Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Global high yield… don’t worry, be happy

Investors might prefer to focus on the yields on offer in the asset class, rather than worry about what, we believe, is the misplaced fear of defaults.

The below is an extract from our Q3 Active Fixed Income Outlook.

The past: what just happened?

The second quarter of 2024 registered positive returns across the globe in high yield. Emerging markets, once again, led the way, followed by Europe and the US. Credit spreads were broadly unchanged, and BB rated bonds outperformed single B rated bonds. Demand for the asset class persisted as fundamentals and global growth remained robust, and the yields on offer, standing at more than 7%,[1] continued to appeal to many investors.

The present: reducing exposure in Europe

The strategy continues to target a higher income than the comparative benchmark, expressed through an overweight position in higher spread global names. Our view remains that spreads adequately compensate for the degree of credit risk undertaken (see outlook).

From a regional perspective, we have started to reduce exposure in Europe, rotating back into the US, with emerging markets constituting our largest overweight position. From a sector perspective, our focus on the ‘core’ part of the economy remains, with an overweight exposure to the consumer, services and industrial sectors. Conversely, we have underweight positions in the global automotive, utilities and shipping sectors.

What could go wrong?

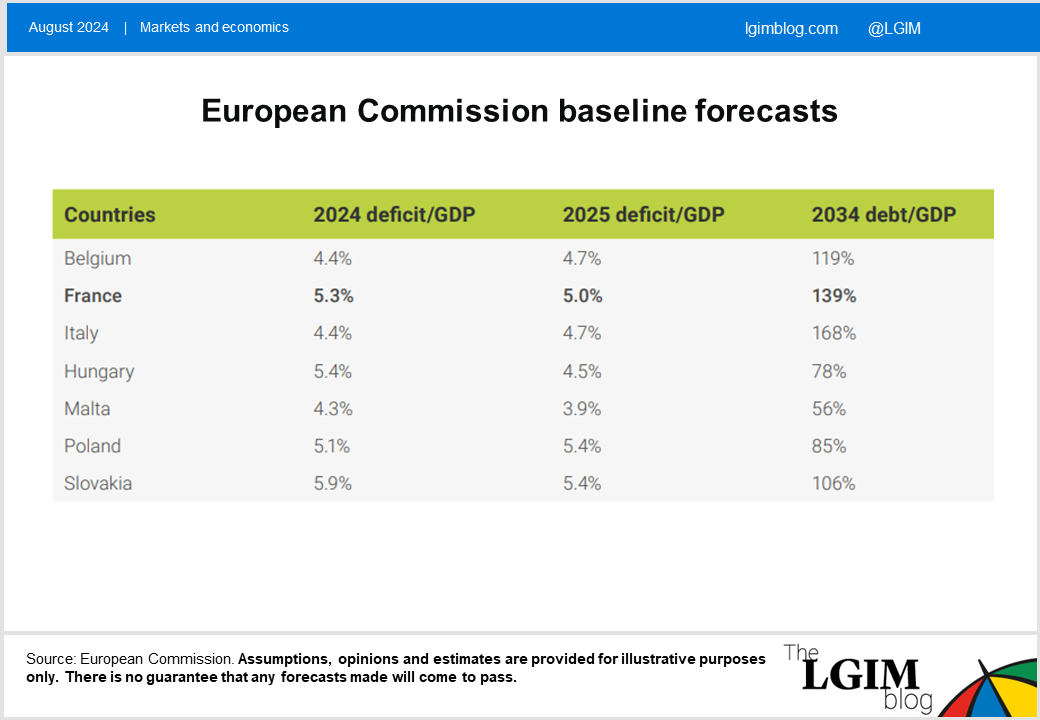

There are many known elections, but it’s the unknown, snap elections that appear to cause the most concern. French parliamentary elections illustrated this, while focusing investor attention on imbalances, such as deficits and debt burdens.

As the first table on the right shows, France has one of the largest sovereign debts in Europe – along with Belgium and Italy. This has caused us to be more cautious on our positioning within Europe because downside risk doesn’t yet seem reflected in high yield credit markets.

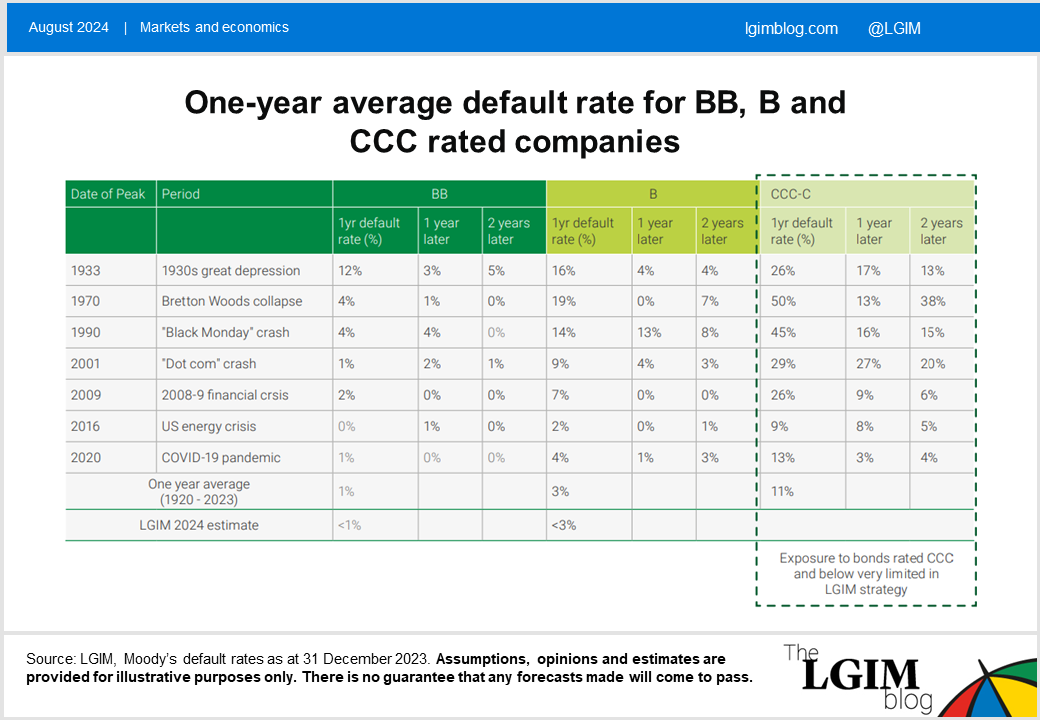

Although defaults have ticked up, they remain around historic averages. Going forward, we expect this to continue within an environment of decent global growth and expectations that central banks will likely begin cutting interest rates towards the end of 2024. Improving credit quality in the index supports this view.

On a final note, there are many myths about high yield that we would like to contest.

For now, we shall comment on what we believe to be the misplaced fear of defaults in the higher quality segment of the high yield universe (BB and B rated). As the below table shows, historic average one-year defaults are less than 1% for BB and around 3% for single B rated bonds. During periods of crisis, the default rate rarely rises above 7%, even for single B rated bonds.

This explains why, if investors buy BB and B rated bonds and keep them for the average life of the bond (three to four years), they generally earn at least 75% of the yield on offer. Historically, the income received has more than offset mark-to-market volatility and losses due to defaults over the same period.

The above is an extract from our Q3 Active Fixed Income Outlook.

[1] Source: HW00 ICE BofA Global High Yield index as at end June 2024, total returns, US$ hedged.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.