Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Global high yield – ain’t no mountain (or wall) high enough

We believe the current environment remains favourable for high yield bonds. Worries over upcoming maturity walls are unfounded, in our view. We believe the key reason for any delay in refinancing for many companies is to gain access to better terms, not an inability to access capital.

The below is an extract from our Q2 Active Fixed Income outlook.

The past: what just happened?

The first quarter of 2024 registered positive returns (~2%[1]) across the globe in high yield, with emerging markets leading the way, followed by Europe and the US. Credit spreads tightened and single B rated bonds outperformed BB rated bonds.

Demand for the asset class continued during a period which saw a supportive earnings season, decent global growth, and market expectations that central banks will begin cutting rates in 2024. Defaults remain around historic averages and we expect this will continue – largely on account of flexible bond terms, sensible levels of indebtedness among most issuers, and robust profitability and cash generation.

The present: key themes

We’ve added higher income bonds correlated more to credit improvement and less to long-term interest rates. Our view remains that spreads adequately compensate for credit risk and, in our strategies, we are targeting a higher yield than the benchmark.

From a regional perspective, we have reduced our exposure to US high yield in favour of European and emerging markets. US credit spreads appear relatively tight, while the US region has a higher interest rate environment compared with Europe and developed Asia. As the global economic outlook is set to improve, we seek to take credit risk in core parts of the economy in consumer, services and industrial sectors.

By contrast, we have underweight positions in the global automotive, utilities and shipping sectors. Underpinning our investment choices is our incorporation of behavioural finance – we are constantly on the lookout for imbalances between hard data and the interpretation and valuation ascribed to companies by the market.

What could go wrong?

One key risk in 2024 is growth remaining strong in the US despite the interest rate hiking cycle, which could force the market to reassess its expectations for multiple Federal Reserve rate cuts in the second half. This could negatively affect the price of longer-dated corporate bonds and compromise the strong inflows into fixed income asset classes that we’ve seen so far this year. That said, we believe strong growth would protect high yield bonds (and more importantly keep open the refinancing window by supporting corporate creditworthiness).

Outlook

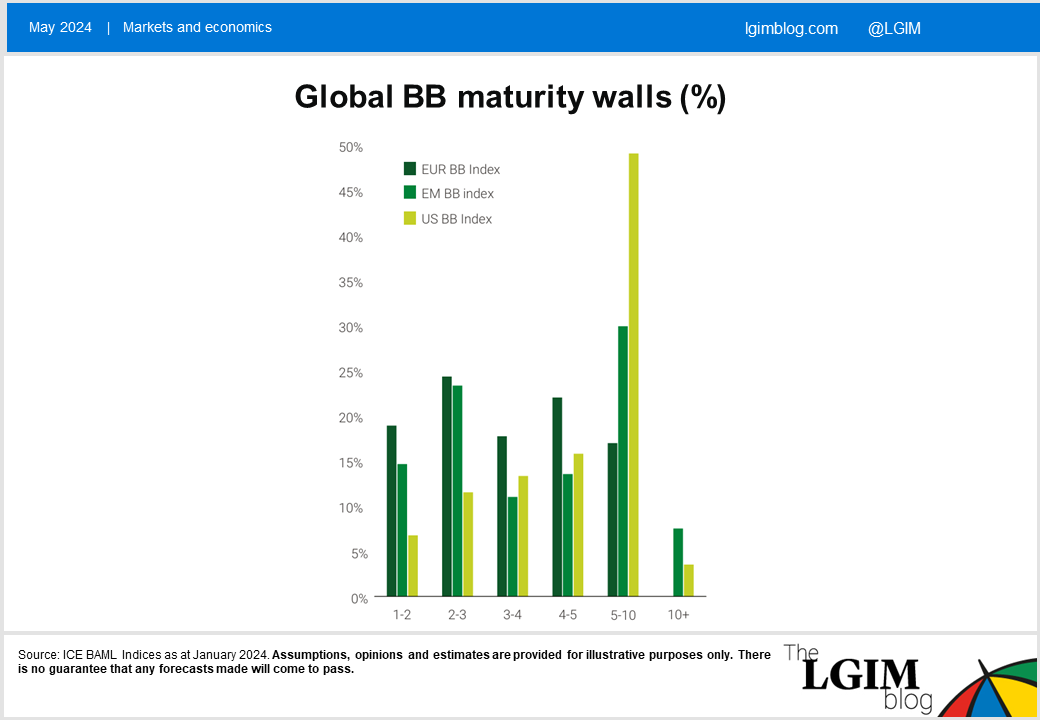

Many investors pay particular attention to maturity walls – the total amount of debt that will mature in coming years. Overall, the majority of global high yield, BB and B rated bonds are at least three years away from maturity (see chart below for BBs) with almost all having call structures which enable flexible refinancing. Both BB and B have a considerable amount of debt (although still less than one-fifth) maturing in 2025 but we don’t believe this should ring alarm bells.

The low default rate (which we expect to stay low as the global economy rebounds) tells us companies have not been squeezed into default just because of upcoming maturities. The refinancing requirement for 2025 translates to similar levels of historic average issuance volumes in each of the areas. Furthermore, many issuers are moving to the leveraged loans and direct lending markets, potentially taking the pressure off the high yield bond market.

Our final consideration highlights the still low average bond price (around 95 for BB and B rated bonds) and so, we believe, the refinancing cycle represents an opportunity for investors as those bonds move to par.

The above is an extract from our Q2 Active Fixed Income outlook.

[1] Source: HW00 ICE BofA Global High Yield index as at end Q1 2024, total returns, local currency

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.