Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

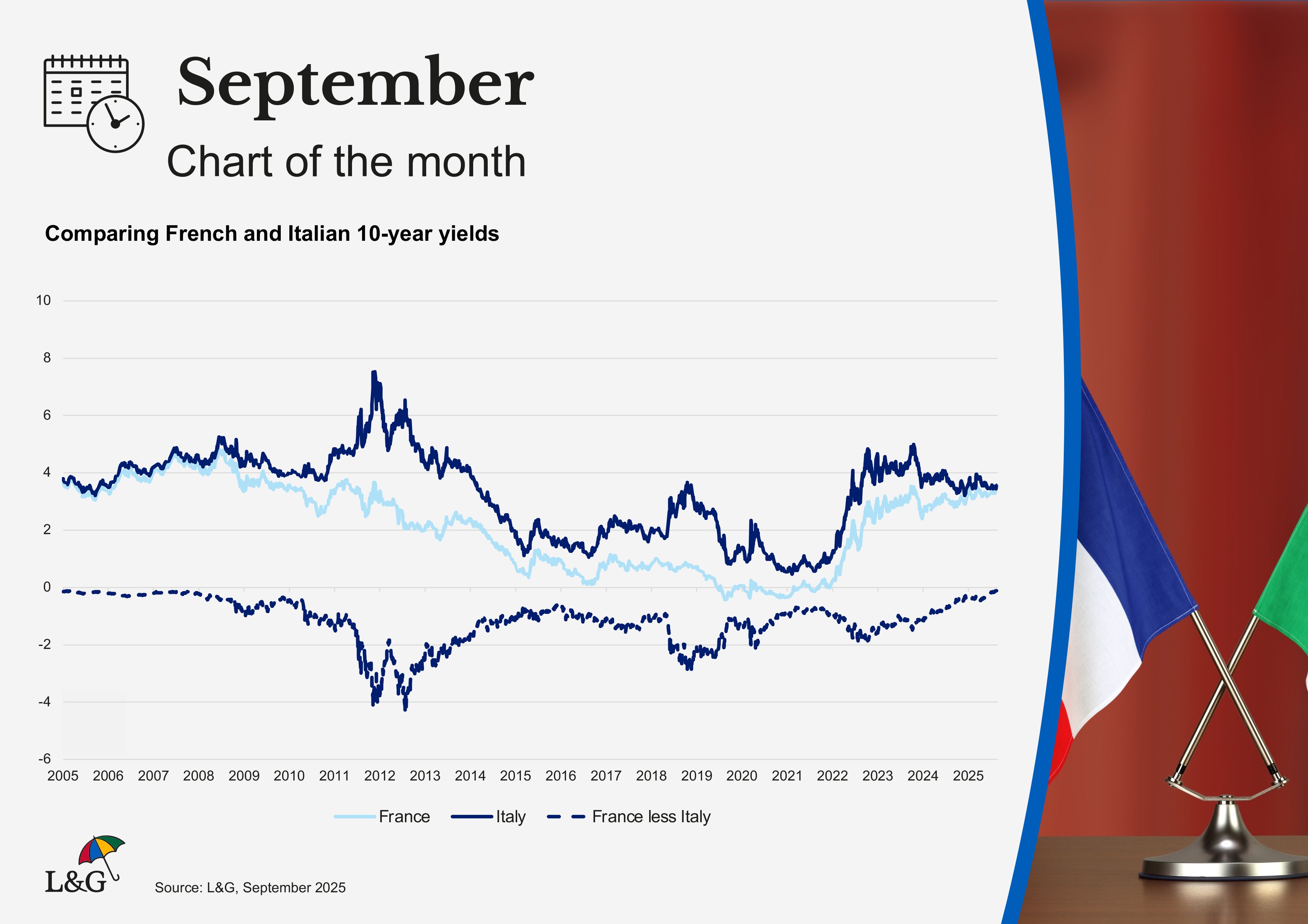

Chart of the month: French finances in focus

French bond spreads are widening as its political-risk timetable accelerates.

France has two related issues. It has a significant budget deficit and a minority (centrist) government, flanked by large shares of MPs on the far-left and far-right. In July, the centrist government proposed further aggressive budget cuts: including abolition of two public holidays, pension and benefit freezes, no indexation of tax thresholds, civil service cuts and higher health costs.

Needless to say, this isn’t popular. Mass protests “let’s block everything” (bloquons tout) are planned for 10 September. To get ahead of this, the prime minster announced an emergency recall of Parliament for 8 September (two weeks ahead of schedule) for a confidence vote on the government’s fiscal strategy (rather than precise measures).

Technicalities mean it will be hard for the government to win this confidence vote because abstentions do not help. A confidence vote held by the government requires a majority of votes cast. By contrast, a ‘no confidence’ (censure) vote called by the opposition requires a majority of Members of Parliament. This was also the case for eventually passing last year’s budget under special article 49.3. The budget was able to be passed because the opposition centre-left socialist party was able to abstain.

This time around, abstentions won’t help. Socialists will need to vote for the government. Their leader has already said support for the government is “inconceivable”. So France’s political risk timetable has accelerated. The general consensus was that the stricter draft budget would be negotiated down from October and a less aggressive budget would still satisfy the European Commission.

Moreover, there’s now a risk of new parliamentary elections as more than 12 months have passed since the previous ones. This wasn’t the case last December when prime minister Barnier lost a no-confidence vote. President Macron just appointed a new centrist prime minister. Consensus is split as to whether Macron will engage in another round of changes and appoint a new prime minister or call for fresh elections.

Latest polls show the far right gaining further ground. So it’s argued that new election threats can force concessions from the socialists. A new prime minister could lead to less aggressive fiscal tightening, but potentially still enough to satisfy the European Commission. That could therefore be a potentially attractive opportunity to buy French bonds. However, there is a significant tail risk from fresh elections, particularly given the far right has threatened to withdraw EU funding. Fundamentally, in our view, the rise of social media boosts extreme parties in elections.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.