Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

On a string: navigating the yo-yo of EU–US trade policy

After months of speculation, the EU–US trade agreement has finally been reached. However, questions remain about its longer-term consequences for the global economy.

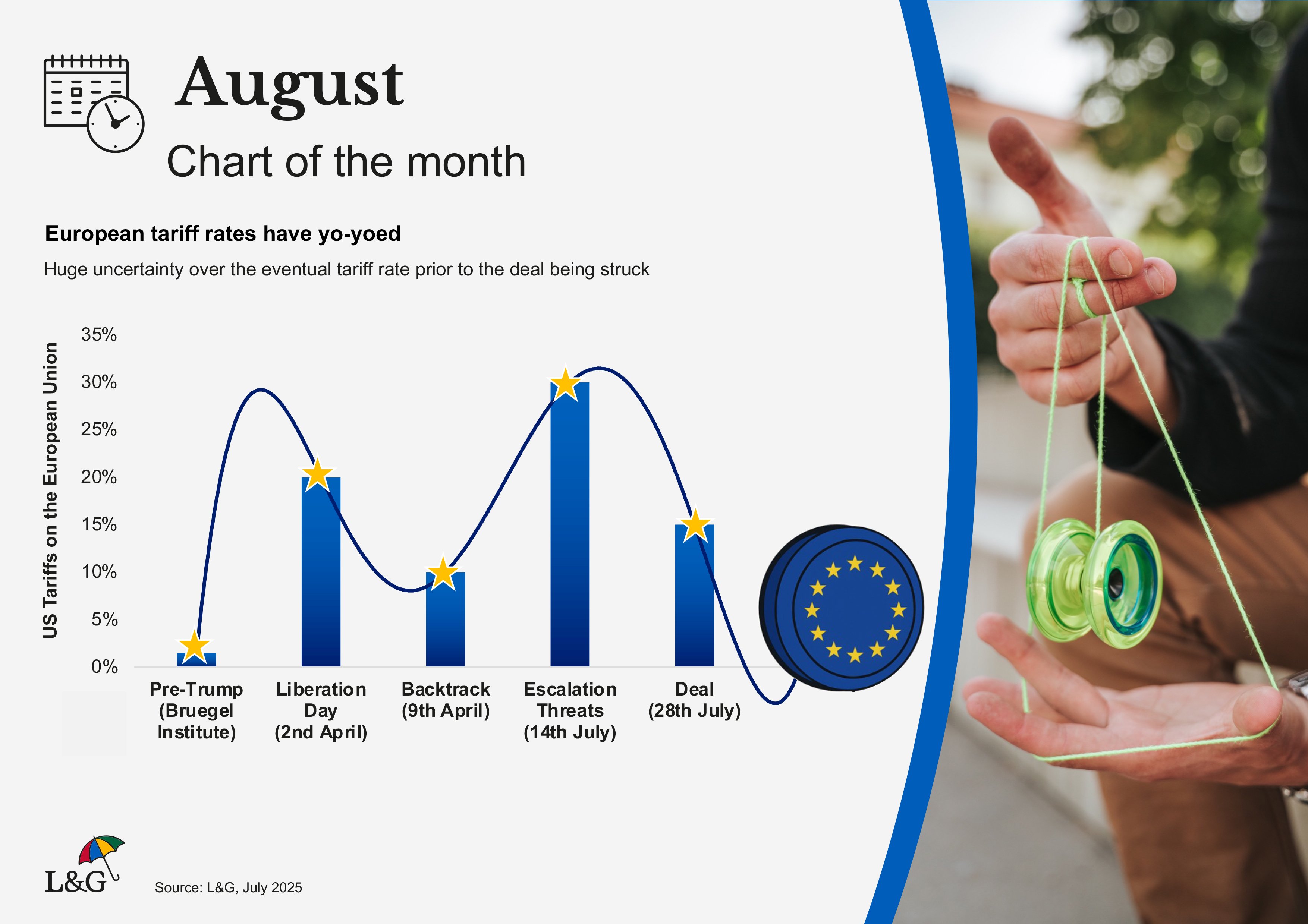

Despite the smiling press conferences, the ‘biggest deal ever made’ was far from straightforward. The speculated tariff rate has swung back and forth over recent months, leaving investors in a state of limbo. From optimistic whispers of 10% to open threats of 30%, the final figure of 15% offers some short-term relief but major questions about the long-term implications remain.

The political noise surrounding the EU–US trade negotiations was far from empty rhetoric. The Trump administration’s assertive tactics appear to have delivered results. The EU’s concessions, including the agreed tariff and substantial commitments on energy and defence procurement, reflect a pragmatic decision to avoid a more damaging outcome. However, it is difficult to frame this as a victory for Europe. The agreement introduces economic frictions that are likely to undermine efficiency on both sides of the Atlantic.

For investors, we believe the short-term outlook has improved. The removal of the immediate uncertainty, alongside last week’s agreement with Japan and ongoing negotiations with China, is providing greater clarity around the United States’ relationships with its major trading partners. Equity markets have recovered from their April jitters, and the target of 1% growth in the United States for the second half of the year now appears more achievable.

Nonetheless, the deal carries clear costs. Tariffs are likely to result in higher prices for US consumers, particularly in sectors that depend heavily on imports. Whether this leads to broader inflationary pressure remains to be seen. However, the recent easing in financial conditions may help cushion the impact on overall growth. As for the longer-term effects of the uncertainty shock, these remain largely unknown and could take time to fully emerge.

In Europe, the situation is more complex. The continent has avoided the worst-case scenario, and second-quarter GDP data has exceeded expectations. However, the competitive shock from US tariffs, especially in the automotive sector, remains a concern. Similar pressures on Japan and Korea offer some mitigation, but the rapid appreciation of the euro presents an additional challenge for European exporters.

So, what does this mean for investors? In the short term, the fog has lifted. Markets can now factor in a known tariff rate, and the risk of retaliatory escalation appears low.

Looking further ahead, uncertainty persists. The success of recent trade deals, achieved through aggressive tactics, may encourage the US administration to adopt similar approaches in other areas. While the EU has avoided a crisis, deeper questions around competitiveness, political stability and strategic autonomy remain unresolved.

In summary, the worst has been avoided, but the story is far from over. Trade policy, and geo-politics more broadly, continue to be difficult to predict. In our view, maintaining a well-diversified[1] portfolio, spreading risk across asset classes, regions and sectors, remains the most sensible approach for long-term investors.

[1] It should be noted that diversification is no guarantee against a loss in a declining market.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.