Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Friendshoring: putting money where your mouth is

Evidence for friendshoring is even stronger in investment flows than in goods trade.

In this series of articles, we explore the evidence for a US-led trend of friend-shoring away from China and towards other major emerging markets (EMs).

In the first blog, we looked at the friendshoring trend reflected in global goods trade.

Here, we examine the evidence for friend-shoring as seen in flows of foreign direct investment (FDI) between countries. While patchier data diminishes our sample, we can nonetheless form a general view of FDI flows.

FDI flows: the ties that bind

Since friendshoring’s emergence as an investment theme after COVID-19, a battery of announcements from major firms focused attention on Mexico, Vietnam and India. Mentions of ‘friendshoring’ on S&P500 earnings calls jumped three-fold during Q1 2023 alone. This cheers Washington, but markets have watched carefully – could this be hot air?

The balance of FDI holdings among our sample of countries suggests not. Looking at the balance of FDI holdings from the US and China in recipient countries, the US has expanded its lead, particularly in allied countries (Mexico, Japan, Australia). In Europe and Asia, the US maintained its lead over China, despite China’s much-discussed Belt and Road Initiative.

Countries have also boosted their US-bound FDI flows. Direct investment in the US as a share of total investment has increased compared with the 2012-16 average. This is particularly true in countries associated with friendshoring (Mexico or Japan). A picture emerges of a deepening investment relationship between EMs and the US, which has kept it economy buoyant for longer than we initially assumed. As the effect of rate hikes accumulates, we expect this to reverse.

Geopolitical chairs

FDI linkages with the US are deepening, but global FDI is increasingly politicised. An IMF study found that allied countries are increasingly internalising their FDI. In 2010, the top 20% of geopolitically aligned countries (measured by UN general assembly votes) accounted for 37% of global FDI flows – in 2021 that reached over 50%.

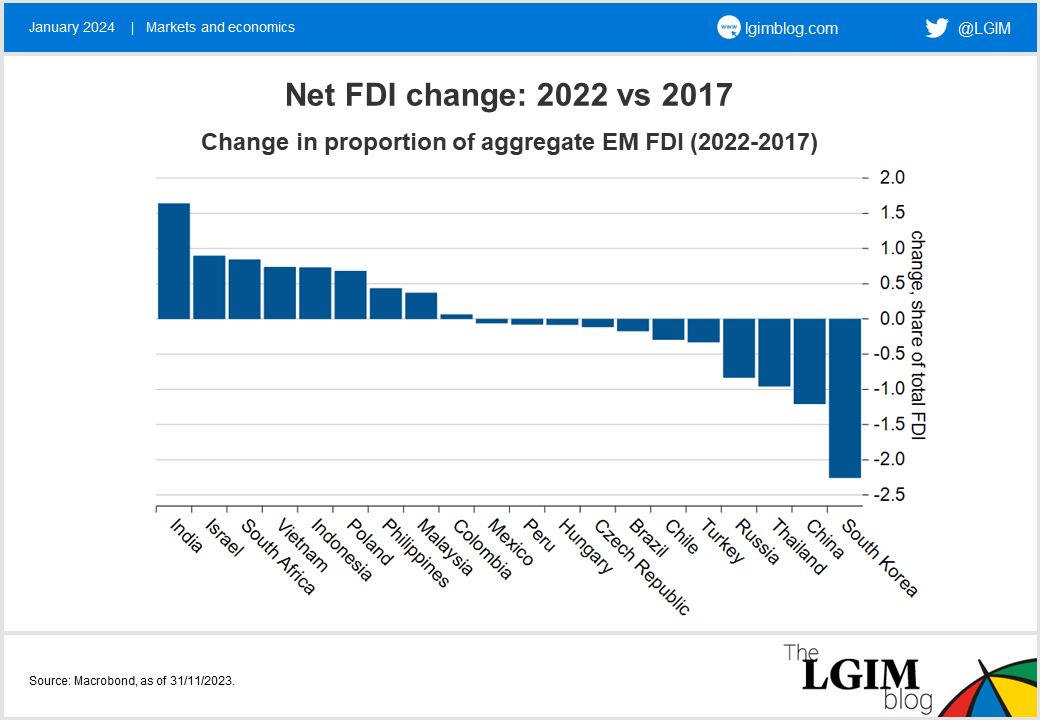

This is reflected also in official FDI statistics. By aggregating net FDI we can proxy the change in FDI shares across countries since 2017. The results are stark. China (where inward FDI has fallen since 2020) and South Korea (an FDI exporter) have seen their share of total FDI fall significantly, whereas India, Israel, Poland and Vietnam have seen their market shares rise. With friendshoring increasingly talked about, we believe this re-ordering of investment is likely to continue.

Semiconductors: an FDI story

This sorting of FDI is particularly acute in semiconductors. Recent years have brought semiconductors from a mere component to the core of Sino-US competition. According to IMF research, the emphasis on semiconductors in Western policy yielded a doubling of FDI from 2020 to 2022, while Chinese semiconductor-bound FDI fell to a quarter of its 2018 level.

All told, evidence of friendshoring is greater in investments than goods trade, with US investment playing a large role, particularly in sectors with substantial geopolitical significance, such as semiconductors. The reflection of the trend in investment reinforces our conviction that friend-shoring will persist.

But what will the impact of this trend be for Sino-US tensions? Who will benefit? And what will the consequences be for markets? This will be covered in the last instalment of this blog series.

This is the second in a series of blog posts covering global ‘friendshoring’; the last instalment will discuss trend’s impact on the world’s economy and geopolitics.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.