Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Italian debt: could risk premiums be returning to peripheral bonds?

During a testing period for non-core European credit, we explore if now heralds the return of opportunity in Italian debt.

The last few weeks have been testing for European government and credit markets – and for Italian sovereign debt, in particular.

During the European Central Bank (ECB) meeting in June, president Lagarde's language was too vague for the markets' liking and did not address the lack of progress on possible tools they could use to limit the widening of Italian spreads versus German bund yields. This rattled European markets - and rattled them hard.

Meanwhile, inflation is raging through key economies. The UK, US, and Eurozone all have annual inflation at or above 8% and rising, and it is unclear how drastic policy measures will need to be to contain it.

At the 9 June monetary policy meeting, the ECB President, Christine Lagarde, confirmed that a 25 basis point rate increase would be on the cards in July. Reacting to a sharp increase in the central bank’s inflation forecast, she also said the ECB expects to raise interest rates by 50 basis points in September, with more increases to follow.

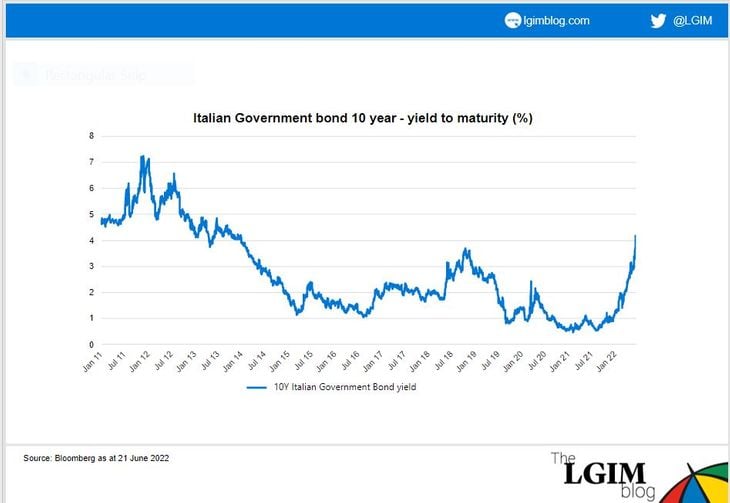

Right up to the ECB meeting, yields on Italian government bonds (aka ‘Buoni Poliennali del Tesoro’, or BTPs) were steady, at around 3%.

However, things quickly started to unravel afterwards, with markets pushing the Italian government’s borrowing costs to beyond 4% – a move reminiscent of the market stresses seen during the 2011 European sovereign debt crisis, as the chart below shows:

Even the yield on 10-year German government bonds (aka bunds) rapidly rose to above 1.75%. Bunds are generally seen as almost risk-free and are used as benchmarks for government debt across Europe.

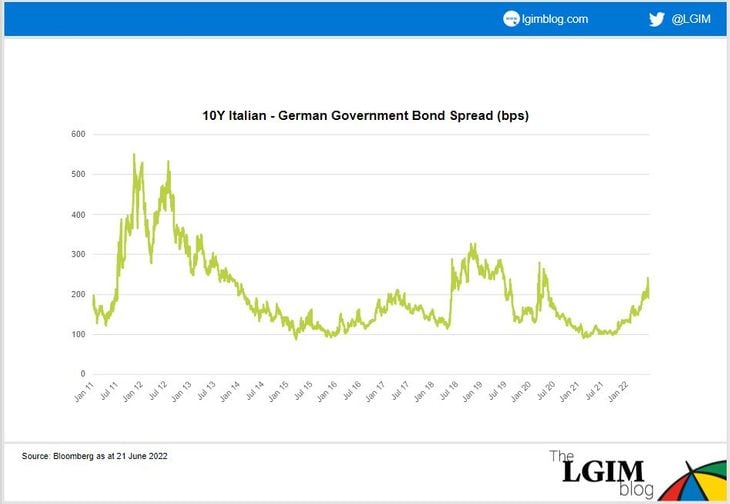

We can see some context for the move in Italian bonds by charting the spread (difference in yield) between German and Italian bonds. These spreads reached a high of 250 basis points soon after the meeting, but this is barely half what they reached in 2011. The chart below shows this:

Then, only a few days after their rate-setting meeting, the ECB announced an emergency meeting on 15 June to look at an ‘anti fragmentation tool’ to support peripheral government debt, in particular Italian bonds.

This was enough to provide some much-needed relief to the European markets, with yields on BTPs lower on the day of the announcement and the spread between Italian and German bonds soon falling back to its pre-meeting level of below 200 basis points.

So far, the proposed details of the relief package have been at the higher end of expectations:

- There was a quick turnaround in time for the July meeting

- We saw light levels of conditionality – the package relies upon conditions set for Next Generation EU (aka the European Union Recovery Instrument, an economic recovery package set up to support the EU member states during the COVID-19 pandemic). All players have pre-qualified for these measures

- They appear to be moving away from vague ‘market stress’ language to targeting set spread levels to encourage buying

Given the build-up in expectations, there is also a good deal of scope for disappointment if these tools cannot be agreed and become open to a legal challenge that could take years. For now, the market is taking comfort that this has effectively put a ceiling on Italian-German spreads.

Overall, if the ECB can convince the markets they can stamp out spread widening, hiking in greater increments may become more straightforward.

In the credit space, there hasn’t been a discernible premium attached to peripheral issuers for some time, especially in non-financials – partly due to the ECB’s corporate bond-buying programme.

The recent repricing of peripheral bank bonds and Italian corporates means some of that premium has returned, which in our view has begun to create some more interesting investment opportunities.

At this stage we don't know what the ECB will announce. However, even in the new paradigm where monetary support is lifted in the form of rate rises and quantitative tightening, recent events have indicated that central banks have got the markets' back.

At least for now.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.