Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Riding out regime change in fixed income

We assess how public and private credit investors can navigate macro volatility, while questioning the enduring strength of US Treasuries and the outlook for cash rates.

The following is an excerpt from our midyear global outlook.

At the beginning of the year, the one constant we expected from the new US administration was volatility. That expectation was more than met in the first half of the year.

We do not anticipate any meaningful falls in volatility or uncertainty for the remainder of the year, given that the outlook for trade, fiscal policy and the economy remains unusually murky. So, for investors in public credit markets, we believe it’s increasingly important not to become wedded to a particular view on inflation or recession, and to retain flexibility over asset allocation decisions.

During periods in which the market grows concerned about inflation upswings, we would expect to see upward pressure on interest rates. Worries about recessionary conditions would have the opposite impact. However, both inflation and recession worries can be triggered by supply-side restrictions (arising from tariffs, immigration restrictions or oil supply concerns). Benign pricing means that we generally prefer shorter-duration positioning, but the market’s attitude is in flux as concerns oscillate between those twin implications of the same set of shocks.

For credit allocation decisions, the second half of the year may increasingly be a ‘stock’ picker’s market. We will be relying on our integrated research team of credit, equity and investment stewardship analysts to guide us through the murk. They will be assessing which companies can better cope with the volatile environment, or whether you are being paid for the company’s particular risk profile.

Investors should also continue to focus on the strength of technicals in fixed income, in our view: buyers in search of yields rather than spreads have dominated flows, resulting in spreads remaining at tight levels on a historic basis. Thus, spreads can remain range-bound for a long period of time, with the higher yields in fixed income remaining the main source of return.

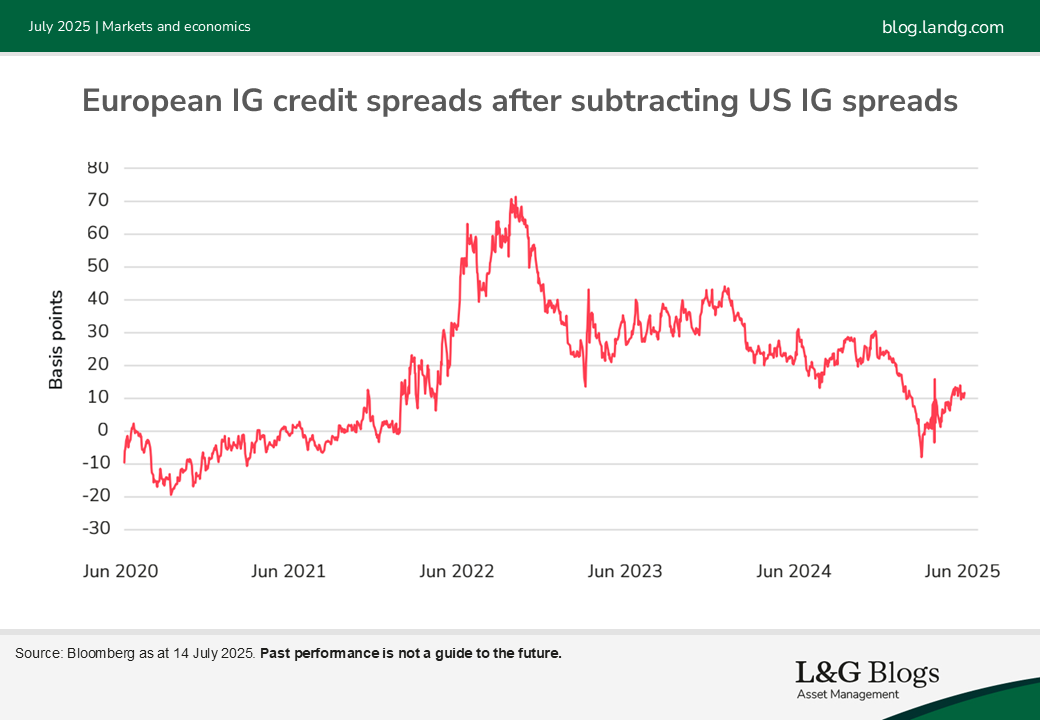

This analysis of technicals will then include the key question surrounding the apparent lack of US exceptionalism – and the willingness of foreigners to continue investing in US markets. We think there will be increasing interest in non-US credit markets from Asian investors as they look to diversify their exposures – but they cannot abandon the American market altogether. Therefore, the relative valuation differential between US and European credit will remain a key area of focus for us.

Private credit props

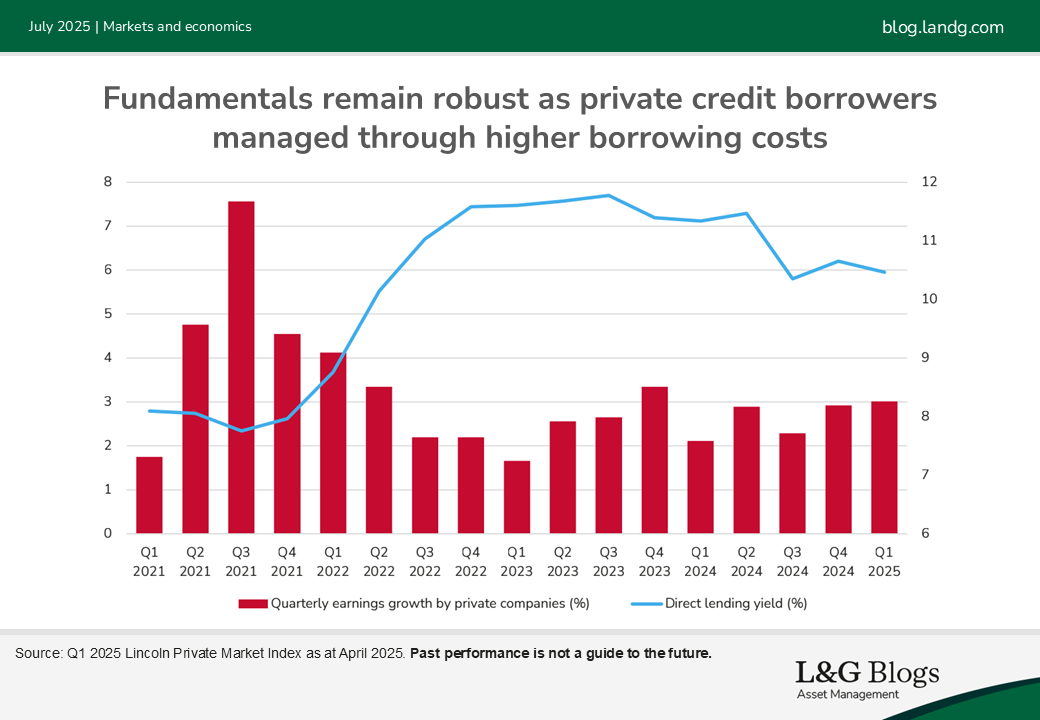

A prolonged higher-for-longer rates regime is supportive for private credit returns, in our view. Sub-IG direct lending yield (c.10% currently)[1] remains high in absolute terms, although only average relative to history. IG private credit yields (c.5-7%)[2] are pricing towards the top of the historical range, offering potentially attractive returns.

Similar to public markets, private credit spreads are relatively tight – although the illiquidity premium has been stable so far in 2025. We are seeing increasing dispersion, with borrowers insulated from tariff volatility experiencing limited effect on pricing, while those more impacted or of lower credit quality need to offer wider spreads to attract lender demand. We prefer to be defensive in the current environment – non-cyclicals over cyclicals – and focus on diversification.

We view private credit as relatively sheltered from the recent macro volatility – at least in terms of direct tariff impact.

A large chunk of investment grade private credit is infrastructure, utilities and real estate issuers, all of which are supported by highly predictable cashflows. Sub-IG borrowers, meanwhile, are concentrated in companies with domestic operations and service-based revenue, rather than goods-based. Direct exposure to tariff impact has been estimated at around 10%.[3]

Fundamentals have been robust, with earnings growth capable of managing leverage in a higher rate environment so far. But prolonged trade tensions and fiscal concerns will have a broader influence and add to overall risk for the asset class.

We believe that cost increases, lower demand and more uncertainty for business planning will likely hit earnings growth, leading to weaker borrowers breaching debt covenants. We see smaller companies as disproportionally impacted, due to limited pricing power and revenue diversification. Another source of risk is the 2021-2022 vintage of loans – originated when yields were low and leverage high. They are coming up for refinancing in 2025-26 and could struggle due to higher debt costs and a weak M&A market.

All these factors raise concerns of an increase in defaults and represent a big test for the covenant-loose loans that have dominated direct lending issuance in recent years.

Three reasons why Treasuries are here to stay

In recent months, policy changes emerging from America have led to anxieties around the US Treasury market. Amid the disruption of the ‘Liberation Day’ tariffs, the US dollar weakened and government bond yields jumped – the opposite of what conventional wisdom would have expected.

Observers since have speculated that this portends ill for the dominance of the US Treasury market. However, despite investor heartburn, we see risks to US asset dominance as more modest than extrapolation suggests for three reasons.

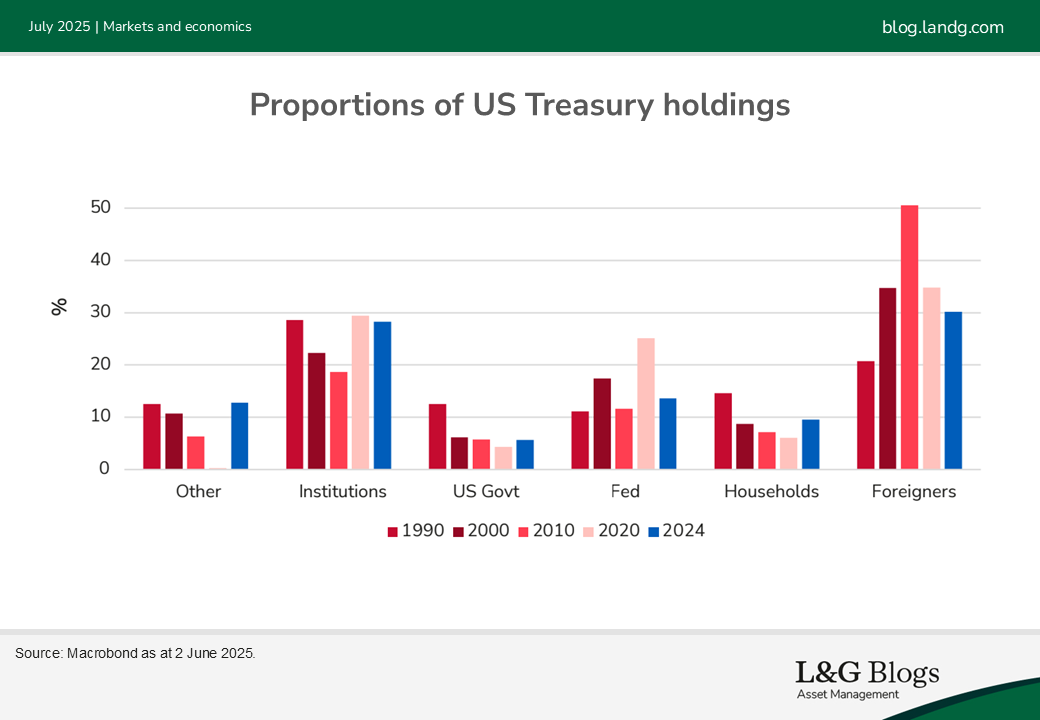

- The threat of mass selloffs of Treasuries from foreign actors, ominously speculated about in early April, carries less weight than before.[4] The mid-2000s saw discussions of the “balance of financial terror” between the US and offshore Treasury holders.[5] Since then, though, US debt ownership has become substantially indigenous, with the foreign share of Treasury holdings falling from 55% in 2008 to around 30% today.[6] This blunts the threat of an external effort to dethrone the dollar-Treasury nexus.

- While debates in Congress make it clear policymakers are relaxed about deficit reduction, it’s likely demand exists to absorb new issuance. Externally, International Monetary Fund forecasts of surpluses among major creditor countries suggest a trajectory of accumulation of new assets outpacing Treasury issuance.[7] Domestically, the Fed is mulling slowing its shedding of Treasury bills and there is talk of regulatory change to make it easier for banks to hold US debt. We think all these actions will supplement demand for Treasuries, and offer them some ballast despite a more erratic policy environment.

- Lastly, there exist meagre alternatives to US asset dominance. China, the US’s greatest rival by GDP, maintains capital controls, limiting outbound investment and stunting its ability to serve as a competitor. Europe’s debt has neither the scale nor the internal cohesion to challenge US hegemony. Unorthodox alternatives such as gold or cryptocurrency could be touted as alternatives, but neither produce income – nor are universally accepted as collateral like US Treasuries. US government paper remains the unavoidable global asset, and there’s little evidence this will change much in future. in our view.

The second Trump administration is likely to continue offering markets a lot of disruption to digest. From trade and fiscal policy to geopolitics, we should expect a greater risk appetite than prior administrations. However, we believe the displacement of Treasuries will likely take bigger shocks and a more sustained push by rivals over a longer timeframe than we have seen.

What’s in store for cash?

Short-term cash rates will continue to be influenced by monetary policy decisions throughout the second half of the year. Across the US, UK and Eurozone, we expect central banks to continue with a data-dependent and gradual approach to cutting interest rates.

While our baseline expectation is for one or two cuts in each of these markets in the second half of 2025, increased market uncertainty amid the changing US policy agenda means we could see either more or fewer cuts depending how economic data evolves. Should inflation pick up again, we could see central banks opt to maintain restrictive monetary policy, with rates on hold or only coming down very slowly for the remainder of the year. However, we do not expect to see an increase in interest rates.

In the event of a sharp deterioration in economic data, a faster removal of restrictive policy would be warranted through more aggressive rate cutting to support global economies, potentially up to three or four times depending on the speed and scale of any deterioration. While markets await clear direction in the data, we expect cash rates to remain attractive to investors for the remainder of the year.

This article is an excerpt from our midyear global outlook.

[1] Source: L&G as at May 2025.

[2] Source: L&G as at May 2025.

[3] Source: KBRA and Fitch.

[4] Source: https://www.cnbc.com/2025/04/15/us-treasurys-selloff-whathappened-and-why.html

[5] Source: http://www.perjacobsson.org/2004/100304.pdf

[6] Source: Macrobond as at 2 June 2025.

[7] Source: https://www.imf.org/external/datamapper/BCA@WEO/OEMDC/%20ADVEC/WEOWORLD

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.