Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Carving a path in private markets

With 2026 well underway, we look at the key themes we see shaping private markets in the months ahead.

We recently sat down as a research team to talk over key theme within private markets as part of the L&G Talks Asset Management series.

Discussion centred on why we believe global diversification matters more than ever, how we think it’s possible to balance inflation resilience with a total‑return mindset, and the practical implications for real estate, infrastructure and private credit.

Below, we’ve summarised some of the key takeaways from the episode.

2025 in review and key themes for 2026

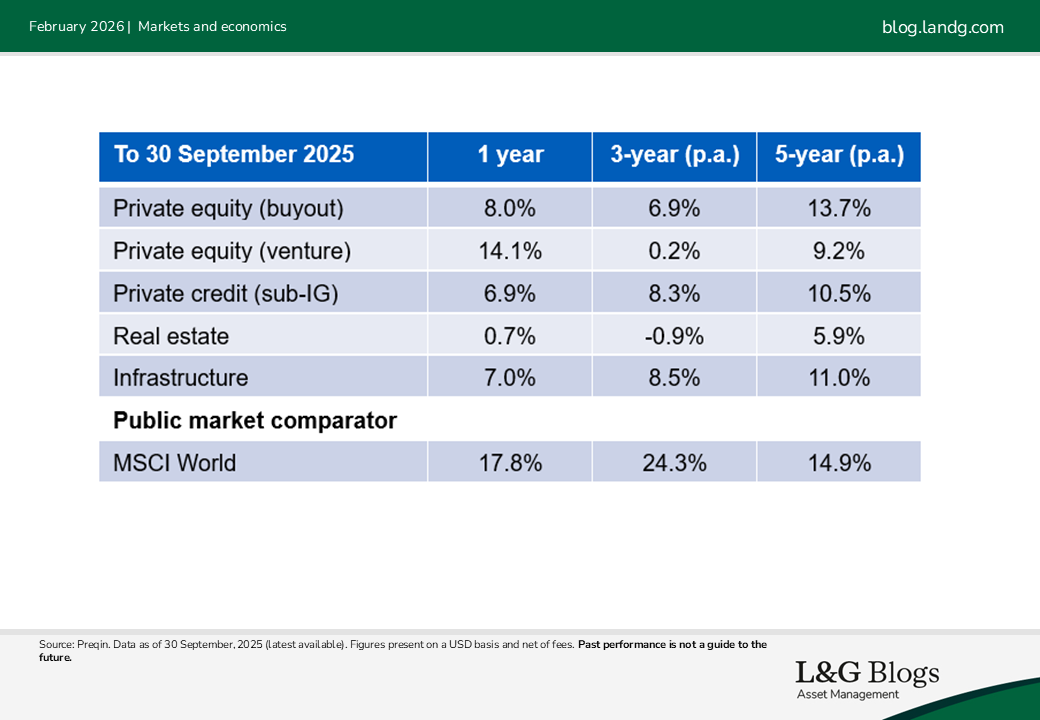

Private credit and infrastructure delivered another year of steady returns in 2025. Real estate valuations appeared to bottom out, meaning income was the main driver of return (see table below).

Meanwhile, global public equities performed strongly. From a total portfolio perspective, this would have reduced private market weightings for many asset owners, potentially setting up a more active year for allocations in 2026.

New capital allocations were mixed. Based on fund closes in 2025, it was a record year for infrastructure, modest improvement for real estate and weaker in private equity and credit.

Our three main themes for 2026 are as follows:

· Geopolitics: Amid ongoing uncertainty, investors may want to seek out geographical diversification particularly stable complements to the US.

· Inflation resilience: We believe sticky inflation underscores the benefits of assets with pricing power that may enable cashflows to rise in inflationary conditions.

· Total-return approach: As interest rates remain elevated, harvesting income yield alone may not be sufficient to deliver the performance most equity investors are wanting.

Real estate: Selection, location and the spectrum of income

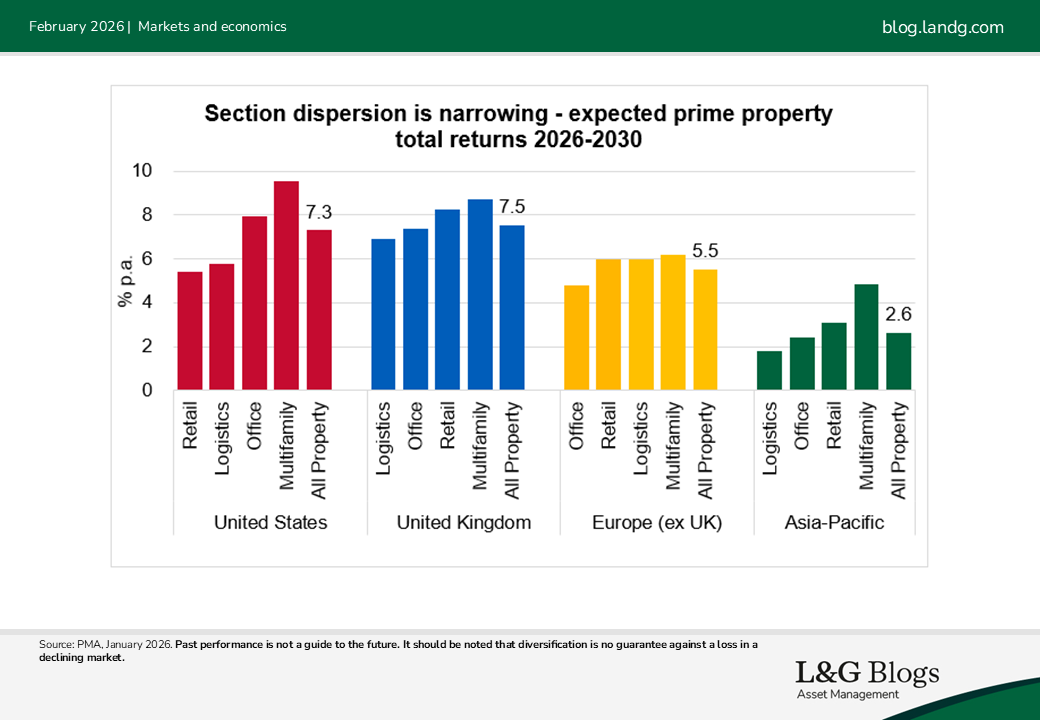

Long‑term expected returns look reasonable around 7% in the UK and US, a little lower in Europe. The dispersion between sectors is less pronounced than in the past decade, so a simple “own more XYZ sector” approach is unlikely to be a free lunch.

In such an environment, we believe the following approaches may help investors find alpha:

· Going beyond sector tilts. We see alpha increasingly coming from forensic segment and asset selection and location intelligence.

· Being deliberate about income style. At one end, long‑income assets with inflation‑linked leases may look more attractive post‑repricing. At the other, operational real estate – which swaps lease security for revenue exposure – could offer higher potential returns but also requires operating expertise.

· Targeting delivery gaps. Under‑development in recent years has created shortages of high‑quality stock. Where planning, cost and demand fundamentals align, we believe development and heavy refurbishment can be compelling sources of excess return.

Infrastructure: Digital demand meets the power challenge

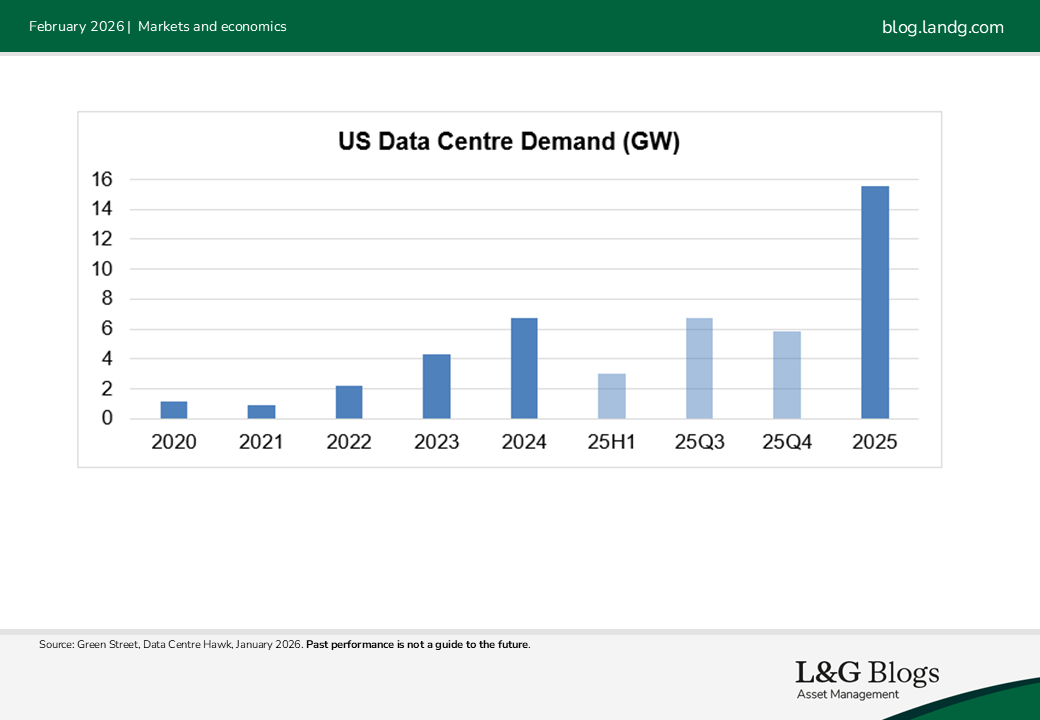

Big Tech capex continues to dominate the digital infrastructure market. Data centre demand continues to outpace constrained supply, underpinning strong rental growth and higher valuations for power‑rich capacity. We expect strong US growth to continue. While European demand growth is relatively more moderate, we see data sovereignty continuing to drive investment. Regions with abundant, stable, lower‑cost clean power, such as Iberia and the Nordics, are drawing mounting interest.

How might investors approach digital infrastructure?

· Valuation discipline. Balancing what’s paid for live, operational capacity versus future cashflows from data centres under construction.

· Backing power‑secure platforms. Time-to-power is the biggest barrier to new developments, meaning investors may wish to prioritise sites and partners with firm, scalable grid access.

· Diversifying within digital infrastructure. This may be achieved by combining exposure across data centres, backbone fibre and towers.

· Seeking synergistic AI infrastructure partnerships. Choosing partners for data centre growth who can create cost synergies across the vertical AI infrastructure stack.

Private credit: Resilient IG and nuanced sub-IG

2025 was a record year for IG private credit issuance, led by infrastructure and utilities. Spreads are tight, but higher base rates keep all‑in yields attractive, in our opinion, relative to history. Credit quality has also been resilient. We retain high conviction here for 2026.

In sub investment‑grade (sub-IG) credit, the high‑profile First Brands* bankruptcy made headlines in late-2025, prompting a healthy re‑examination of portfolio credit quality and underwriting standards. Activity slowed in Q4, but we see no evidence of systemic stress to date.

Defaults remained relatively low. Returns moderated (c. 9.5% in 2025 vs c.11% in 2024) mainly due to the rates/spread backdrop rather than loss severity.

What are the key considerations for sub-IG in 2026?

· Higher-for-longer: Elevated rates support investor returns but may strain highly levered borrowers, especially the 2021 vintage that is due to refinance.

· Uncertainty in AI exposure: A large proportion of direct lending borrowers are in technology or tech‑adjacent sectors. AI will create winners and losers. We believe it’s important to focus on managers with sector depth, proactive surveillance and credible workout capabilities.

Final thoughts

2026 is shaping up to be an active and complex year. We believe that focus on global diversification, pricing power and alpha generation are the key to resilience and outperformance.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecast will come to pass.

It should be noted that diversification is no guarantee against a loss in a declining market.

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.