Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Is AI the answer?

While scepticism runs high, there’s potential for AI to have far bigger impact on the economy and markets than historical parallels suggest.

The following is an excerpt from our 2026 global outlook

AI is the topic du jour, with concerns about bubble risk dominating headlines. Yet while AI-scepticism runs high, there’s been a lot less focus on the implications should the technology deliver.

Historical parallels suggest a modest productivity boost translating into 30-50 basis points of gross domestic product (GDP) uplift for a decade, before the economy reverts to trend. But AI’s potentially universal application and ‘agentic’ ability to replicate human output hint at a far bigger impact.

Long-term economic implications

If AI-powered computers can take on a wider set of tasks, demographic burdens in rich countries could lighten through automation in sectors like elderly care. AI could also reshape the debt sustainability profile for rich countries. If AI powers a run of growth and tax revenues similar to the stellar run of technology-enhanced global growth that substantially lightened the fiscal burden in the 1990s, today’s fiscal anxieties could ease.

Meanwhile, big tech’s push to build massive data centres could balkanise AI infrastructure, with global powers like the US and China capturing disproportionate benefits, even as AI applications could simultaneously democratise growth in more fiscally constrained regions.

With regards to the labour market, in typical capex cycles, job shedding is delayed until recessions force firms to realise productivity gains. Yet that may not be the case with AI, as it rivals humans in an increasingly larger share of tasks. The cadence of labour market effects from AI may catch many by surprise, with the potential risk that AI increasingly weighs on white-collar jobs even as productivity rises.

In the US, the labour market already looks fragile; companies have paused hiring given tariff uncertainty while anticipating AI productivity gains to come. A move to shed labour outright could squeeze median and youth consumers. Typically, such a scenario would impact growth and might lead to a recession. Yet if AI is delivering productivity gains and driving an investment capex boom, then GDP might remain near trend even as the unemployment rate rises – a very unusual scenario.

How markets could react to this scenario is tricky to predict. If median-consumer weakness drives disinflation and unemployment rises while growth stays near trend, the Federal Reserve could cut aggressively. Lower rates may not save jobs but could be risk-positive for markets.

Not a bubble but a sentiment surge

We believe two distinct concerns – that ‘hyperscalers’ may be overvalued and that AI may fail to deliver real productivity gains – often get conflated in the current debate about the technology. While the jury is still out on the long-term economic implications of AI, we believe bubble concerns about current valuations are overblown. Those concerns centre around the belief that hyperscaler valuations look so stretched that it’s difficult to see how the sector can generate the required rate of returns to justify its massive capex.

Yet hypserscalers’ huge stock gains over the last three years have come with a doubling of EBITDA and steady margins, not just multiple expansion. Nvidia* – a key enabler of AI – has seen its price-to-earnings (P/E) multiple compress from 39x to 29x, even as its total shareholder return soared by 998%, driven entirely by earnings growth rather than multiple expansion.[1]

If we aren’t in a bubble on current valuations, and today’s use cases support the current level of spending, it’s worth considering whether we are in a sentiment bubble. Nvidia’s* CEO, Jensen Huang, speculated in September that global AI infrastructure spending may reach $3-4 trillion per annum by the end of the decade. This scale of spending is many magnitudes above what even the most bullish analysts are forecasting.

Amazon’s* Jeff Bezos has called the AI investment boom an “industrial bubble,” not a financial one. All AI ideas are getting funded – good and bad. If the tech is real, then most of the value will accrue to the implementers, not the enablers.

As such, from a macroeconomic perspective, bad AI investments might be an acceptable cost to bear for the sake of fast innovation that could revolutionise the American economy. In addition, the AI spending boom does not look aggressive when compared to other technological revolutions. That said, some hyperscalers seem to be investing with the rationale that falling behind the AI-curve will present existential risk to their companies. That dynamic likely increases the risk of wasteful spending.

We do think AI has the potential to change businesses the way the Internet did, but at a much faster rate. Its impact will be broad and deep, with businesses previously considered to have impeachable economic moats brought under pressure. Numerous blue-chip companies could have their ‘Kodak moment’ simultaneously.

The revolution will be funded by debt

The AI investment boom is being is clearly being debt-funded. We see 2025 as a likely inflection point, where companies are transitioning from self-financing to more reliance on debt markets, spreading AI-related risks more broadly across the economy.

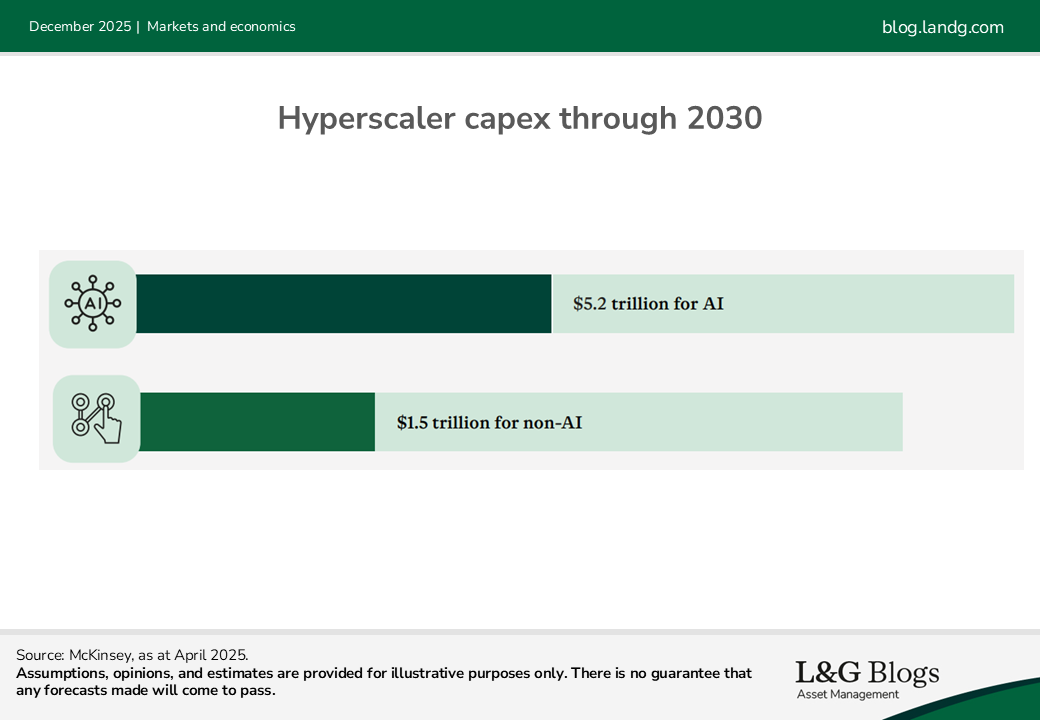

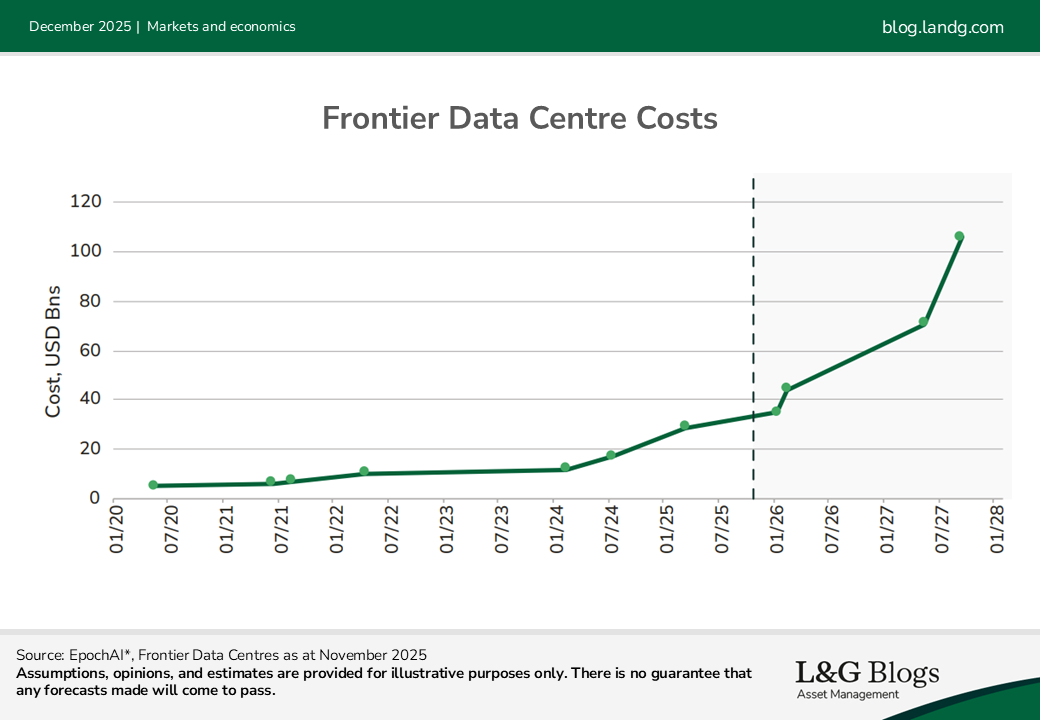

Everyone is now asking how much AI-related debt issuance is on the horizon after deals by Meta* ($30 billion), Oracle* ($18 billion), Google* ($24 billion), according to Bloomberg as at November, and a handful of high-yield-rated data centre issuers recently.* A recent McKinsey* report sees nearly $7 trillion of hyperscaler capex through 2030 ($5.2 trillion for AI and $1.5 trillion for non-AI). Morgan Stanley* estimates $3 trillion over three years, while EpochAI* estimates that the cost of the most expensive data centre could reach $100 billion by 2027. Even with hyperscalers still funding a healthy portion from their free cash flow, the implication is $500-800 billion of additional debt annually – or $2-3 trillion cumulatively by 2030.

Here’s one way to frame the debt financing requirement. Over the past decade, the US non-Treasury bond markets grew $1.5 trillion annually, according to Bloomberg* data as at November. Adding $500-800 billion would boost net supply by 30-50%, our calculations indicate, pushing the total above $2 trillion for the first time and setting a record for the largest year-over-year percentage increase going back a decade.

A sub-plot to the supply story is the debate around which bond markets will see the most AI-issuance. To date, data centres have mostly been financed in securitized and private markets as off-balance sheet/limited-recourse/project-style financing. But the financing needs are now too big to bypass the greater demand available in public markets, as the recent surge in unsecured issuance from Meta*, Google* and Oracle* illustrates. Indeed, there has been an increase in quasi-private transactions where large financing deals begin life in the private market and then get registered and marketed to public investors before pricing and distribution.

The rising capital intensity of AI infrastructure could accelerate public-private hybrid financing models. In a world where AI does drive significant growth, venture capital may see outsized gains, while enabling infrastructure – especially data centres – may command even higher valuations in private markets.

In this scenario, leverage in AI infrastructure may amplify returns rather than stress credit markets. However, a balanced view needs to be taken in times of uncertainty. With private markets today offering entry points across the risk-return spectrum, selecting investments that offer AI exposure and retain value in diverse exit scenarios becomes the challenge.

History often rhymes

Will AI echo Moore’s Law, the dot-com boom, the gold rush or the railroad era? Perhaps a little of each. What is certain, in our view, is investor uncertainty and the need for diversification. The next decade will reveal whether the current boom is a bubble, a revolution or something in between.

In the meantime, while we are certainly on the lookout for AI disruption to the economy and markets, our base case for 2026 is that AI-driven capex and productivity gains continue to drive economic momentum, corporate profits stay resilient and companies refrain from shedding labour for now, in line with historical productivity booms where labour shedding comes later.

Read our 2026 global outlook

It should be noted that diversification is no guarantee against a loss in a declining market.

* For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

[1] Source for hyperscaler and Nvidia metrics: Bloomberg as at November.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.