Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

What does bond yield volatility mean for private credit?

The start of 2025 saw investors having to grapple with significant market volatility. For private credit, we see no reason to panic at this stage and find attractive opportunities in the short-dated space.

A volatile start to the year

When we wrote our 2025 private credit outlook back in December we took a more cautious view versus market consensus and highlighted the potential of macro uncertainty and implications of a higher-for-longer environment.

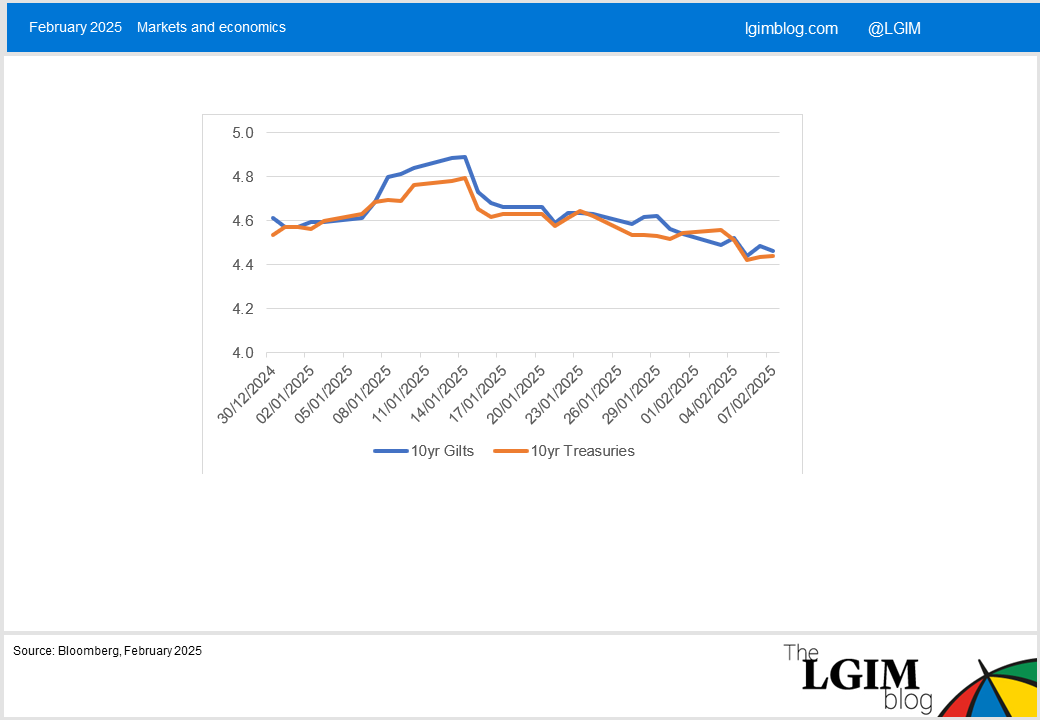

Market volatility over the first few weeks of 2025 certainly kept investors on their toes. We started with fears of stagflation which prompted 10-year treasury and gilt yields to rise by about 20-30bps in the first 10 days in January. This was then reversed following softer inflation data (see chart below). Equity markets had their own rollercoaster, initially caused by the release of DeepSeek’s latest model, and more recently by President Trump’s tariff announcements.

Credit spreads at the same time have been far more sanguine. Public investment-grade (IG) spreads are broadly unchanged YTD and the US high-yield spread has in fact fallen by 25bps (as at 30 January). Calm spreads suggest investors do not seem to be particularly concerned about the impact on credit fundamentals, in our view.

We expect more episodes of elevated volatility for the rest of the year but see no reason to panic yet for private credit. The asset class is generally in good health and there is so far no sign of pipeline or investor demand being impacted. If rates were to stay higher for longer, this would support yield on new issuance.

We have also been here before. Private credit markets continued to provide capital during the rates turmoil in October 2022 and October 2023. This led to significant growth and strong returns for the asset class over the last few years. Nevertheless, we still advocate caution. A key takeaway from rollercoaster over the last few weeks is that it is impossible to predict the timing and source of the next big downturn.

Short-dated investment grade private credit

If investors are worried about the impact of rate volatility, but want to take advantage of more attractive yields than public markets, where can they go? We think short-dated IG private credit is a potentially attractive way to boost the resilience of a private credit portfolio. Typically, these assets have maturities ranging from 3 to 36 months providing natural liquidity and thus potentially giving investors flexibility to reallocate capital in the future.

The investment universe is diverse, encompassing capital call facilities, NAV lending, working capital financing, bridging loans, and more. These more esoteric opportunities require specialised underwriting skills. As highlighted in our 2025 outlook, the core segment of private credit is becoming increasingly crowded. However, diversifying into alternative, short-dated financing may lead to more attractive risk-adjusted returns, in our view.

Investors may even end up looking beyond traditional short-duration fixed-income allocations, given the opportunities we see in this space. The super short-duration IG private credit market (typically less than 1 year maturity, modified duration below 0.1 year) is particularly interesting to us given the potential to insulate from rate volatility and macro uncertainty, which we expect to be a theme of the year. The strong credit quality gives an additional layer of protection.

Currently, spreads on super short-dated IG assets, range between 100-300bps above the risk-free rate, which represent very attractive premium for the credit risk.

Conclusion

In short, our view has not materially changed. We continue to believe that private credit is well-positioned. However, the recent market volatility underscores the importance of focusing on fundamentals, robust underwriting, and relative value.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.