Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Global high yield: Quiet strength beyond the headlines

Global high yield remains resilient; benefiting from strong corporate fundamentals and liquidity, with robust technicals.

This article is an extract from our Q4 2025 Active Fixed Income outlook.

The past – What just happened?

Markets have continued to digest the implications of US President Trump’s tariff policy, with volatility driven more by political headlines than economic fundamentals. Investors have largely adopted a ‘wait and see’ approach, interpreting aggressive proposals as negotiating tactics rather than imminent policy shifts.

High-yield spreads tightened by approximately 20 basis points (bps) since the end of June, with yields peaking at 6.32%* before retracing to around 6.05%*. This tightening reflects improved risk sentiment and a robust technical backdrop, with strong inflows and limited new issuance supporting valuations.

European and emerging market high yield segments led the rally, buoyed by strong technicals (light supply, sustained inflows) and broad spread compression.US high yield also rose but was more modest as higher Treasury yields partly offset its gains. From a credit ratings perspective, single-B credits performed roughly in line with double-B credits across the globe.

The present – positioned for income with a regional tilt away from the US

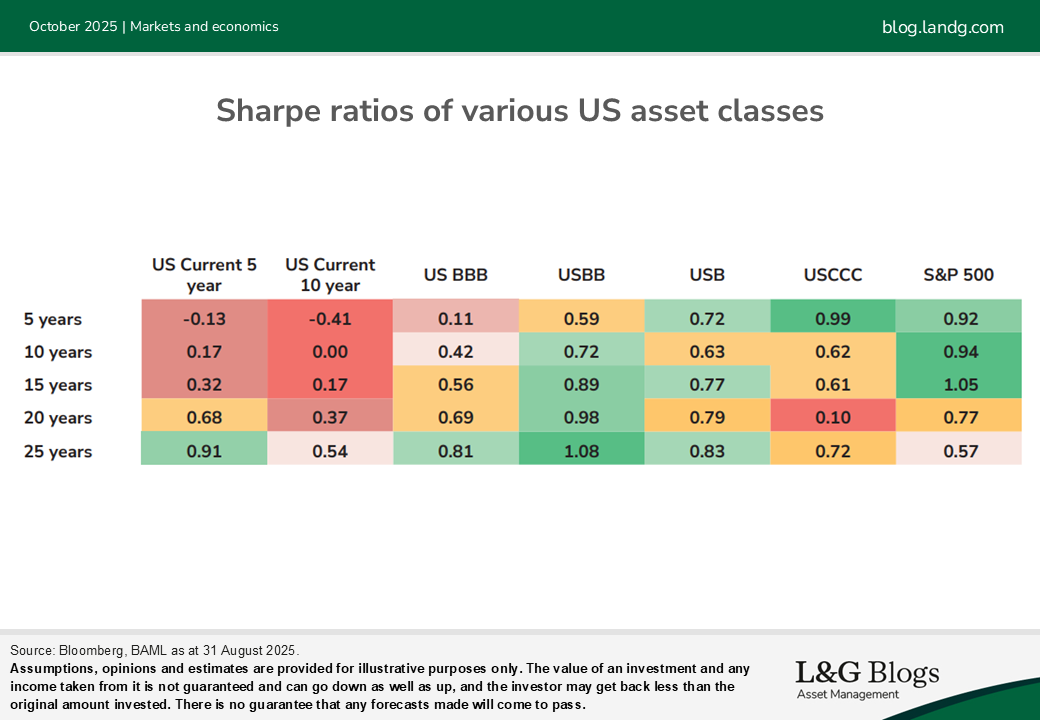

We maintain our macro credit score at +1, reflecting our view that credit risk remains attractively priced. We believe the high yield market acts as a strong income asset class, with investors generally compensated for default risk (particular in the BB and B rated cohorts). Comparisons to historic spreads should bear in mind that the current high yield index is higher quality (BBs dominating with 60% of the index versus less than 8% of CCCs), lower duration (3 years versus the historical average of 4 years) and the reference government bonds are more volatile and lower quality now than historically.

This is illustrated in the Sharpe Ratios table below which compares various US asset classes – with corporate credit, particularly the BB cohort producing persistently higher Sharpe ratios versus government bonds (and investment grade credit). Yields at 6.1%* are close to the historic median, and duration remains low at 3.2 years.

The high-yield market is benefiting from strong corporate fundamentals and liquidity, with technicals remaining robust due to limited net new supply and strong demand.

Regionally, we remain overweight Europe and emerging markets (EM) and underweight the US. In our view, European credit benefits from consistent policymaking and fiscal support, while EM offers similar macro risks to the US but with higher spreads and yields. US policy-related downside risks are not fully priced in, reinforcing our cautious stance.

Sector-wise, we continue to favour media and technology, real estate, and aerospace/defence. We remain underweight automotive and utilities, which face structural challenges and capital intensity.

Outlook – Coupon-like returns with limited tail risk?

The global high yield market continues to exhibit resilience despite various global challenges. Market consensus has shifted away from a technical recession in the US in 2025 and global growth is low but steady – a very supportive backdrop for credit. The US Federal Reserve’s move to cut rates by quarter point in September and signal there may be more to come is a strong potential tailwind. Within this context, our outlook for global high yield remains positive, with a focus on carry and selective risk-taking.

We believe spreads can tighten further into year end, within a relatively narrow band of outcomes. The market is likely to deliver coupon-like returns, currently around 6.2%, with the index already up 6.8% YTD** as at 10 September 2025.

What could go wrong?

- Policy disruption and constraints: While escalating policy shocks or geopolitics could tighten financial conditions, a mild US recession alone is unlikely to cause a spike in defaults unless credit transmission deteriorates more broadly.

- Inflation rebound: The main risk to yield demand and the carry trade. We believe high yield’s low duration offers resilience in stagflationary environments compared toother fixed income asset classes, although absolute returns would be lower.

This article is an extract from our Q4 2025 Active Fixed Income outlook.

*Unhedged yield for the ICE BAML BB-B Global non-financial index (HWXC)

**USD hedged total returns for the ICE BAML BB-B Global nonfinancial index (HWXC)

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.