Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Moving on up: is another ‘goldilocks’ year in store for high yield?

Many investors thought 2023 would be a year of defaults and credit pressure. As it turns out, last year might actually be described as a ‘goldilocks’ period for high yield. Could the asset class continue moving on up this year?

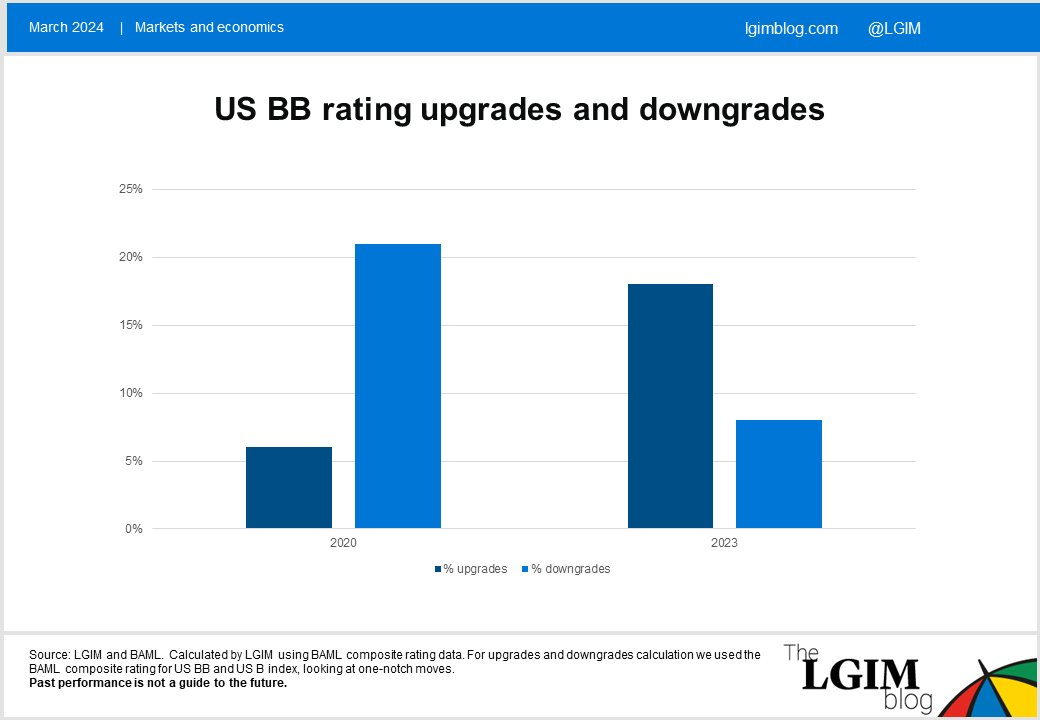

2023 saw a notable upward shift in the ratings provided by the core rating agencies (Moody’s, Fitch and S&P), and this momentum could continue into 2025. Contrary to some expectations, idiosyncratic credit risk has been improving, with nearly a fifth of BB and B rated bonds experiencing at least a one-notch upwards shift.

Upgrades now outweigh downgrades within high yield; for double B rated bonds the upgrade ratio (a measure of the relative frequency of credit rating upgrades and downgrades) has gone from 0.3x in 2020 to 2.6x as of December 2023[1].

Furthermore, 14% of these upgrades have been ‘rising stars’ (rising stars can be defined as when an issuer moves from high yield to investment grade, according to its rating). Quite a contrast to 2020, as observed in the chart below:

What changed?

In our view, the rating agencies became too pessimistic when COVID-19 struck in 2020. Then, conversely, the strong economic growth in 2023 that surprised most spurred the agencies to begin revising their tune. This was most noticeable in fallen angels becoming rising stars, with over 25 issuers becoming rising stars in 2023 compared with only 10 fallen angels.

With the strong growth and likely falling rates and spreads, this revision upwards in ratings, in our opinion, will continue in to 2025. This could also support further spread tightening and lower the cost of finance for many companies, especially rising stars.

We therefore believe 2024 could turn out as positive as the year just past and could potentially bring another 12 months or more of ‘goldilocks’ conditions for the asset class.

[1] Source: LGIM and BAML. Calculated by LGIM using BAML composite rating data. For upgrades and downgrades calculation we used the BAML composite rating for US BB and US B index, looking at one-notch moves.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.