Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

The US swing factor

The world’s largest economy will likely determine which of a wide range of scenarios for global growth plays out in 2026.

The following is an excerpt from our 2026 global outlook

Global growth has been surprisingly resilient since the spring, despite the uncertainty caused by disruptive US trade policy. Growth has been aided by rapid AI spending and positive wealth effects on consumption from surging big tech stocks.

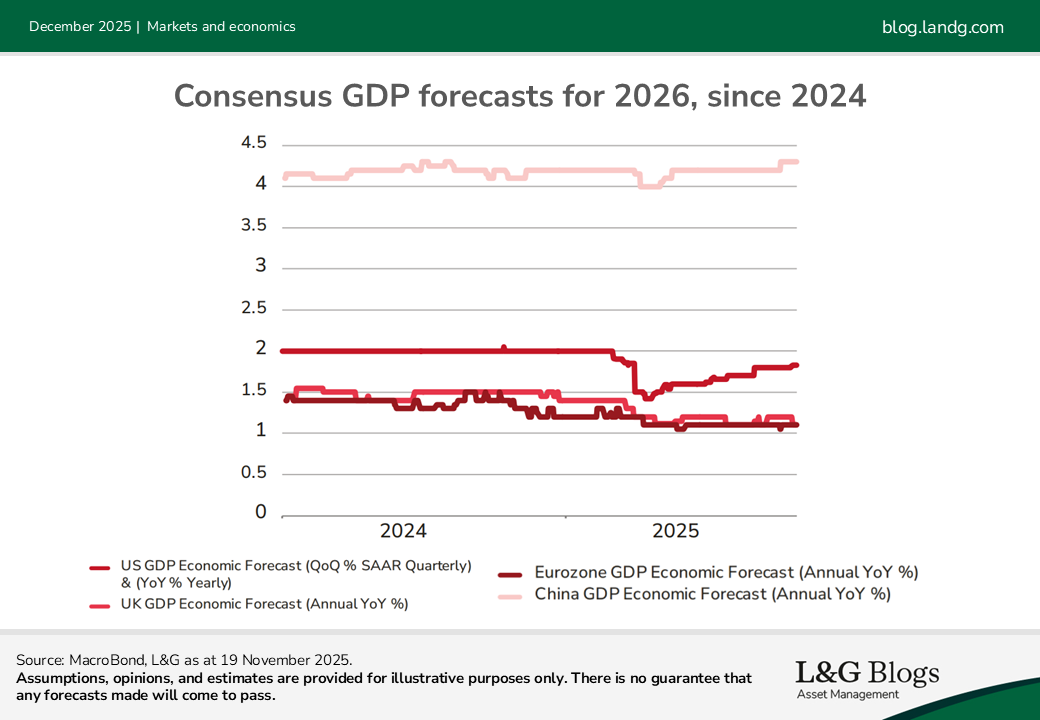

Looking ahead, consensus forecasts reflect a return to equilibrium in a number of economies during 2026, with global growth around trend, unemployment close to its natural rate, inflation potentially on a path towards target and many central bank rates moving to near ‘neutral’.

While central forecasts appear clustered around this view, there are a wide range of scenarios; these mostly reflect the US economy as the swing factor.

In the near-term, consensus expects a couple of softer quarters in the US as tariffs feed through into higher prices and this squeezes real incomes. But growth is expected to recover through 2026. Tariffs are seen as a one-off price level effect, which will fade, while consumers should receive a moderate boost to annual disposable income from rebate checks in the spring, given tax cuts in the One Big Beautiful Bill passed earlier this year.

The euro area has been more sluggish, but growth is expected to strengthen gradually from a turn in the global manufacturing cycle, with the potential for earlier rate cuts boosting interest-rate sensitive parts of the economy and government spending in defence and infrastructure gaining traction, notably from Germany.

As the chart shows, China is expected to grow in the 4-5% range with government support and a diminished drag from the property sector.

We see the UK as being relatively more vulnerable to weaker-than-expected growth, given tightening fiscal policy. However, this could trigger more interest rate cuts than the two priced by the Bank of England over the next year from 4% in November, in our view.

Downside and upside risks

Downside risks revolve around concerns the US labour market could weaken further, in our view. So far, the slowing in employment growth reflects both demand and supply factors, with immigration flows abruptly halting. But if layoffs were to increase, consumer job fears would intensify, likely triggering a pullback in spending. It is not clear that the Fed would be prepared to cut interest rates fast enough to fully offset this dynamic, especially if inflation is rising.

Tariff pass-through has proven more muted than expected so far, but this could be a delayed effect. Inventories were built in anticipation of tariffs; once they are depleted, firms might feel more compelled to raise prices.

Geopolitics remains another source of risk. For example, should the Supreme Court rule that the President has overstepped his authority in using the International Emergency Economic Powers Act to impose tariffs, this could inject a fresh round of uncertainty in US trade policy.

Upside risks mainly reflect the potential for continued strong investment in AI and business adoption, which could boost economy-wide productivity, as noted elsewhere in this outlook.

However, the AI roll-out has a number of challenges. There is a danger of over-investment. If return expectations are not met, AI-related equity prices could correct, delivering a shock to household wealth. Alternatively, the pace of change might be so fast that AI automation leads to job losses. The disruption could undermine consumer spending, even as firms potentially expand margins through efficiency gains.

Read our 2026 global outlook

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.