Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

The great unravelling?

The initial bout of optimism around President Trump’s agenda for the US economy appears to be fading as uncertainty rises. Is this just a temporary soft patch or the beginning of a more serious growth deterioration?

One month on from our first assessment of President Trump’s agenda and our apprehension about the US economic outlook has increased. However, it is always the case that there is lots of uncertainty. As investors, we consider it our role to judge if the situation is more uncertain than usual.

So far markets have shown a relatively modest reaction to the policy changes from the new US administration and the consensus among economists is that the US is still set to enjoy a period of 2% growth, with no recession in sight. With a slowdown in immigration widely expected, this implies favourable per capita income growth.

Despite some unsettling headlines, we try to remind ourselves of the case for optimism. The US Federal Reserve appears to have pulled off a soft landing in the US economy, with inflation moderating and the economy in equilibrium alongside solid real income and profit growth.

The US appears to have unique advantages in energy, deep capital markets and technology. The business environment appears orientated towards de-regulation and tax cuts and there is big push to make government more efficient. Yet we worry there are several negative factors which will ultimately lead to a growth disappointment.

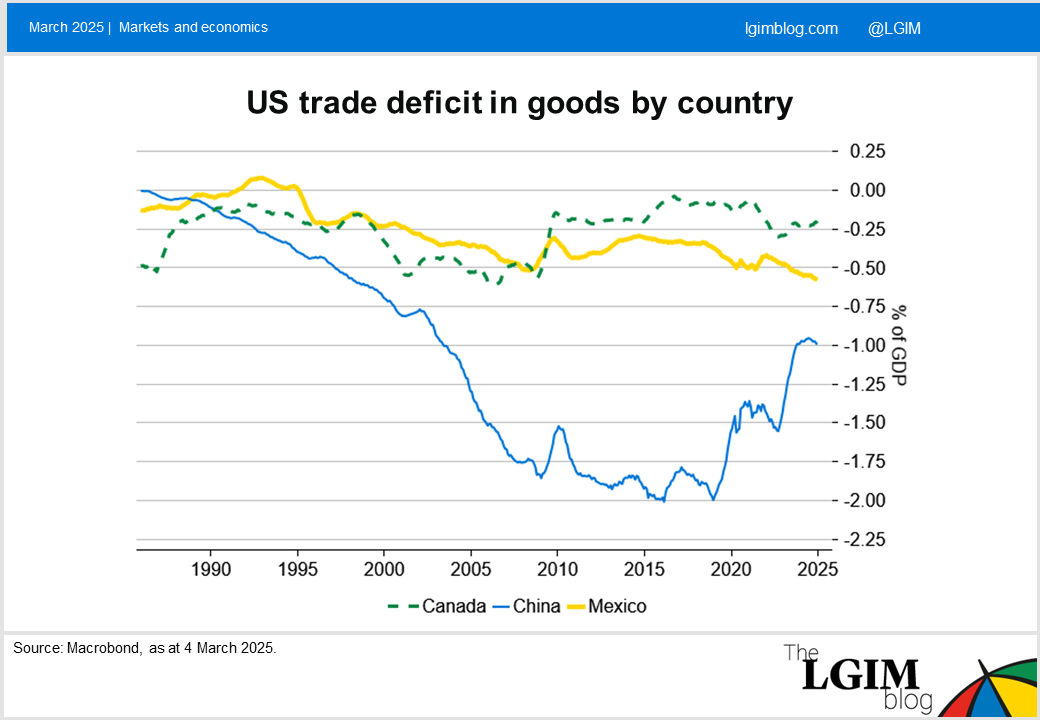

Tariffs

The biggest economic concern is tariffs and we have now seen 25% rates introduced on Mexico and Canada, though it is not clear how long these will last and if both countries can make progress on curbing fentanyl supplies into the US. The additional 10% on China seems more likely to persist. Aluminium and steel tariffs are scheduled for 12 March, while 2 April is setting up to be a crucial date to watch as President Trump has threatened broad reciprocal tariffs and tariffs on agriculture.

When economists measure the static cost from the direct impact of higher prices for the US consumer and retaliation on US exports, the impact appears manageable for the US (less so for Mexico and Canada). The complicating factor is the uncertainty around where tariffs will ultimately land. We believe this is likely to have a chilling effect on business investment. Tariffs could also potentially put upward pressure on an already overvalued US dollar, further undermining exports, though our conviction on this point is low considering the dollar has recently weakened as tariffs have gone up.

Retaliation to tariffs has begun, but the impact of geopolitical risk on growth is harder to assess. Increased defence spending in Europe even has the potential boost GDP. One tail risk we are monitoring is the potential for a broad boycott of US exports and brands.

Immigration

Immigration restraint will directly slow consumer spending and company earnings. Border encounters were already down sharply in recent months, but appear to have fallen to near zero since inauguration.

The risks to the consensus view on net immigration (which is a return to pre-pandemic rates) seem skewed to the downside in our view. Furthermore, while actual deportations might be constrained by a lack of resources, the threat appears to have risen. This could lead to more saving among existing illegal immigrants.

Cuts to government spending

Cuts to spending are proving more substantial than anticipated. At a minimum there will now be around 2m federal workers worried about job security. The function of government could be disrupted with unintended consequences.

Private contractors that rely on government contracts and appear to outnumber federal employees by more than two to one also face greater uncertainty. The uncertainty could also potentially impact private sector hiring exposed to contracts, grants and regulatory approval. So the overall impact on payrolls could be significant in the months ahead.

Benefits now appear more in scope than suggested during the election campaign. Food stamps appear likely to be frozen or cut. This hits those with a high marginal propensity to consume. There are also threats to cuts to Medicaid which could lead to more savings in anticipation of increasing out-of-pocket expenses. More generally reforms to healthcare could potentially lead to an investment pause in this sector while the uncertainty persists.

The extent to which parts of the Inflation Reduction Act get stripped back is unclear. But lots of the green energy investment will now be likely to be on hold or cancelled. Also, the ending of electric vehicle tax credit could negatively impact auto sales (as well as higher prices from tariffs).

Tax cuts

The potential offset to the negative news is the tax cuts, which could arrive later than the damage inflicted on the economy from the bad news. Second, the extent of any fresh stimulus is not clear. Congress could potentially insist on some deficit reduction in exchange for extending expiring tax cuts. Consensus seems to be leaning towards a net fiscal stimulus with some additional tax cuts and only modest overall spending restraint (with more spending for defence and border security and some cuts elsewhere).

Signposts

If these concerns materialise, we would expect the first signs to come from more than just a reversal in the boost to confidence surveys seen since the election. There has been some slippage during the first few weeks after inauguration, but the levels are still indicating steady growth. First quarter GDP might be weak, but this largely reflects a temporary jump in imports to get supplies ahead of potential tariffs which will likely unwind in the second quarter.

Over the next few months, we should receive greater clarity around where tariffs are likely to settle and the contours for fiscal policy. If confidence holds up and the labour market remains solid, our outlook may brighten. For now, however, downside risks dominate the investment landscape in our view.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.