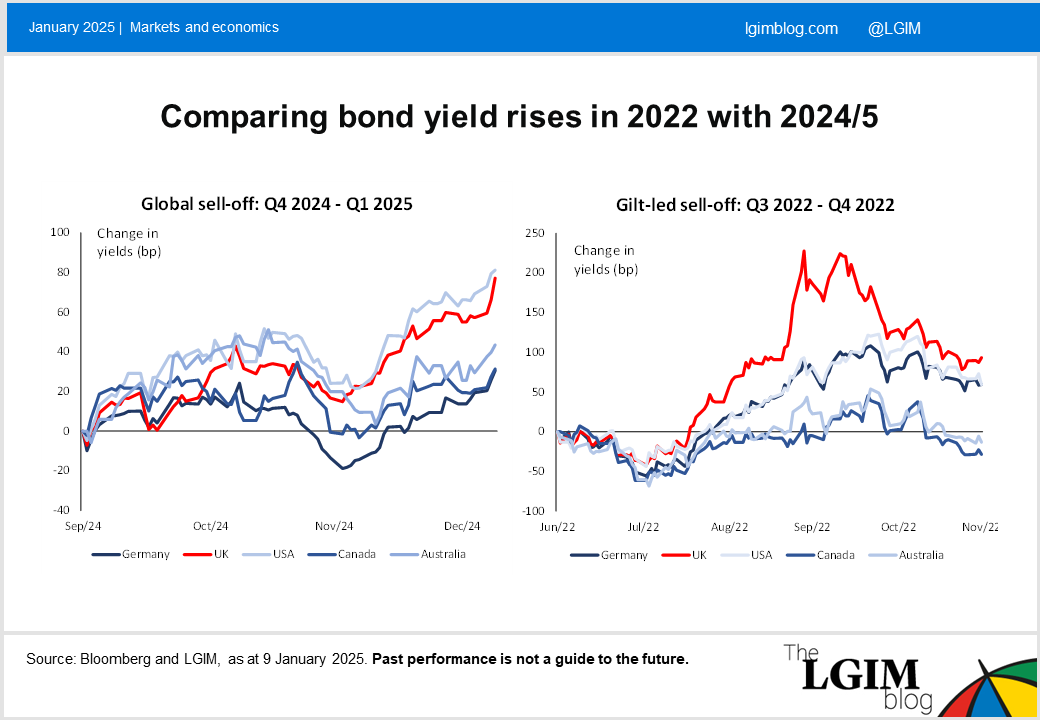

Although gilt yields have largely moved in parallel with major markets such as the US, there has been an idiosyncratic element of sterling weakness in recent trading days. This is very different to the dynamic in Q3 2022 where gilts and the UK currency were very weak in isolation for an extended period. However, should this recent trend continue it would act as a potential buffer for returns in any sterling-denominated portfolios with unhedged exposure to overseas assets.

Despite the increase in yields, markets remain orderly. The magnitude of daily and intra-day moves in gilt yields is far lower than we saw around the 2022 mini-Budget.

One development which carries echoes of 2022 is the weakening of sterling alongside rising gilt yields. That acts as a potential buffer for returns in any sterling-denominated portfolios with unhedged exposure to overseas assets.

What have the yield moves implied for equity markets?

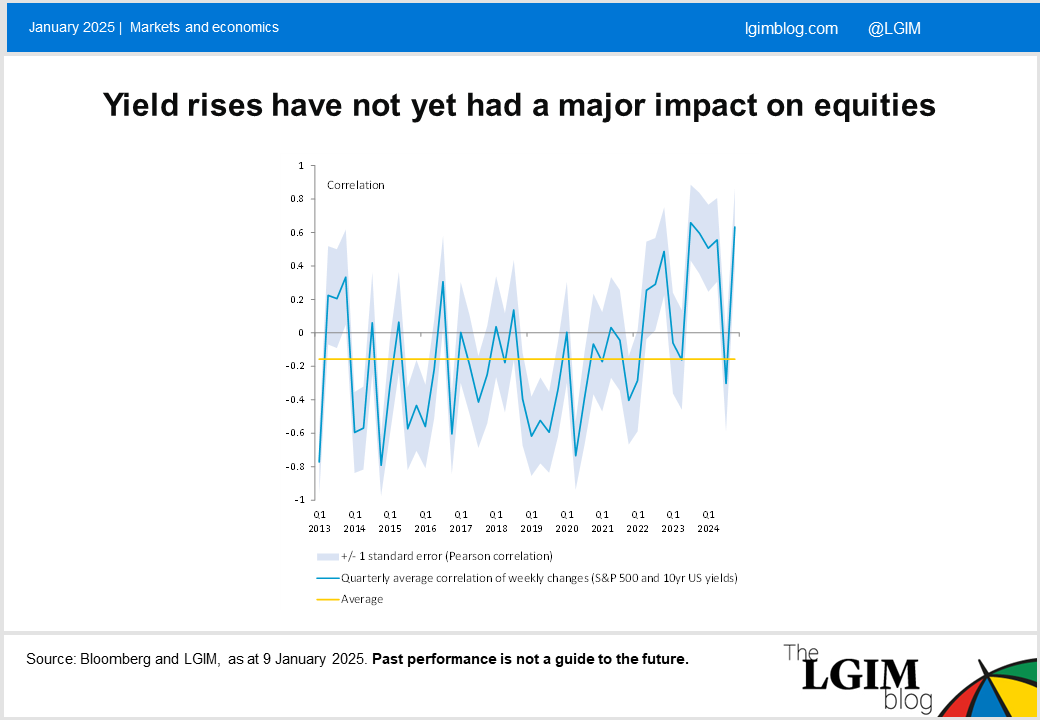

Relatively high frequency measures of the correlation between equity and bond returns turned positive again in Q4, having dipped back to their long-run average in Q3. However, that obscures the fact that rising bond yields have not yet been a material drag on equity returns.

In the fourth quarter, global yields were up 60bps but the MSCI World still delivered local currency returns above 1.5%.

Rising bond yields however have had very different impact on certain parts of the market. REITs are down over 10% in absolute terms since the start of Q4, while banks have been among the best performing sectors in both the US and Europe.

How do we think this will unfold from here?

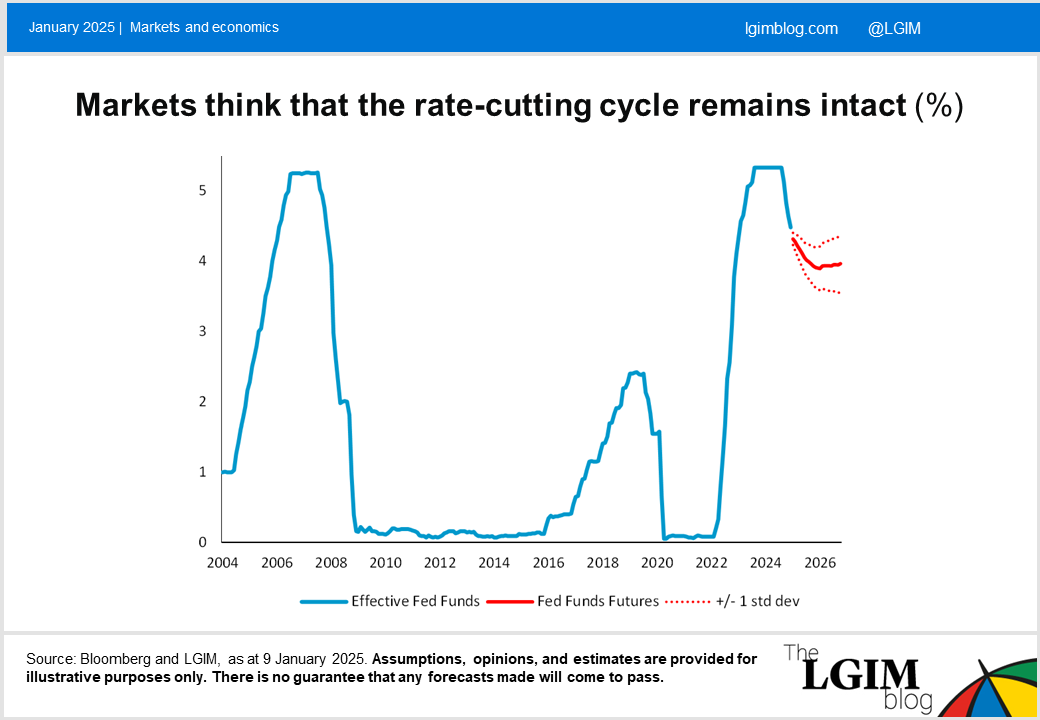

Looking ahead, economic data in the US and in various other developed markets show that a disinflationary trend remains underway. Hiring in the US has remained much stronger than elsewhere, but even in the US wage growth has been moderating. Providing US unemployment does not fall back below 4%, we expect government bond markets to trade towards estimates of the neutral rate over the longer term.

In the absence of data that disproves a gradual return to target consistent levels of inflation, we expect central banks to continue to cut rates in the search for neutral. And as this happens, we expect market pricing of rates to be biased towards lower yields.

In the UK, we believe that the government’s ongoing commitment to their recently announced fiscal rules is paramount to help stifle any fears of 2022 redux. We have no reason to doubt that commitment will hold.

More broadly, we think that rising bond yields only become a sustained problem for the equity market if the conversation turns from pace of cuts to another hiking cycle. That remains a relatively distant prospect.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.