Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Unconstrained strategies: what’s on the horizon?

Why it’s important to be flexible in unpredictable times.

This article is an extract from our Q4 2025 Active Fixed Income outlook.

The past – what just happened?

In September, the US Federal Reserve (Fed) cut interest rates for the first time this year by 25 basis points (bps). The updated dot plot is largely in line with market expectations, suggesting two more such cuts this year, followed by a further 75 - 100bps of cuts in 2026.

The move followed a weak US jobs report in August and a dovish Jackson Hole speech by Fed chair Powell, which led to a large drop in short-dated US Treasury bond yields, with the 2-year bond yield falling 33 basis points (bps) over the month.

Longer-dated Treasury yields fell in early September, lagging the move at the short end.

This extra risk premium reflected actions by President Trump, such as firing the Bureau of Labour Statistics Commissioner and calling for the resignation of a Fed member, which have raised concerns about Fed independence. Nevertheless, the September Fed meeting did show some resistance to the challenges from the administration, with near-unanimous support for the consensus 25bps cut, even from two Fed governors who were appointed by President Trump in his first administration.

Meanwhile, the Bank of England chose to cut interest rates by 25bps in August, but the rhetoric was relatively hawkish, while the European Central Bank kept rates unchanged at its September meeting.

French political noise impacted European credit markets, with the euro investment grade index spread widening initially, before tightening back towards the end of the month. High yield indices outperformed, with spreads a little tighter on the month.

The present – uncertainty reigns

We believe uncertainty is the new certainty due to geopolitical issues including the potential impact of US tariffs on the global economy. Therefore adopting a flexible approach by exploring opportunities across fixed income markets globally could help investors navigate idiosyncratic market risks. In our view, not being tied to a benchmark, sector, region or narrow duration target could help investors prepare for surprises.

Predicting gross domestic product or inflation moves on a consistent and accurate basis is near impossible, so we focus our efforts on probing consensus economic views and where adopting contrarian positions can be beneficial.

With government bonds, we think longer maturity yield curves are very steep, particularly in Japan and the UK. There is also a strong consensus that these curves will steepen even more, while we believe that governments are not incentivised to issue the most expensive debt. Therefore, we are more inclined to use yield curve flattening strategies at the long end.

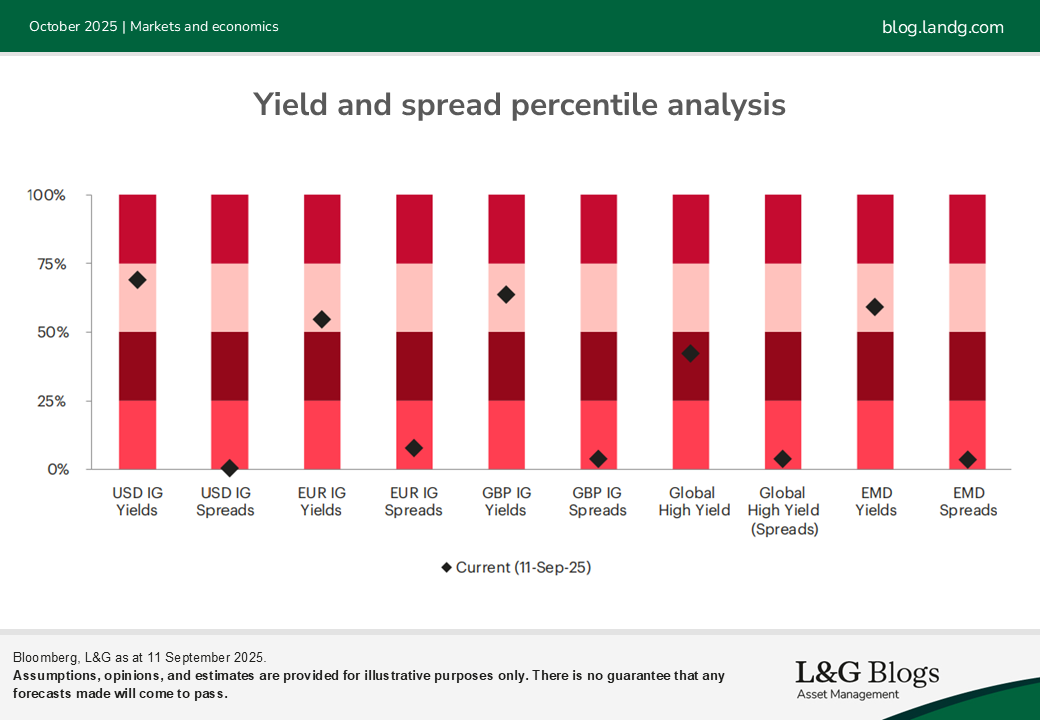

In our view, current credit buyers are driven more by yields than spreads. It’s feasible that spreads can remain tight while yields remain attractive. Therefore, we have maintained exposure to credit, building slightly larger liquidity buffers and levels of hedges using credit default swap indices.

Like many investors, we are driven to pursue both yield and carry to generate returns and smooth out some market volatility. With this in mind, we are currently exploring opportunities in bank subordinated debt, US corporate hybrids and selected areas of hard currency emerging market and high yield debt and shorter duration investment grade.

Outlook – what could go right or wrong?

Looking ahead, fixed income (and equity) markets have been supported by the prospect of Fed rate cuts and the large amount of capex spending by US tech companies. But there remains the risk that inflation is nudged higher due to tariffs or growth (either in the tech sector or more widely) disappointments, which could put credit valuations under pressure.

The recent weakening in labour market data cemented market views that the Fed will cut interest rates over the next 18 months, leading to an increase in inflows into credit. Additionally, the start of Fed rate cut programme could lead to some outflows from the huge $7.5 trillion held in US money market funds, some of which could potentially be directed towards fixed income. Therefore, we maintain a constructive short-term view on credit, which continues to be buoyed by strong demand and limited longer dated supply.

We believe US economic activity is likely to have a bigger impact on volatility than in other regions such as Europe, due to the tension between weakening labour market data and inflation remaining stubbornly above the Fed’s target.

There are also valid concerns from foreign investors about the implications of the end of US exceptionalism, although there are very few deep, liquid alternative markets.

The credit market’s robust supply and demand dynamics could be challenged should a large proportion of the US tech capex spend be funded via debt markets, which could result in a widening in spreads. US spread valuations continue to be slightly tighter than in Europe on a historical basis, which combined with the factors described above means we believe it’s important to maintain a balanced portfolio, without excessive concentrations in US credit.

This article is an extract from our Q4 AFI outlook.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.