Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

University-linked investments: Selectivity and opportunities within private markets

The UK Government’s legislative priorities highlight, in our view, the importance of working with universities to support spinouts, and the critical nature of infrastructure such as laboratories. Meanwhile, the Solvency framework and the Mansion House reforms aim to unlock higher net returns to long-term savers by making it more efficient to invest in productive assets.

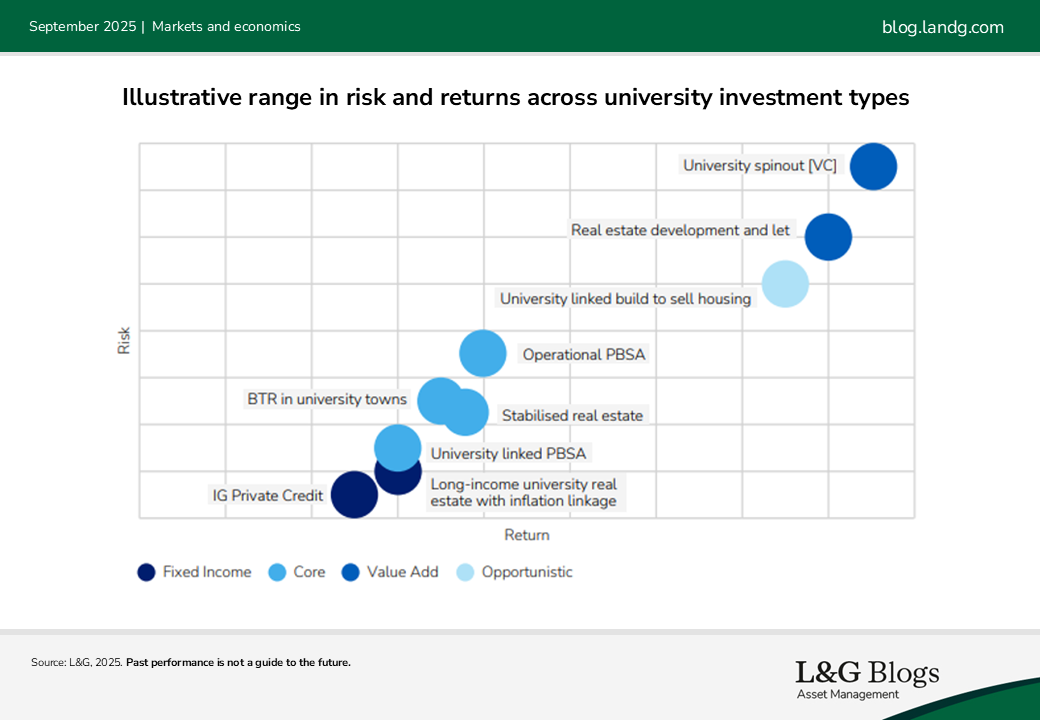

University-related investments can be considered a distinct private market investment theme, in our opinion, given they combine opportunities in real estate, credit and venture capital. But selectivity is becoming more critical. In 2024, universities that L&G classify as the ‘Global Elite’ saw international student acceptances grow by 10%. Those we define as ‘Trailing Institutions’ cluster saw a decline of 30%[1].

Meanwhile, our research also shows the tuition fee cap for UK domestic students has constrained finances. Adjusted for CPI inflation, a real-term decline of 26% and an average loss of £2,500 per domestic student per year can be demonstrated. So far, universities have been able to mitigate through their ability to charge international students more. However, we see this model being more fragile. Survey data on the measures universities are taking show that 49% have stopped delivering some courses and 18% have closed departments[2]. We expect to see more mergers.

For investors seeking exposure to university-linked assets, this requires greater selectivity but does not diminish potential performance. By our estimates, nominal target returns for university-linked investments range from 6% in lower-risk, secure income assets to 15+% in higher-risk assets such as development and venture capital. Equally weighted, we estimate a blended target return to be c.10%. This compares to long-term returns of 6.1% in real estate, 10% in infrastructure and a current yield of 5-7% in credit investment.

The different entry routes are:

Venture capital: As of January 2025, there were 1,337 active spinouts in the UK, of which 55% were seed stage and 30% were venture stage[3]. This has, in our view, created an increasingly attractive pipeline of later-stage scale-up companies that require funding. We believe the market is bifurcating between early-stage investment, funded by well capitalised university-linked investment platforms or VCs, and later-stage investment, largely coming from generalist institutional investors. However, funding challenges exist. Although such challenges are less acute at leading universities, we believe there is a need across all institutions for flexible and patient capital.

Direct real estate: PMA expects returns from student accommodation of around 8% over the next five years with attractive rental growth, notwithstanding localised risks around oversupply. Lab space performance is harder to quantify in the UK given opaque data but, in the US, analysts such as Green Street suggest an entry yield of a similar level to the broader market, following re-pricing, of around 5.9% and long-term rental growth in excess of 2%. For development returns, our own experience in developing teaching facilities and housing suggests achieved development returns of around 15-20% can be sought. Associated residential and office assets in university towns also show outperformance: In the UK, Cambridge’s office real estate has outperformed by more than 50%[4] and in the US, we can demonstrate clear outperformance of local apartment market returns in university-dominated cities of more than 5% annually.

Private credit: Universities are often attractive credit counterparties given implicit government support. They are frequent bond issuers in the public and private credit markets and tend to attract strong demand. University bonds are typically rated between AA and AA-, higher than average. Universities display strong rating stability. Over 75% of bonds have seen either no change or an upgrade to the credit rating since issuance. University bonds have also proved a good source of duration and long-term cashflows. The average maturity of current publicly traded university bonds is c.18 years[5].

Bringing together previously separate asset classes under the lens of one opportunity – universities – helps quantify the opportunity set and encourage coordinated investment approaches.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

[1] See L&G Blogs: Winner takes all in the UK higher education sector

[2] Universities UK, May 2025

[3] Spotlight on Spinouts, Beauhurst; Royal Academy of Engineering, April 2024

[4] Our analysis of MSCI data, Summer 2025

[5] Bloomberg data, Summer 2025

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.