Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Skirting recession

The US administration has reversed course on its most aggressive use of tariffs, but some economic damage could still lie ahead.

The last few weeks have been a rollercoaster for markets and economic forecasts. The S&P500 is back to where it started the year, but forecasts for GDP remain significantly weaker. This is even after a slew of forecast upgrades from major sell-side banks following the surprise announcement on 12 May that both the US and China are to bring tariffs down by 115 percentage points and engage in trade negotiations. Recession forecasts have now been rescinded, though consensus still expects US growth to be less than 1% through this year.

The expected timing of interest rate cuts from the Fed has also been pushed out as without a recession, unemployment might only rise slowly, if at all. The US Federal Reserve will therefore need to focus on inflation, which we believe is still likely to rise uncomfortably above target as the remaining tariffs pass through.

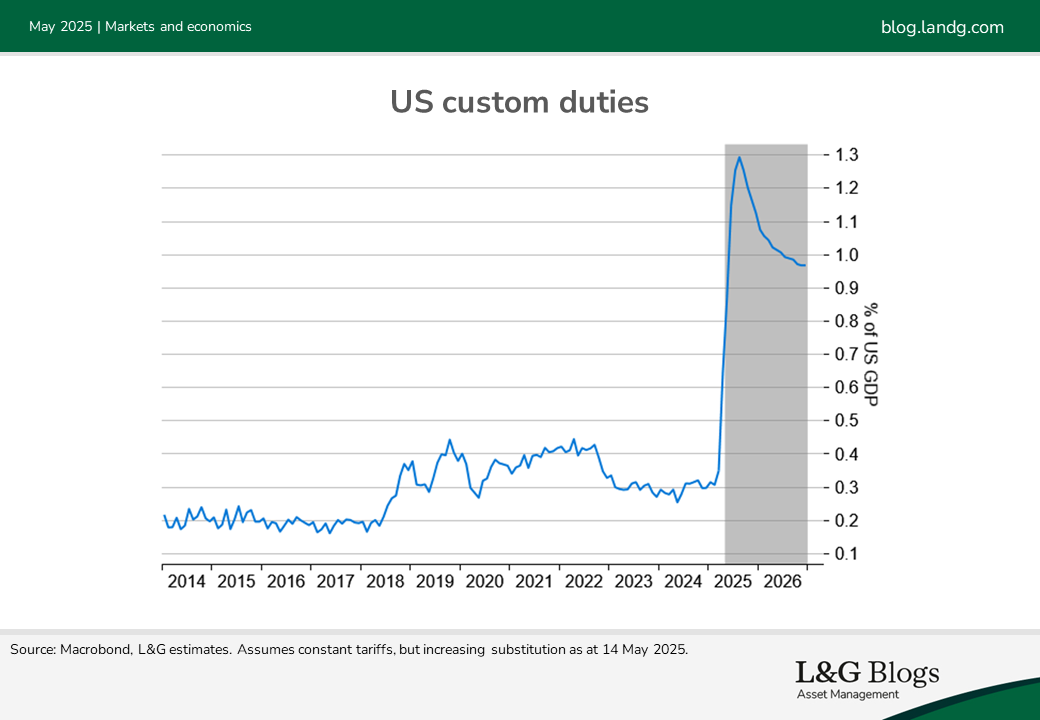

Equity and credit markets are relieved that a global trade war appears to have been averted, but prospects for more deals in the weeks ahead should not mask the unprecedented rise in US tariffs. The overall effective tariff rate is still set to increase to around 15%.

Some of the US sentiment surveys which are currently at recession levels might improve from here, but the impact of tariffs still lies ahead. Prices have yet to rise, judging by the April CPI release. Retailers seem content to run down inventories and wait and see where tariffs settle before changing their prices. There could also be some weaker consumption as payback for the front-running of purchases ahead of tariffs.

Additional growth drags

The recent focus has been on de-escalating trade tensions, but as discussed previously there are several factors weighing on growth prospects. The Department of Government Efficiency (DOGE) has gone out of the headlines, but has still caused some disruption and job insecurity even if the cuts are not as deep as touted. Immigration has ground to a near halt and the fear of deportation could induce a rise in precautionary saving. Student loan repayments have resumed and delinquency rates have spiked and will now impact credit scores. Tourism has also been adversely affected by tariffs and border treatment, with travel from Canada especially impacted.

Fiscal policy

While trade uncertainty has not gone away, attention for a while might shift towards fiscal policy. Some details are beginning to emerge, but discussions remain in flux. There appear to be some small additional personal tax cuts in the package, including the campaign pledges of no tax on tips and overtime. The big expense is making permanent the tax cuts due to expire at year end.

The reinstatement of 100% business expensing is a positive, but there is no room for additional corporate tax cuts. The new tax cuts seem front-loaded and set to expire after 4-5 years (to keep overall costs down). The payfors involve a large cut of the tax credits in the Inflation Reduction Act, but are scheduled to take longer to run off. There are also various proposals to reduce healthcare programs.

We await further spending cut details, but consensus seems to expect these will be resisted and the deficit will take the strain. Tariff revenues are not explicitly counted, but the potential for around 1% of GDP extra revenue will probably be in Congress’ mind, even if they can’t be relied on for 10-year budget scoring. Overall, we don’t expect significant progress to reduce the deficit which is running at 6-7% of GDP, but also we don’t envisage much net stimulus, especially considering the shifting mix of tax and spending could lead to unfavourable fiscal multipliers.

Risks still to the downside

The dialling back of trade tensions is clearly positive. But having swung from complacent in February to more alarmist in April, we worry that the consensus pendulum is now swinging back again to undue optimism. Uncertainty remains high even if off its peak and we still expect it to undermine business investment. The growth and inflation mix is deteriorating which constrains the Fed’s ability to respond to further shocks.

If Congress can pull off more fiscal support than we expect, without upsetting the bond market and rapid progress on trade deals gives confidence on where tariffs will settle, we could reduce our recession probability further. But for now, we see it around 50% versus the roughly 40% among betting markets and other economists.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.