Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Trumpification of the Fed

How serious is the threat facing the independence of the bank? And if independence erodes, what might happen next?

The following is an extract from our Q4 2025 Asset Allocation outlook.

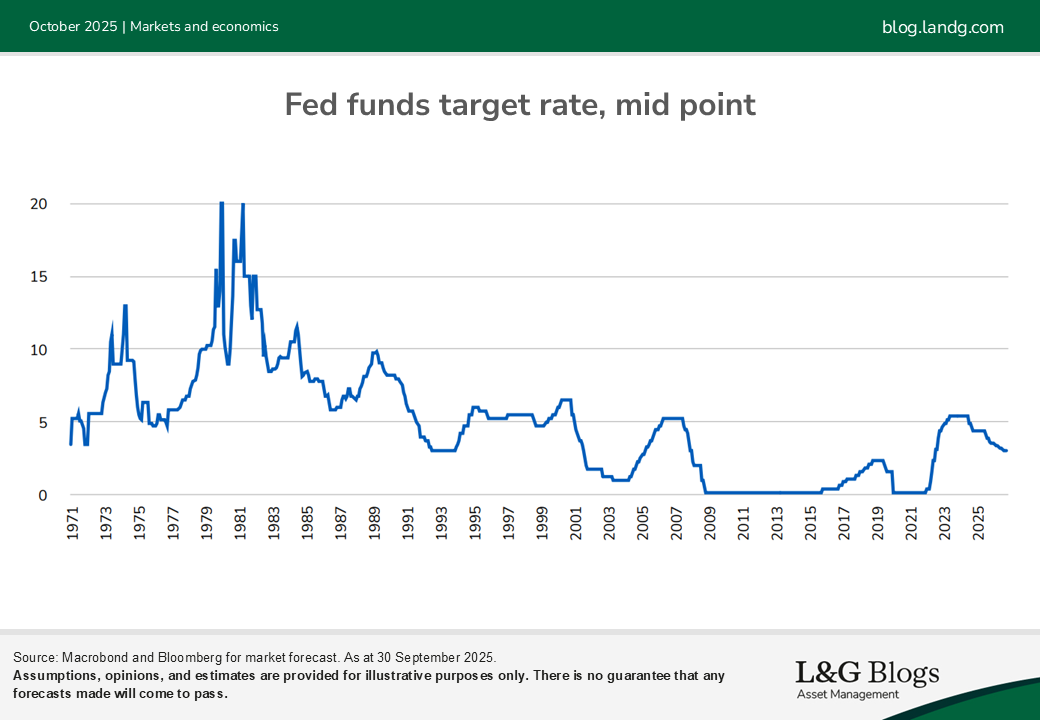

There has been intense presidential pressure on the Fed to cut rates (Jerome “too late” Powell). This serves the purpose of deflecting blame should the economy turn down unexpectedly. So far, the Fed has ignored the political noise and conducted policy with its best intentions for the long-run health of the economy.

But is independence of the Fed under more serious threat? There has already been one early resignation from the Fed Board (Governor Kugler) with Stephen Miran now confirmed to temporarily fill the seat and voting for aggressive rate cuts.

There is also the prospect of another seat opening up, with Governor Cook accused of mortgage fraud and the president calling for her to resign immediately. She is resisting, citing a ‘clerical error’, and so far the courts have ruled the president does not have ‘cause’ to fire her, with the Supreme Court appeal set to hear oral arguments in January. It is also unclear if the Department of Justice will take the case to trial.

Could Powell stay on?

Then there is the question of Powell’s seat. Typically, when the chair’s term ends, they step down from the Board of Governors. This could open up a third nomination for the president. Other seats could also be in play. Will Governor Barr want to continue? He may have stayed on to support Chair Powell after resigning in February 2025 from his role as vice chair for supervision. It is common for governors to not serve their full terms. Vice Chair Bowman and Governor Waller preferred to cut rates earlier and more aggressively than the rest of the Federal Open Market Committee and were appointed by President Trump in his first term.

While clearly dovish, both are expected to uphold Fed independence. However, if the White House gains influence over four new governors, it would have the ability to a make more radical changes (a quorum of four is required for decision making).

For example, the 12 regional Fed presidents’ five-year terms all expire at the end of February 2026. Normally, the reappointment by the Board of Governors is a formality, but this is now a critical moment for future Fed policy.

All Fed governor appointees have to go through the Senate confirmation process. This will not need any Democrats, as only a simple majority is required. Furthermore, the Senate has recently and controversially passed legislation which allows the bundling of nominations. This will make it even harder for Republican senators to vote against candidates, even if they have misgivings, as it would slow down appointments across a range of other agencies.

Market reaction:

Academic research and historical experience shows independent central banks are the best way to maintain long-run price stability as they can resist short-term political pressure. It takes years to build a reputation, and trust can be broken in an instant.

However, markets might even cheer at first. Consider the uncertainty around the neutral interest rate. If the market believes an independent Fed has kept policy too tight, a steady loss of Fed independence could lead to interest rates being brought down closer to their optimal level and growth might improve. Any negative consequences from higher inflation could take time to materialise.

The most severe reaction from financial markets might come if inflation starts to rise and a White House-controlled Fed denies there is a brewing inflation problem. This could lead to a sudden loss in the credibility of the Fed, rising inflation expectations and a weaker dollar. In theory, yield curves should steepen, but in extreme the Fed could introduce some type of yield curve control.

Read our Q4 2025 Asset Allocation outlook.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.