Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

US bankruptcy surge fuels recession fears

A leading indicator suggests US corporates are already struggling under the weight of higher rates.

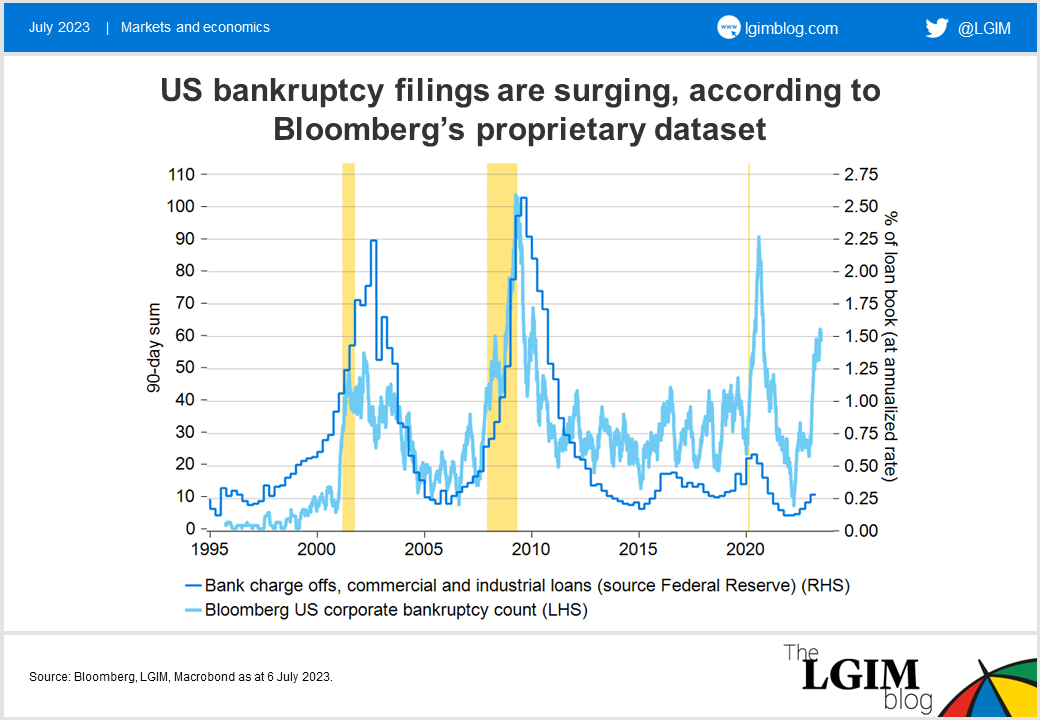

Bloomberg’s proprietary dataset of US bankruptcy filings is sending a worrying signal.

Since the start of the year, the data suggest the number of companies filing for bankruptcy has shot up, much like in previous recessions in 2001, 2008 and 2020 – highlighted by the yellow bands in the chart below.

This proprietary dataset has historically tended to act as a signal of upcoming changes in official quarterly data on Chapter 11 filings or bank charge-offs (loans that have been written off as a loss).

What’s behind the rise?

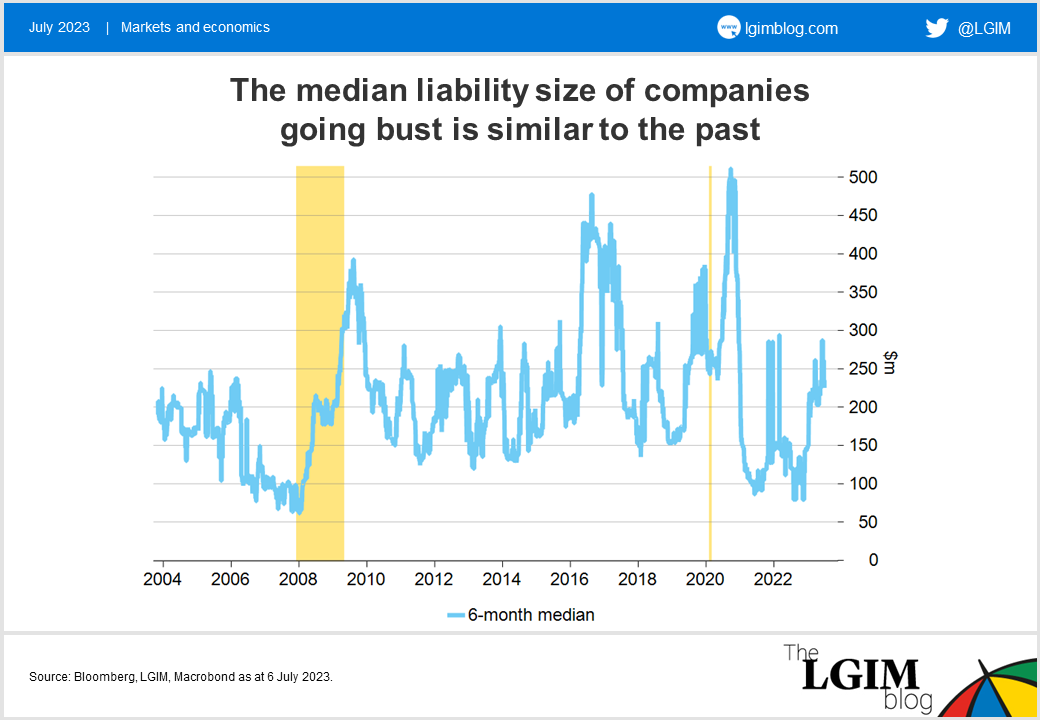

We first wondered if the data might be distorted by a large number of microbusinesses going bust, perhaps reflecting the delayed effect of fraudulent lending taken out during the pandemic. If this were the case, the number of companies going bust would exaggerate the stress in the economy compared with a sales- or employee-weighted index.

Bloomberg provides data on the liabilities and assets of some (but not all) of the companies going bust. Examining this data, we found the median reported liability of companies filing for bankruptcy had not only increased since the start of the year, but was also similar to the level seen during the past two decades, and in previous recessions.

So, we don’t think the bankruptcy count is distorted by a large number of small companies going bust.

What does this mean for the economic outlook?

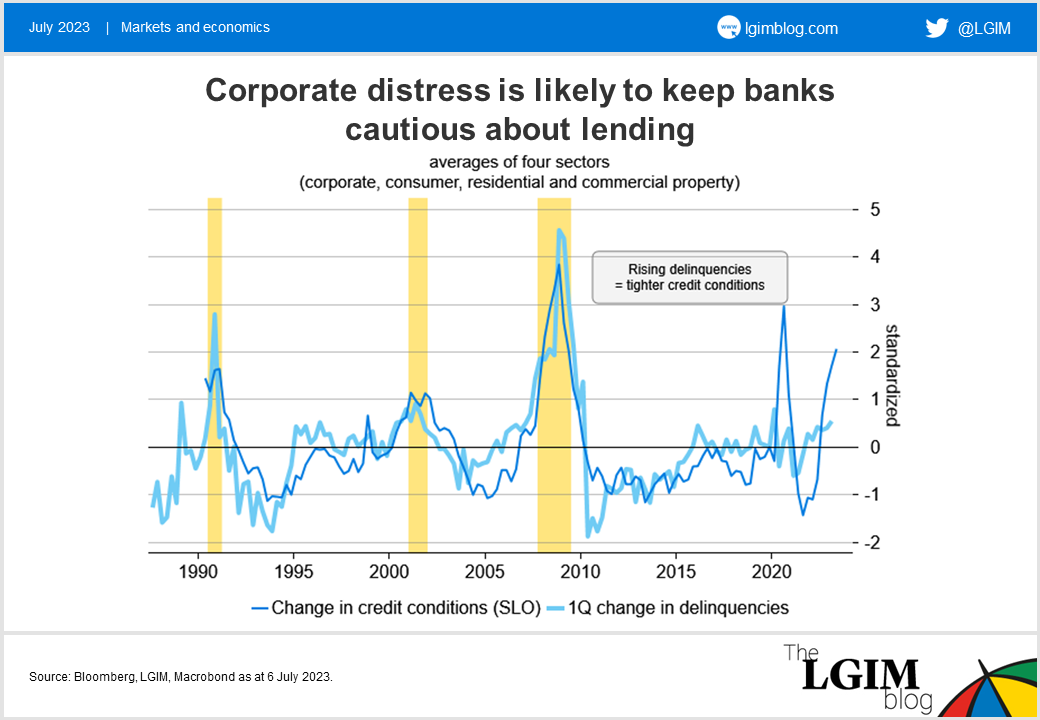

We think the rise in the number of companies filing for bankruptcy and the rise in the median liability of these companies increases the risk of recession through a self-reinforcing tightening of credit conditions and weaker growth.

We’ve shown before how banks become more cautious about lending when previous loans sour (for example, as delinquencies rise). Bank lending is pro-cyclical, making booms bigger and downturns deeper. Corporate distress is likely to keep banks cautious.

On the positive side, the surge in Bloomberg’s bankruptcy index in 2020 resulted in only a limited rise in bank charge-offs. This likely reflects the huge monetary and fiscal stimulus thrown at the economy, including offering companies government-backed loans via the Main Street Lending and the Paycheck Protection programmes.

This time is different. Policy is being restricted, not loosened. The rise in distress likely reflects the pain from higher interest rates. Leveraged-loan issuance has surged over the past decade. Given such loans are predominantly floating, this exposes companies to rises in the Fed funds rate, which has jumped by 500 basis points in just over a year.

In contrast to consensus optimism about a ‘soft landing’, we think a sustained rise in unemployment is needed to bring inflation down. We expect a recession soon and maintain caution on risky assets.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.