Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Tariffs and trade – the world won’t wait

Current anxiety surrounding global trade is understandable. However, the medium-term picture could be brighter. While President Trump may put up tariffs, we believe the rest of the world is likely to move on to trade without the US. This matters for export-oriented stock indices.

We believe that investors shouldn't take President Trump's tariffs threats lightly. They are unlikely to be mere negotiating tools and could have a serious impact on economies with sufficient US exposure.

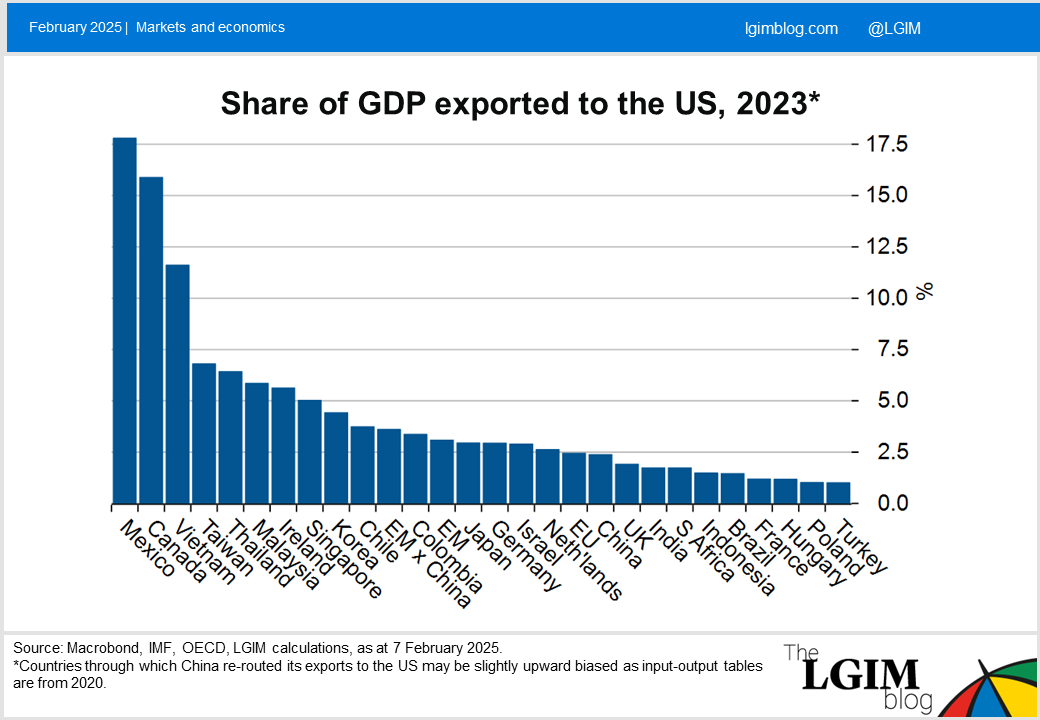

The first chart below shows which countries could be particularly vulnerable to the imposition of US tariffs. Top of the list are Mexico and Canada, followed by Vietnam and Taiwan. Further down the list are the EU and China, which export about 2.5% of their GDP directly to the US.[1]

This is of little comfort, as global growth and risk assets could well suffer in the short term if large economies start to retaliate.

Yet over the medium term the picture is less gloomy in our view as economies are likely to adjust to the new realities. Furthermore, we see plenty of potential opportunities.

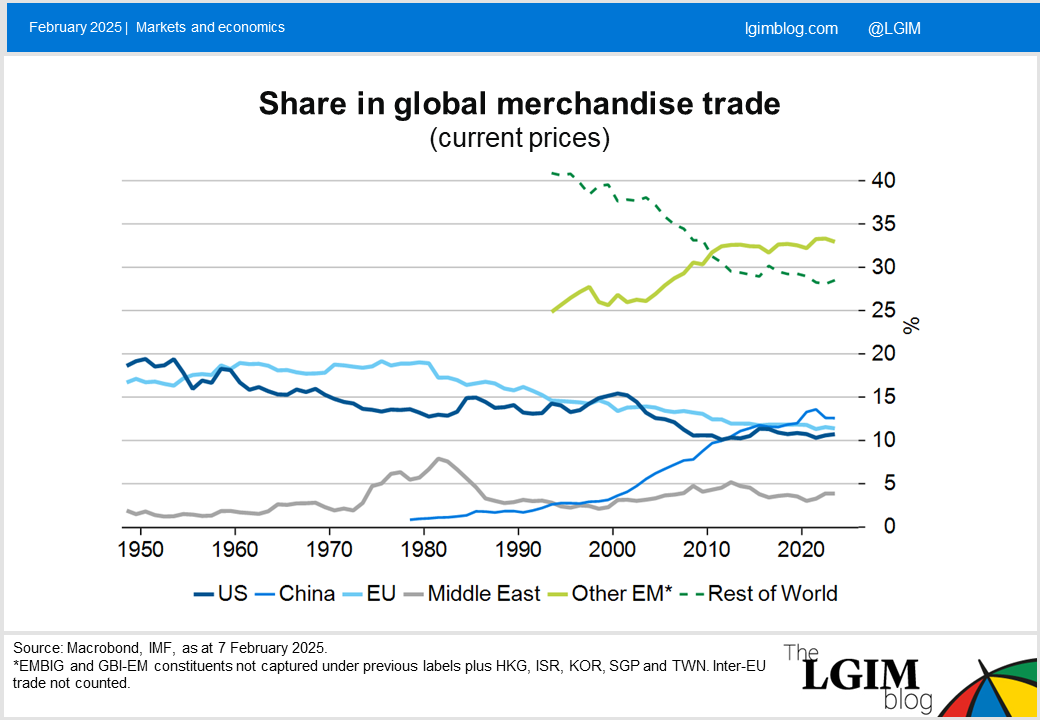

The US is the world’s largest economy, accounting for a quarter of global output, and it exerts even more influence over the global business cycle through the US dollar – the world’s reserve currency. However, the US accounts for just 10% of global merchandise trade, as it is a relatively closed economy. We believe this limits the potential impact of any tariffs over the medium term.

Necessity is the mother of invention

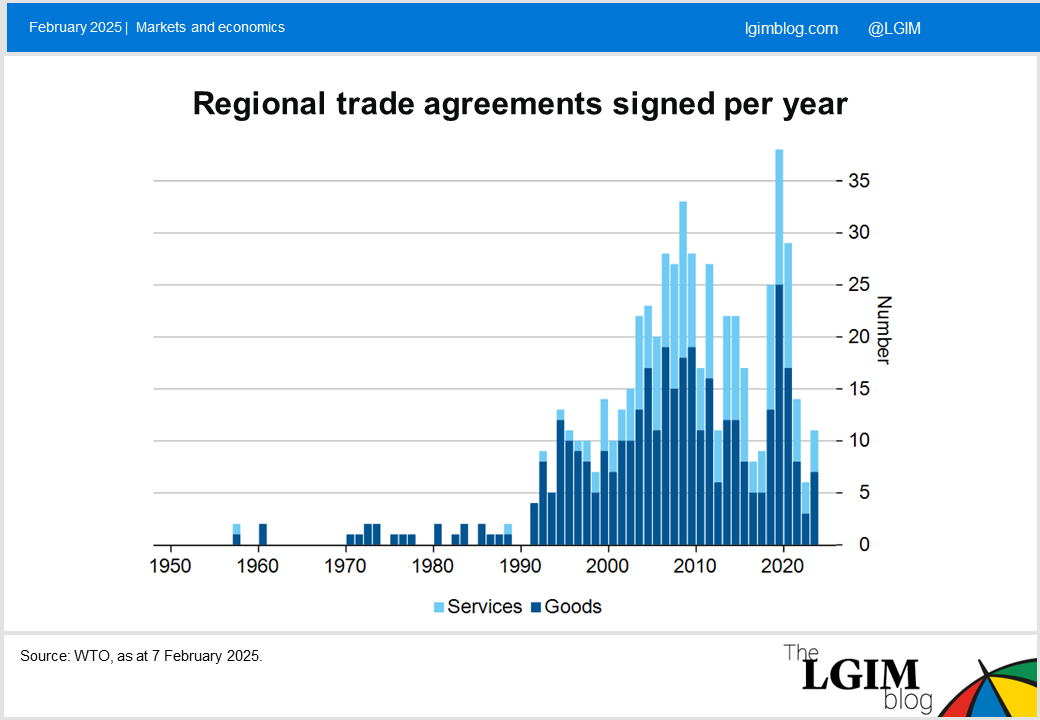

Whenever the US has turned more inward in the past, the rest of the world has tended to make extra efforts to trade among each other. In the last three years of President Trump’s first term, the world signed more regional trade agreements than ever before.

When the US pulled out of the Trans-Pacific Partnership in 2017, 11 countries went ahead nevertheless. When the US abandoned trade talks with Europe in 2018, the latter signed deals with Japan, Singapore and Vietnam and started talks with New Zealand and Chile (meanwhile completed). In 2020, 15 Asian countries created the Regional Comprehensive Economic Partnership and, in 2021, 54 countries formed the African Continental Free Trade Area.

The same is happening now. Since President Trump’s re-election in November, the EU has sealed a trade deal with Mercosur, the Latin American trade block, updated an agreement with Mexico and started talks with Malaysia. Further deals are expected with Australia, Indonesia, the Philippines and Thailand.

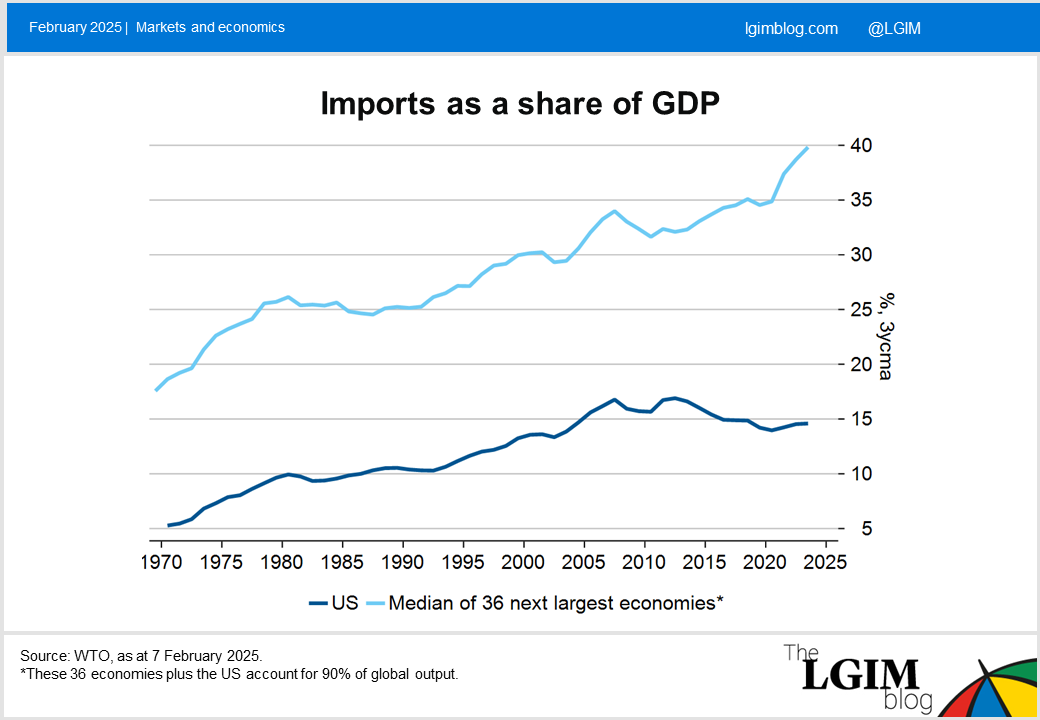

The world’s continued appetite for trade can also be seen in the final chart below. While US imports as a share of GDP have fallen over the past decade, they continued to rise for the rest of the world, gaining additional momentum in recent years. Almost three quarters of the top 35 economies saw their imports-to-GDP ratio rise since 2017, President Trump’s first year in power.

How does all this matter for investors?

Most countries increasingly continue to avail themselves of the advantages of trade: namely economies of scale, comparative advantage, knowledge transfer and innovation through competition. This means we believe their potential growth should hold up and possibly even accelerate despite a more-inward-looking US.

Second, we believe that equity indices that are particularly export-heavy, such as Germany’s DAX, Frances’ CAC40, Japan’s Nikkei, Korea’s KOSPI, Hong Kong’s HSCI or Taiwan’s TAIEX could remain attractive over the medium term, even if they experience some volatility in the short term.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

[1]If the US were to impose universal tariffs on exports via other countries, then intermediate goods would also be affected. However, apart from Hungary, India, Ireland, Israel and the UK, this is unlikely to make much of a difference in our view.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.