Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

UK Commercial Property – moving up the gears

In this blog, we recap our recently released views on the UK’s commercial real estate market and assess how investors are currently viewing the sector.

We released our biannual views on the UK commercial real estate market last month. We see expected returns of between 7-8% that place comfortably within the range of historic realised returns. Additionally, previously challenged sectors like offices and retail are catching up with the strong performers of living and industrial. Yields look like fair value – and have done, in our view, since early 2024.

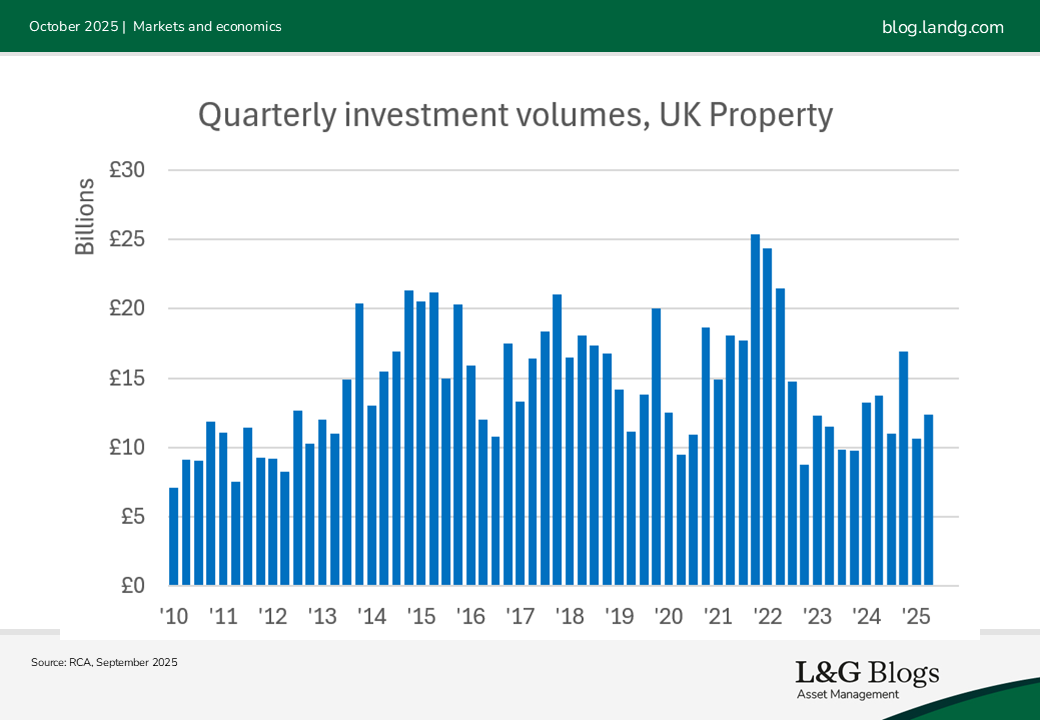

It is therefore surprising to us that investment transactions are still struggling to gain traction and flows into real estate funds remain lacklustre.

We believe there are four main reasons for this apparent dichotomy. Firstly, should investors agree with our view that yields are broadly where they should be based on market interest rates, then there may appear to be little urgency to transact. After all, if values are going to be the same in, say, six months, then there is no upswing to buy into.

Secondly, REITs have not had a good run, having shown much higher sensitivity to market interest rates than direct property. Investors who can choose between public and private markets may be tempted by the current discounts to NAV on offer from REITs.

Thirdly, yields on real estate debt still look attractive relative to direct real estate equity, given higher interest rates and decent margins; investors more interested in downside protection than upside gain may be tempted by the credit route.

Finally, the risk premium offered by direct real estate, although positive, is low compared to recent history and, given stability in yields and sticky interest rates, is not showing much sign of improving.

There is, however, important nuances to these high-level observations.

Taking each in turn: although pricing might not move sharply higher there has still been capital appreciation driven by rental growth. As a result, the current recovery may be slower than historic cyclical recoveries but there are reasonable capital gains on offer – and meanwhile delaying acquisition delays income receipts.

Secondly, over the medium term, history suggests REITs may offer more of an equity market return than a real estate one. And, relative to direct ownership or through funds, there is an opaquer pass through from value creation to investor return. Thirdly, while real estate debt remains compelling, simple yield assessments often over-simplify the comparison between a debt yield and real estate’s initial yield, where no growth is considered. When equivalent yields are used, the gap is tiny. Similarly, a squeezed risk premium is more of a problem when income growth is challenged – but forecasts suggest real terms rental value increases over the next five years.

We should also consider risks to forecasts and what else might influence flows. Upside macro forecast risks seem isolated to achieving non-inflationary growth. This is possible via productivity enhancements through AI, but also resolution of geopolitical conflict. Elsewhere, an expensive equity market has not yet led allocators to correct resultant underweight real estate positions. Persistence in equity pricing could change this. More important, in our view, are the potential implications from pension fund reform, the Mansion House accord, and LGPS consolidation. These could unlock greater capital flows into productive assets, of which real estate forms an important part.

We think the ‘2025 vintage’ offers direct investment managers an opportunity to acquire assets against limited competition at a compelling discount to 2022 pricing, an opportunity to pick assets and locations carefully at a time when sector allocation may not deliver the excess returns it has recently, and to drive value growth through asset management. This can create performance that other routes into real estate can’t offer – at a time when others may struggle to navigate the complexities of higher build costs and might not have the benefit of significant investment in occupier relations and the resultant income retention benefit.

Meanwhile direct real estate funds that can use REITs as a complement to long-term returns, as well a tool for short-term liquidity management when it is required, seem very well placed tactically.

So, although an unlevered 7-8% p.a. return – on average – may not be enough to provoke a stampede of investors, we believe these returns are good relative to history. The direct market offers routes to “move through the gears” to drive returns higher that may not be available to other routes into the sector.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

Past performance is not a guide to the future.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.