Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Harsh port, harsher storm: EM rates in 2022

Tough monetary policies have prevented EM crises this year, but easing even as the global economy faces recession is not on the cards.

It has been a turbulent year for most global assets. The hits from inflation, the Ukraine war and a messy transition to tight monetary policies worldwide have wrought significant pain on many financial assets.

Usually, monetary tightening and pain in developed market (DM) assets is reflected, like a grotesque mirror, in crisis and meltdown across emerging market (EM) assets. But not so this time.

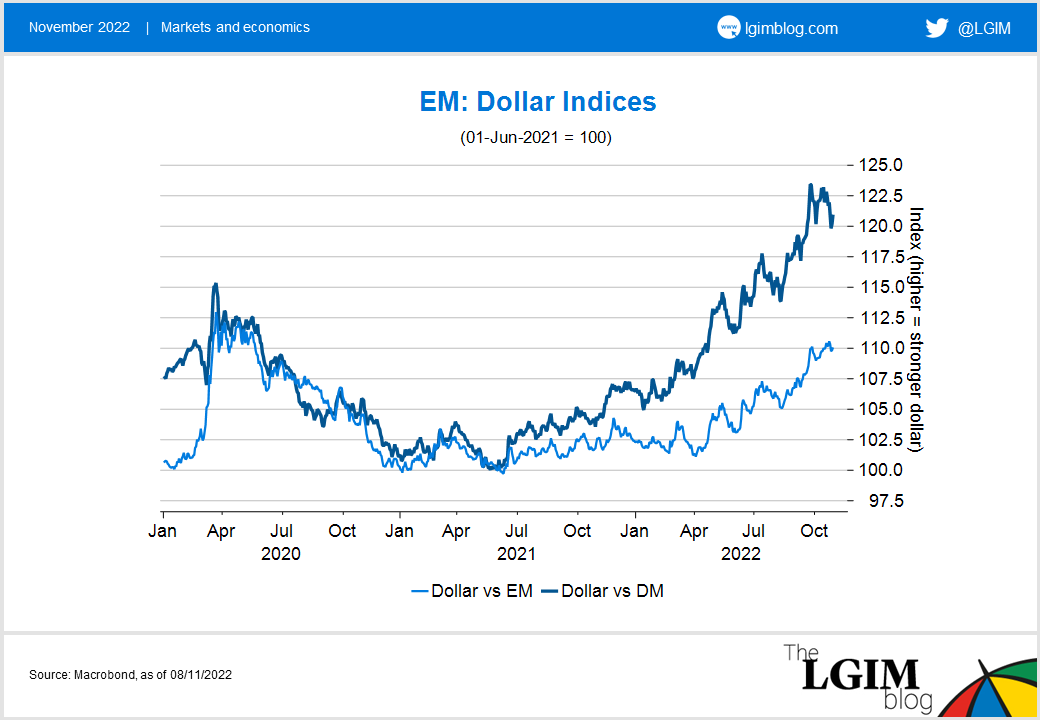

Far from following their usual script of cracking up when DMs go through a tightening cycle, EMs have so far performed well. In currency markets, EM currencies have proved more resilient than their DM counterparts in the face of a renewed round of dollar strength.

Dancin’ on a rates ceiling

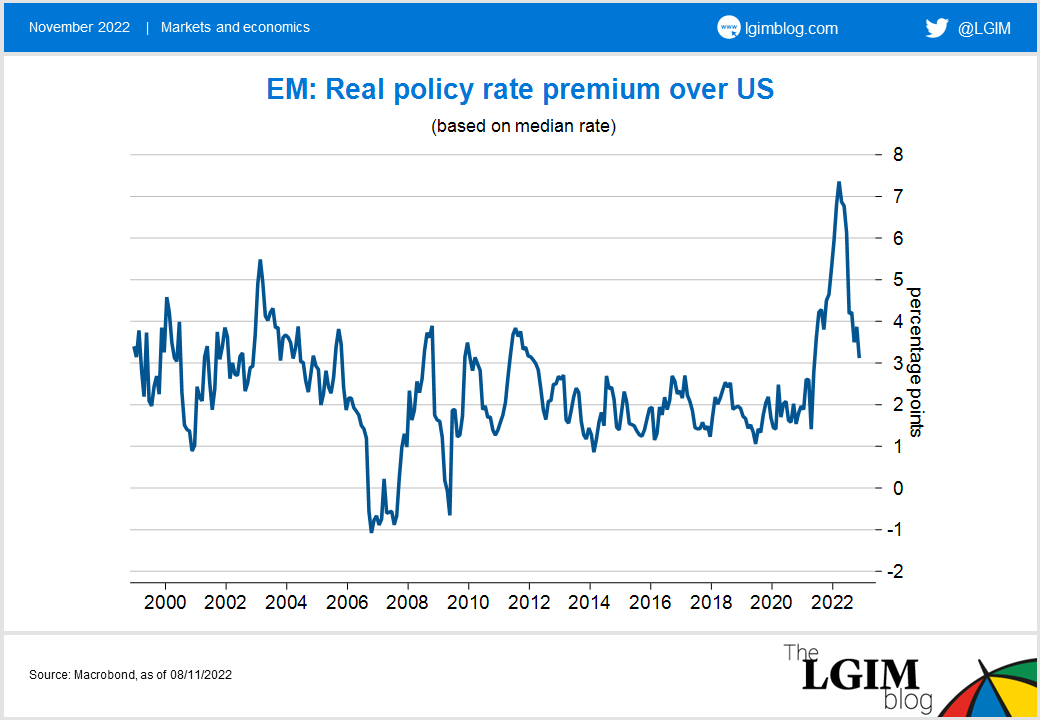

Why have EMs proved safer for investors than their supposedly better-run peers in DMs? One reason is robust monetary policy. EMs started their hiking cycles in the latter half of 2021, a time when most DM commentary was focused on ‘team transitory’ versus ‘team permanent’.

Against the Federal Reserve (Fed), EMs built up substantial premia in real rates throughout much of last year. Led largely by Latin America and later Asia Pacific central banks, policymakers across EMs acted early and decisively to control inflation and stabilise their currencies through both rate hikes and currency interventions.

These policies have worked well so far: inflation in Brazil (the most proactive of the EM central banks) has fallen sharply since June and no major EM has fallen into crisis, despite concerted rate hikes from the Fed.

Deficits ignored

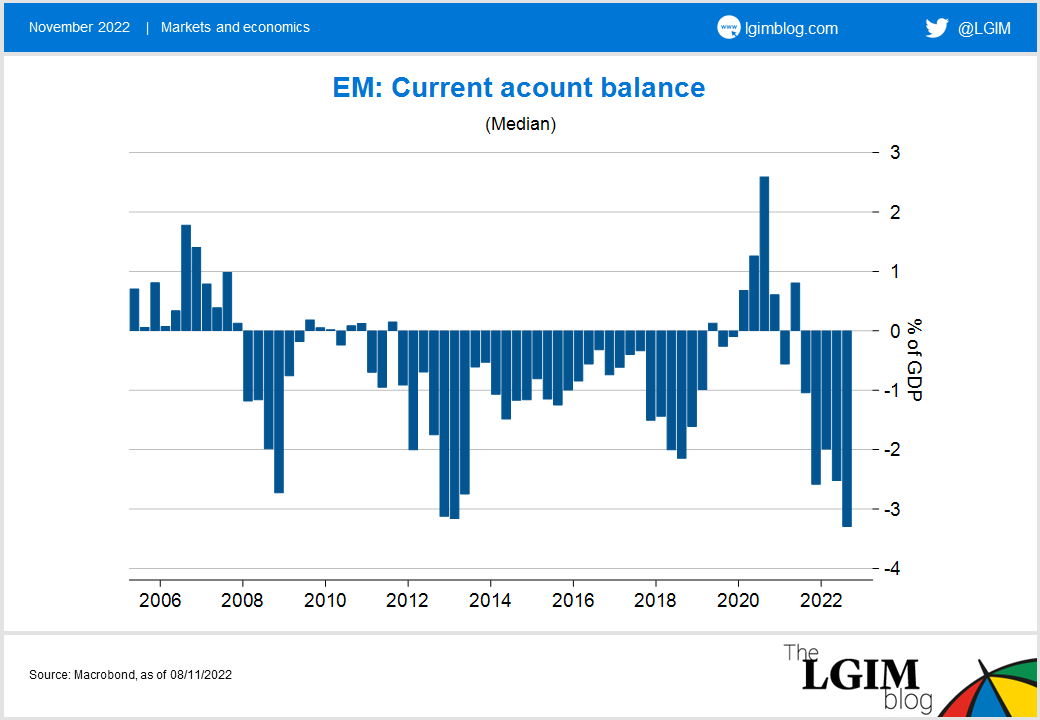

The high real rates buffer has also masked external vulnerabilities, which have gradually swelled since spring. Gas shocks, and the global prices for both oil and food have all contributed to this external pressure. Though many EMs are commodity exporters, only two major EMs (Colombia and Russia) have experienced their terms of trade improve over the past year.

Consequently, the median EM current account is now in a deficit of around 3% of GDP, similar to the levels of stress seen in previous episodes of EM panic in 2008 and 2013.

Bread today… no jam tomorrow

How long can protection against crisis last? Since the Fed began its concerted monetary tightening efforts earlier this year, the real rates premium has fallen significantly, raising the risks from external imbalances. Can EMs withstand this renewed pressure?

Most EM current account deficits do not keep us up at night.

Weakness is concentrated either in Eastern Europe, hit by the Russian energy shock, or in Latin America, where monetary tightening has been most hawkish. Provided monetary policies continue to be tight, these external imbalances should be manageable.

But concern around current account deficits will prevent any rapid easing, even as the global economy faces recession. If EMs want to retain the safe-haven reputations they have earned since 2021, they will offer little reprieve to domestic economies hit by shrinking external demand and foreign investment.

We judge this rates pressure will keep returns in EM equities subdued as activity is hit by hawkish policy. Nevertheless, as the Fed eventually lowers policy rates, EMs will again offer attractive opportunities for rate and currency trades as their inflation moderates and real yields remain elevated compared with the US.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.