Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Solutions chart update: ForGilt me not

Gilts have been a recent standout performer in fixed income. Since peaking around the start of September, 30-year gilt yields extended their run lower through to the end of October. Could the UK Budget be the final piece of the puzzle?

What’s happened?

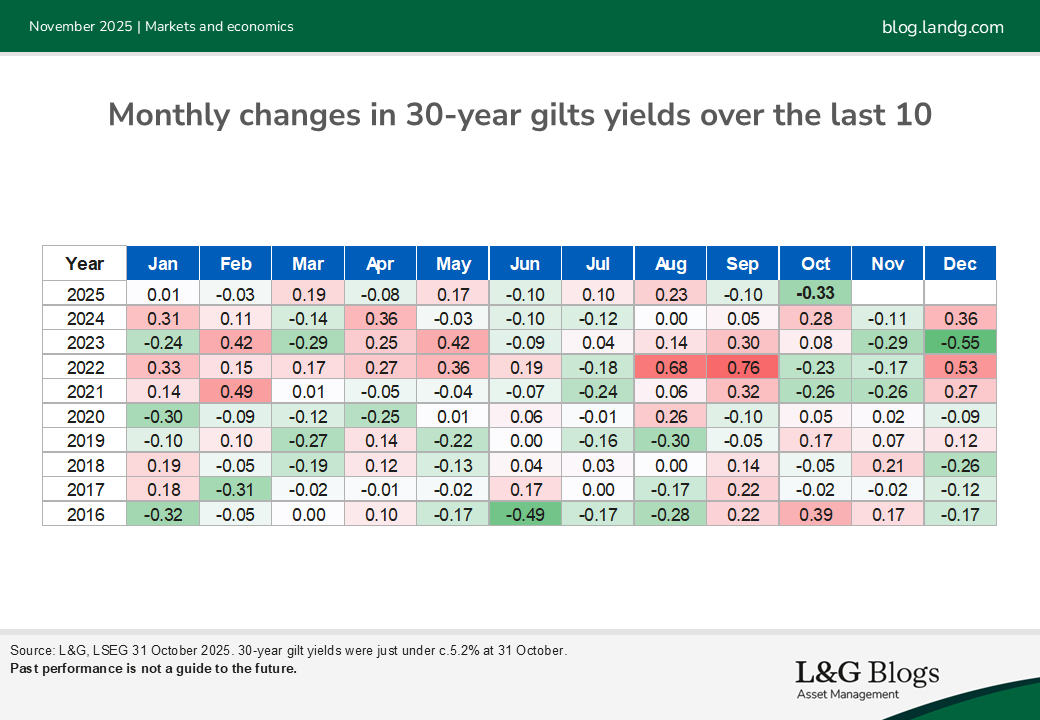

The heatmap shows monthly changes in 30-year gilts yields over the last 10 years:

- It has been over 12 months since 30-year gilt yields saw consecutive months of gains like September and October 2025.

- October 2025 ranks as the 3rd largest fall in 30-year gilt yields over this time period

- The recent performance is materially stronger than the US, Germany, France and Japan where yields ‘only’ fell by 10bps or less during October

Why?

We would point to a confluence of factors:

- Data and central banks. Recent inflation data, although high (3.8% CPI year-on-year for September) came in below expectations and is believed to have peaked, whilst the job market has been weaker. The UK is now pricing in rates at 3.4% in 12m time compared to 3.6% at the end of September. This contrasts to the US and Europe for example where the terminal rates are relatively unchanged.

- The Debt Management Office (DMO) has very successfully negotiated the 2025/26 remit to date and are well ahead of schedule having raised over 200bn of the 300bn remit. They have also continued to be sensitive to long-dated issuance (for example, cancelling a 2056s December auction in September).

- Improved sentiment. Even with the expectation around reduced productivity assumptions from the Office for Budge Responsibility (OBR) in the upcoming budget the gilt market has been relatively robust. There does appear to be a feeling that the government will not blithely increase debt at the Budget.

What could be next?

After a breathless October, gilt markets took stock towards the end of the month and look more rangebound for the time being (oscillating around c.5.2% at the time of writing). Clearly the approaching UK Budget is a major event for this market. How much advance credit has the Chancellor been given for more fiscally agreeable rhetoric? Could that unwind and more on the back were the Budget to be poorly received by investors?

On the other hand, what effect could a well-received Budget have? Furthermore, there is limited supply into year end and a potentially attractive 5%+ yield on 30-year gilts (still well above Europe and the US).

In our view, there is certainly a possibility for 30-year gilts to trade below 5%, which has occurred only once in 2025 and intra-day at that. Could the Budget usher in a longer period of stability?

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.