Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

The barbarians are NOT at the gate

Concerns that rising leveraged buy-out (LBO) activity is bad news for high yield bonds are misplaced. Credit quality is improving, indicating lower default rates, which is good news for investors as spreads have further room to tighten.

When journalists Bryan Burrough and John Helyar wrote Barbarians at the Gate in 1989, they described a world where the rise of the leveraged buyout was leading to a corresponding decline in the credit quality of high yield bonds.

Not today.

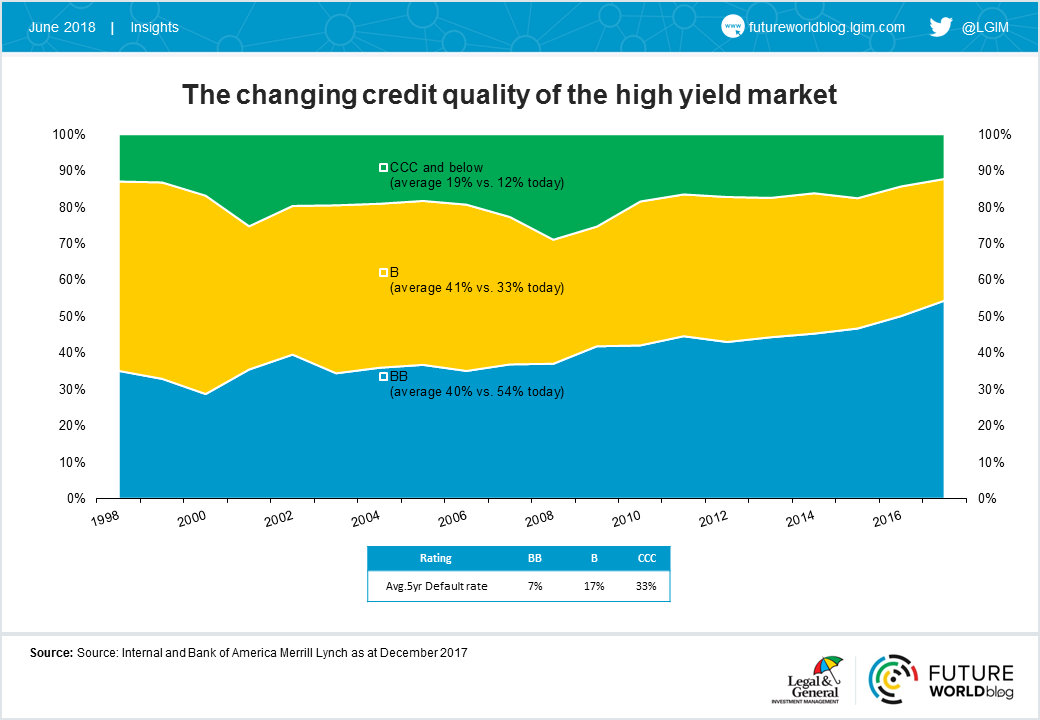

The credit quality of high yields bonds is improving, with a higher proportion of BB rated issues indicating lower default rates in future

Financing costs have been falling, which helps to improve company cashflows and hence the quality of the high yield market. What’s more, today’s coupon rates are typically 2% higher above the market yield amongst European BB-rated issuers, further reducing their borrowing costs. This means there is more headroom for global interest rates to rise before higher financing costs have a negative impact on corporate cashflows.

Nowadays, there are other options on the table to meet corporate financing needs.

Leveraged companies increasingly prefer loan issuance and private credit, rather than high yield bonds, to finance themselves

This is good news for the high yield market, for as leveraged issuers are turning away from bonds likely future credit concerns, and particularly default risk, are being transferred from the high yield bond market to the covenant light loan and private credit arenas.

So, while overall demand for higher yielding assets has never been greater, this shift to loans has led to outflows from the high yield bond market. Most significantly though, this has not hurt the performance of high yield bonds. Quite the reverse; during 2017 there was a negative correlation between capital flows and total returns from high yield bonds.

In the leveraged loan market, where covenants are typically short-term, one could argue credit risk is rapidly growing, removing some of the riskier debt that otherwise would have been parked in the high yield bond market.

If we are expecting a decline in default rates amongst high yield bonds, investors would intuitively expect compression in credit spreads (measuring the return over the risk-free rate) to continue.

Although credit spreads have compressed, we believe that high yield bonds still offer sufficient compensation for credit risk

Based on the average experience in BB rated bonds and quite possibly B rated issues as well, there is still sufficient compensation for credit risk. Amongst riskier CCC rated paper though, this might well not be the case.

Some have argued that the improvement in credit rating within the index could be a product of the rating agencies changing their methodology. However our experience when we are reviewing the many issuers that pass our desk is that this is not the case.

So on that basis, the next time we hit a major economic slowdown, the high yield bond market could actually experience a lower level of defaults.

This is good news for investors, as the market has yet to discount potential for lower default rates

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.