Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Not here for the (credit) duration…

Why we prefer short-dated UK credit over longer-dated corporate bonds.

“Age is an issue of mind over matter. If you don’t mind, it doesn’t matter.”

Mark Twain had a profound understanding of human nature, but he wasn’t well known for his fixed income expertise.

Yet on the question of age in fixed income, we find that it can matter. Our analysis suggests that a strategy of owning five- to 10-year UK credit – alongside healthy gilt and cash balances – while being underweight over-10-year UK credit typically produces higher expected returns over the long run.

That doesn’t mean there isn’t a place for long-dated UK corporate debt in an active UK corporate bond portfolio, though: after a drawdown, future expected returns are larger for over-10-year UK credit as spreads recover.

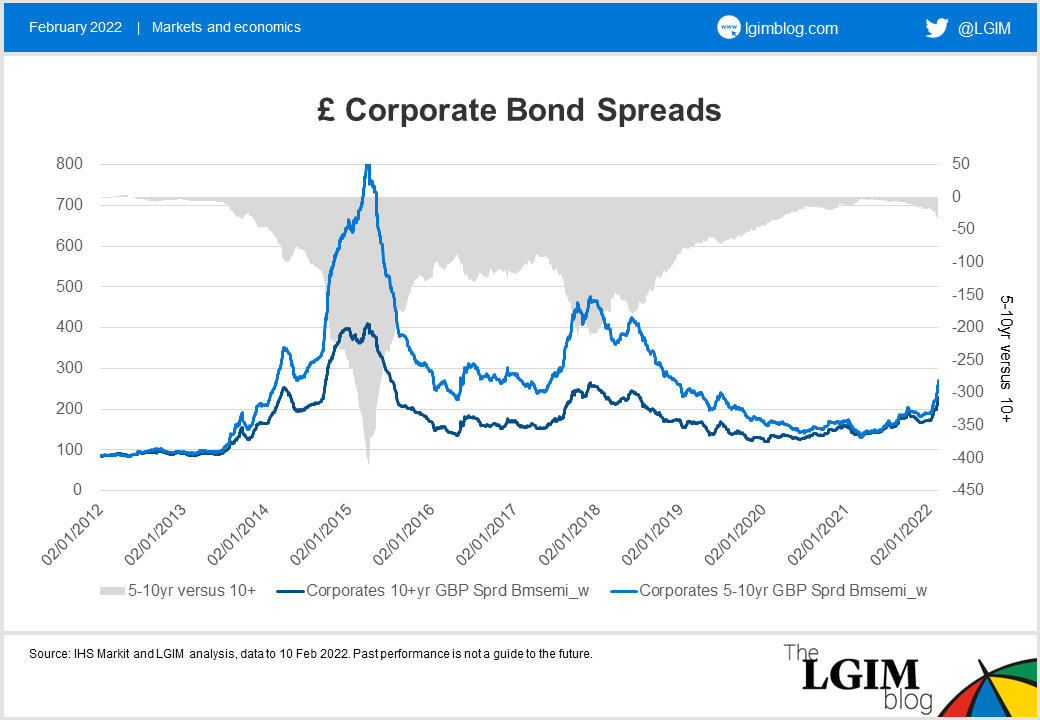

Diminishing demand for long-dated debt

The UK corporate bond market is undeniably the home for long-dated credit issuance and demand. Traditionally, pension schemes have needed long-dated credit to match long-dated liabilities, and this has created a UK credit curve that is flatter than that of its European and US corporate bond counterparts. Given this, potentially more attractive spreads are on offer in the five- to 10-year part of the UK credit curve, in our view.

Yet there is still strong demand for long-dated UK credit, which has kept the UK credit curve relatively flat. However, as pension funds mature and liabilities come to the fore, demand for traditional long-dated UK corporate bonds is diminishing. If this trend continues, then we expect to see UK credit curves steepen and lower excess returns in long-dated UK corporate bonds.

Counting the cost of tight spreads

In the current world of historically expensive and low-volatility credit spreads, we don’t believe we’re being paid to own low-spread and long-dated UK corporate bonds.

Instead, we have a preference for higher-spread, short-dated bonds as we believe our credit expertise enables us to better price that higher credit risk and derive higher expected returns from the carry component while providing a degree of cushioning against larger negative drawdowns if spreads widen.

Longer-dated credit hasn’t had its day, though. Our analysis indicates that the best time to buy longer-dated credit is usually after a market drawdown. In these periods, the premium that must be paid for the greater liquidity of shorter-dated bonds may be better spent rotating into longer-dated credit, with a view to capturing higher expected returns from future spread tightening.

Mind the liquidity gap

Given default risk is historically very low in investment-grade credit, the main components of the credit spread are liquidity risk and downgrade risk. Within our experienced credit-trading team, we see liquidity risk as currently under-priced across the curve, and any increase in liquidity risk premium is likely to result in lower expected returns for over-10-year bonds compared with five- to 10-year securities.

Finally, we believe our expertise in credit selection will help us identify credits within the five- to 10-year space that offer attractive expected returns without having to take undue duration risk and expose the portfolios to the possibility of steeper credit curves in UK corporate bonds. This should also help to safeguard expected returns in the event of a drawdown.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.